EE bond’s fixed rate stays at 2.7%; doubling period holds at 20 years

By David Enna, Tipswatch.com

After signaling for a few days that it would hold off to May 1 to announce new rates for U.S. Series I Savings Bonds, the ever-unpredictable Treasury did it early anyway, and it matched my expectations.

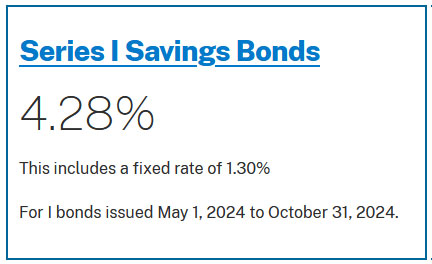

The I Bond’s new fixed rate holds at 1.3% for purchases from May to October, and the composite rate falls from April’s 5.27% to 4.28% for new purchases.

The I Bond’s fixed rate is important for investors. It is permanent and stays with an I Bond until redemption or maturity in 30 years. This new fixed rate only applies to I Bonds purchased from May to October 2024.

The inflation-adjusted variable rate applies to all I Bonds, no matter when they were issued. It changes every six months and the starting date of the change depends on the month you bought the I Bond. This new 2.96% variable rate is based on non-seasonally adjusted inflation from October 2023 to March 2024.

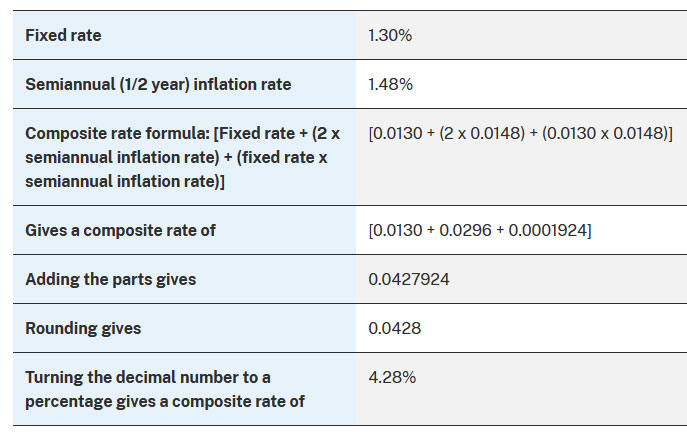

The composite rate is based on a combination of the fixed and variable rates, using this formula:

The new inflation-adjusted variable rate rolls out over time, as I noted. For example, if you bought an I Bond in April 2024, it would earn 5.27% through September, and then transition to 4.28% for six months beginning in October.

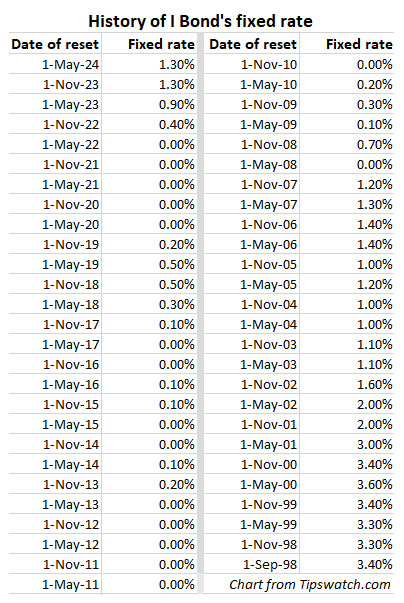

Track the history of the I Bond’s variable rate on my Inflation and I Bonds page.

No surprises

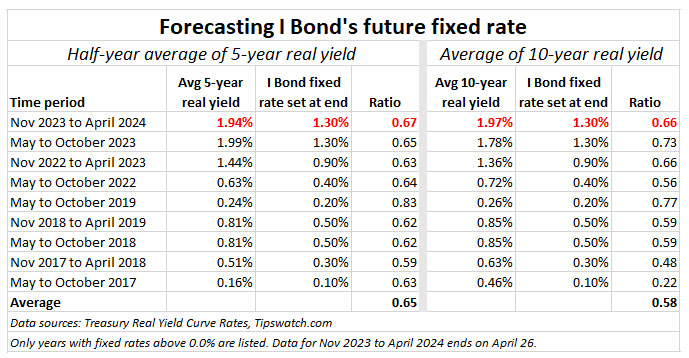

I Bond watchers (like me) had been forecasting that the fixed rate would hold at 1.3%, based on a ratio of 0.65 applied to the six-month average of 5- and 10-year real yields. and then rounded to the tenth decimal point. It was reassuring to see the forecast worked, this time. This gives us a little more supporting data on how the Treasury makes this decision.

Reaction

I have been recommending making your 2024 I Bond purchase in April to lock in both the 1.3% fixed rate and 5.27% composite rate for a full six months. Now that the fixed rate held at 1.3%, that strategy looks solid. Now we can await the November 1 rate reset.

Timing your investments can be important, because I Bond purchases are limited to $10,000 per person per year unless you use your tax return to get paper I Bonds or add to your holdings through gift-box, trusts, or business-owner strategies. Whatever rate is set in November will be available for purchase in January 2025, when the purchase limit resets.

Even though T-bills have yields higher than the I Bond’s new composite rate of 4.28%, these savings bonds still make sense for investors looking to build a large cash reserve that is inflation-adjusted, tax-deferred and totally safe. Right now, it is T-bills for the short-term, I Bonds for the long-term.

EE Savings Bond

The Treasury decided to hold the fixed rate on the EE Savings Bond at 2.70%, well below the yield of comparable nominal Treasury investments. I had been predicting the rate could rise to 2.8% or 2.9%, based on the trend in yields for the 10-year Treasury note (currently yielding 4.63%).

The Treasury also held the EE bond’s doubling period at 20 years, meaning this savings bond will yield 3.53% compounded if held for 20 years. I had expected that decision, but honestly, it would be more fair to set the doubling period at 18 years, creating an effective yield of 4%.

I doubt there will be much interest in EE Savings Bonds when T-bills are earning nearly 5.5% and the 20-year Treasury bond yields 4.86%. Both of those make more investment sense. Too bad.

What’s your reaction?

Investors are sorting through a lot of issues when considering I Bonds these days. T-bills offer a better rate of short-term return, with no fear of a penalty for early redemption. Treasury Inflation-Protected Securities offer better real returns, but with more complexity and potential market fluctuations.

I suspect most I Bond investors have already purchased their allotment for 2024 and are now ready to sit back and enjoy life.

FYI, earlier today (April 30) I looked on TreasuryDirect and it “appeared” you could still set a purchase for April 30, 2024, which in theory would get the higher April composite rate. Forget it. I have already gotten feedback from a reader that a purchase entered today is getting the May rate.

The Treasury really needed to clarify its wording, which said for several days, “The current rate of 5.27 percent is available until 11:59 p.m. Eastern Time on Tuesday, April 30. The new rate becomes available at midnight.”

That was highly suspect.

Now, on the afternoon of April 30, TreasuryDirect has gone in and changed the wording on its I Bond FAQ page to this bizarre past-tense instruction:

The rate of 5.27 percent was available until 11:59 p.m. Eastern Time on Tuesday, April 30. The current rate of 4.28 percent became available at midnight.

Treasury, you screwed this one up.

Post your ideas and thoughts in the comments section below.

• Confused by I Bonds? Read my Q&A on I Bonds

• Let’s ‘try’ to clarify how an I Bond’s interest is calculated

• Inflation and I Bonds: Track the variable rate changes

• I Bonds: Here’s a simple way to track current value

• I Bond Manifesto: How this investment can work as an emergency fund

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

David, a typo I picked up rereading; in italics:

Reaction

I have been recommending making your 2024 I Bond purchase in April to lock in both the 1.3% fixed rate and 5.27% variable rate for a full six months.

Thanks for spotting that. It is fixed.

David, thank you for all the information.

Now that you have informed us about the gift box, I don’t worry if the fixed rate of I-Bonds go up in October, since I can always put another 10K via the gift box strategy at the higher rate.

“Have your cake and eat too!”

As others have mentioned, one of my interest rates is “Not Available.” It’s funny because it’s not the ones I just bought last week, it’s the ones that I bought in November 2023 that already has $132 of interest. I could “somewhat” understand if it was the most recent ones bought in that the system just hadn’t been able to process them yet, but even that would give me pause.

As for waiting until literally the last day to buy, I don’t think 2-3 days of keeping it somewhere else is going to help you that much and risk missing the boat altogether.

Now that’s just creepy. No later after I sent this message and looked at everything once more on the treasury site did it update and give me 4.28%.

I’ve seen that before after a rate reset. There was a note about maintenanace this morning which likely included an update that addressed the missing interest rates.

Until one year passes, you may see NA because you can’t yet redeem.

The N/A is not in the latest bond purchased It is in one before the two latest in the list So no, that can’t be it.

And as Frank said it has been fixed, my rate now says 3.87%

never had a problem with the website,always been good to me.

With Treasury now announcing I-bond fixed rates on the last day of the month, how about this strategy:

1.) Buy a certificate of indebtedness (CofI) a day or two ahead of the end of month. This puts funds in the Treasury’s account so should be available for I-bond purchase without delay.

2.) On the last day of the month, buy at the current month fixed rate using the CofI funds or wait until later, depending on rates.

3.) If buying the last day of the month looks unfavorable, return the CofI funds to an account paying interest. Buy at the end of the next month or revisit the strategy 6 months later.

Cost for the optionality is the interest foregone while moving into and out of the CofI.

I am not sure this would work any better than placing an advance order for the last day, with money to be drawn from your brokerage account. Advance orders, from what I have heard, were placed on April 30. However, my advice remains: Give yourself at least two business days for your order to complete. No worries with that strategy.

Treasury direct was slow to update the information on their webpage.

Even now (well past 1 pm EST) they still say that the interest rates are unavailable for bonds purchased on May 2023

IAAAD05-01-2023Not Available $25.00 $25.85

IAAAE05-01-2023Not Available $25.00 $25.85

Also it took several hours in the AM for them to update the savings calculator for redemptions on dates between 06/2024 to 11/2024. the message was:

The following error(s) have occurred:

The Treasury Direct web site is a mess. It was created in the 1980s and enlarged over time. It is now too clunky and worst of all, provides us with occasional misinformation. It needs a complete do-over by some professional web site designers who also know about the intricacies of savings bonds. I imagine such people do not exist.

It is a pity that we can only buy and redeem savings bonds using Treasury Direct. In the old days we could buy and redeem them at most banks. For some reason, brokerages today do not want to deal with them, although they will allow customers to buy Treasury bills, notes, and bonds at auction for no commission. There are a lot of bizarre redemption rules for savings bonds when the owner has passed away, and maybe brokerages just don’t want to be bothered.

The website is pretty clunky! But then why does it apparently have 70+% “excellent” ratings in that little survey they give you at the end?

Interestingly, I received an email from Treasury this week that they’re working on redesigning the website, and to provide input.

I’ve heard from others getting this email, too. Right now, I am OK with the site because I know it so well and I know (sort of) all the ways to avoid problems. When you log in and get that 1997 look in the account pages, I am fine.

I’m pretty content with the most recent update from a couple of years ago.

When you had to type in your password with the onscreen keyboard before ~2022… yikes! I don’t remember exactly what the site looked like, but it didn’t seem like an official government website to handle thousands of dollars, except by being way out of date and neglected!

In the really old days, Treasury sent you a little card, the size of a credit card, which had info needed to log on.

It has to do with fraud and process of redemption from the bank’s point of view. They essentially have to front you the money and they go collect from the treasury- which can take ages.

has the spread between I bond fixed rate of 1.3% and long term (20+ years) TIPS real rate of 2.4% been this high in the past? what is considered a “usual” or historically average spread between these two rates?

Yes, 110 basis points is a large spread, much larger than typical. That’s mainly because 20-year TIPS real yields often were struggling to get to 1.0% for a decade and then spent a couple years below zero. If the 5-year TIPS averaged 2.4% real yield for the next six months, you’d be looking at an I Bond fixed rate of about 1.6%, I’d guess.

David, I want to congratulate you (and some Boglehead experts?) on cracking the code to predict the fixed rate for I bonds. After all these years, it appears you now know the secret formula that is unpublished by the Treasury. Thank you so much for all your dedication and sage advice provided by this website. Congratulations!

It’s progress, but I still expect future surprises from the Treasury. This 0.65 ratio has worked well since 2017, but wasn’t accurate before then. So it’s possible the Treasury decided on a new grading system. And it could change again, of course.

I think I might have screwed up my timing by not doing this in April, but does it make sense to take a 0% fixed rate I-Bond purchased in 10/2022 and redeem it this month (May) and then purchase a new one with the 1.3% fixed rate component? I know I have to pay the 3 month interest penalty. Are a lot of people doing this?

Yes it makes sense, and at least some people are doing it (including me).

In a recent article David suggested keeping the 0% rate while you build up your stash of I-bonds. However if you have all the I-bonds you want, or are fine doing the gift trick, I think it’s worth redeeming and getting a new one. You make up for the penalty fairly quickly.

The exact breakeven time span depends on your tax rate (you have to pay taxes on the interest gained from selling the Oct 22 bond), and how you invest the surplus interest if the original was a max $10k bond (as you’ll have $940 in interest from the old bond you can’t put in the new I-bond). All that said, you should breakeven around a year from now.

I did convert one set of 0.0% fixed-rate I Bonds for a regular purchase at the end of March and then another set for gift-box purchases at the end of April. It makes sense for me, because I have a lot of I Bond holdings. I will probably start working on the 0.1% I Bonds in the future, if rates stay elevated.

So, yes, it makes sense, unless you are trying to build up your total amount of I Bonds. The hold the 0.0% and buy the 1.3%.

Hi David,

Thank you for all of the information offered on your website.

I purchased quite a few I-Bonds through the gift strategy at the 9.62%. If I redeem some of them in May, does it mean that I will be penalized at the 2.96% annualized inflation rate for 3 months of interest. Thanks.

This depends on your original month of purchase, because you could still be earning 3.94%. You need to wait for three months AFTER the transition to 2.96% to get the penalty all applied to 2.96%. FYI, I will be posting on Sunday morning a look at current I Bond composite rates, for I Bonds back into history.

David,

I am still a bit confused when it comes to how the interest is presented in Treasury Direct.

The I-Bond I purchased with the issue date of 6/1/22 is showing $11,076 on 5/2/24. When I used the https://eyebonds.info/

to check the value, it shows $11,184 for May 1st. Is it because Treasury has already deducted 3 months of penalty plus the June 2022’s interest since I bought near the end of June.

Treasury is showing 3.94% interest for this bond, does that mean it’s the interest rate for the penalty or the current inflation rate of 2.96% as I had asked in my previous comment?

I try to re-read your article https://tipswatch.com/2023/08/06/the-i-bond-exit-ramp-is-now-open-proceed-with-caution/, but I still get confused with being new to the whole process. Thank you for your patience.

TreasuryDirect will never show you the last three months of interest earned until you have held the I Bond 5 years. Eyebonds.info shows the compounded interest with no penalty, so the total is higher. The 3.96% interest rate you see in the calculator is the earlier variable rate. In June you will transition to 2.96% for six months. This I Bond has a 0.0% fixed rate.

Another thing to consider: You could redeem the 0.0% I Bonds, put the money into a high-rate money market or 4-week Treasurys, and then wait until October to buy the I Bonds with the 1.3% fixed rate. You will earn more than the 4.28%, maybe, through October.

Great idea. Thank you!

I was introduced to Treasury Direct’s purchase processing style when I tried to buy some I Bonds one year on 12/31. The purchase counted against the next year’s limit.

There’s probably no hope of getting them to allocate a 4/30 purchase to April regardless of what the page says. I work for the government, so I’m used to them not standing behind what they say if they either make a mistake or later decide a change needs to be made.

Treasury Direct scores again for blatant stupidity. They say their savings bond calculator will calculate value for paper bonds, but not electronic bonds. Uhhh, aren’t they supposed to be the same?

“The Savings Bond Calculator WILL NOT: Give correct values for electronic bonds. The Calculator is for paper bonds only.“

https://treasurydirect.gov/BC/SBCPrice

This Calculator issue is strange. Yes, it gives absolutely correct numbers for electronic I Bonds, even subtracting the three-month interest penalty for I Bonds held less than 5 years. The only issue is that you must enter I Bonds in $5,000 increments (since that is the maximum size of tax-refund paper I Bonds.) I find that tool extremely useful and I hope Treasury doesn’t ditch it.

Thanks for checking the calculation. I use the “calculator” every six months to calculate my earnings for each month for the next six months. The $5,000 maximum is easily worked around. But such a bizarre statement by Treasury Direct makes the whole site suspect, although so far the numbers have been accurate. I would guess they hired some new workers and some of the older, smarter ones recently retired.

BTW, David, nice call on the new fixed rate.

The rate of 5.27 percent was available until 11:59 p.m. Eastern Time on Tuesday, April 30. The current rate of 4.28 percent became available at midnight.

Talk about a communications failure. The Treasury must have planned to use this text tomorrow, but instead announced the new rate today and someone still decided to put it on their website. They are telling the public that something was (but is no longer) available for purchase until a specific time that hasn’t yet occurred.

That past-tense wording will disappear by tomorrow, or soon after. I am assuming the Treasury was flooded with calls complaining, and rightly so, that, “You said the rate was available until 11:59 p.m.!” This past-tense wording is an effort to cover over their error. Not working.

What’s the deal with EE bonds? What is their purpose given such a low yield?

For many years, EE Bonds had a fixed rate of 0.1% but paid 3.53% if held for 20 years, while the 20-year Treasury bond was paying about 2.5%. EEs made sense then. Now, they just are not attractive.

As I’ve pointed out in comments on at least two other recent threads here, TreasuryDirect’s FAQ say that bonds will be considered issued effective as of the first day of the month in which TreasuryDirect receives the funds for the purchase. For example, place an order on April 25, TreasuryDirect receives the electronic funds on April 26, I Bond considered issued April 1.

So when TreasuryDirect says (said) that the April I Bond rates were “available” until 11:59p on April 30, that was true, provided TreasuryDirect also received the funds by that time.

But while, considered alone, that was a truthful statement, it was also sufficiently ambiguous as to still lead some people to believe they could get the April rate if they simply placed an order on April 30, regardless of when TreasuryDirect finally had their cash in hand.

I doubt TreasuryDirect is intentionally trying to mislead I Bond customers, but I do think the language of TreasuryDirect’s non-FAQ announcements on this subject could use some sprucing up–because the date of funds receipt, not the date of order, is obviously the controlling factor.

See https://www.treasurydirect.gov/indiv/help/treasurydirect-help/faq/ >>>”Purchasing Savings Bonds” >>>”If I buy an EE or I Bond at the end of the month, what issue date appears on the bond?”

Yes, the Treasury gave investors unclear instructions. For years, I have urged I Bond investors to make the purchase a couple business days before the end of the month. (I bought on April 25, for example.) Last year, the Treasury clearly stated that I Bond purchases made on the last day of the month would get the November rate, not October. This year Treasury muddied it up, for no apparent reason.

I understand the frustration, disappointment and ambiguity. But why wait until the very last day before the rate reset? Is that missed 1 or 2 days interest on 10k going to make or break you?

I agree, of course. I was recommending making the purchase on Thursday or Friday last week, “just in case.” Monday worked. Tuesday didn’t, despite the odd wording Treasury posted. Not worth testing the limits.

Dave: Have you done any recent long-form podcast(s) or YouTube on your history and the history of this site? Would make for a fascinating listen on how you got to this point.

A different perspective as to if the announcement is “early”: Any instructions entered on TD today to buy an I-Bond would have a purchase date of 5/1/2024 or later. So the announcement, I believe, is “timely” in that it gives potential investors accurate information as to the terms of their prospective purchase.

I also believe there is no risk to purchasing an I-Bond on the last day of the month as long as the instructions are entered into TD at least one business day prior. TD notes that purchase instructions will be effective “the next business day” and the effective date of the purchase is displayed on the final confirmation screen.

Certainly it might be a prudent course of action to weigh the potential consequences of things not going as expected and schedule purchases to be executed prior to the last day (in other words, “don’t wait until the last minute”). But my point is that although TD as an interface to a Treasury execution system has many, many nuances (and is sometimes unavailable when needed) — the financial aspects of it (as one would expect) are understandable, explainable, and accurate.

Anecdotally: I scheduled a purchase in mid-April to be executed on 4/30/2024 and it was executed today as expected. I also entered instructions for a purchase yesterday (4/29/2024) that were also executed today as expected.

It is strange, though, that Treasury has been saying April purchases could be made until 11:59 pm on April 30. I’ve never seen that before, and it made me think the new I Bond rate would be announced at midnight.

Yes, both can be true although they seem inconsistent. April purchases can be made through April 30, but the instructions have to be submitted prior to 11:59PM on April 29 (the business day before April 30).

As to your last paragraph: the initial order entry screen will default to the current date in the Schedule single purchase for: field, but the Purchase Date(s) message on the final page will show the actual date of purchase and has the following message: “The purchase date(s) will be on the next available business day.“

You can verify this yourself by starting a $25 gift box purchase — the first “submit” will bring you to the final confirmation page that will show an 05-01-2024 Purchase Date(s) (and from that point you can Cancel without an actual execution)

And while I did not stay up to midnight to test the 11:59PM on April 29 limit to place an order to be executed on April 30 — I would have been able to place an order for today at 10PMish last night.

I liken it to T+1 settlement of secondary market Treasury transactions. If I go right now and buy a Treasury using my brokerage account, it’s not actually mine until tomorrow (which is important for things like accrued interest). I’m not saying the I-Bond (and presumably all TD purchases) “next day” is in fact T+1, only that it’s effectively equivalent.

As I mentioned previously, I also bought yesterday and the bonds were issued today with the 5.27% rate. The key is to make sure Treasury Direct logs the purchase date no later than last day of the calendar month. You can check this by clicking the pending purchases and investments tab under ManageDirect in TD.

Once a new calendar day begins (after midnight ET), any new purchase you submit will be issued the following business day. So unless you schedule your purchase ahead of time for the 30th/31st, the last day to submit a new purchase is the second-to-last day of the calendar month.

I think that what TREASURY wished to do (and manages to succeed) is that nobody can decide wether to buy or not an I bond for the month of April (or October) knowing for sure what the fix rate is going to be for May (or November).

This is a truism, as it’s the similar as to when you decide how much to buy, if at all, T-bills at auction.

I think I did the right thing buying I bonds in April, but I am also glad that the fixed Rate has remained 1.3%.

I will wait and see how the inflation goes from April to September before committing to purchase more I bonds.

I think the best strategy (for me at least) is to hold the bonds up until you really need the money, so I am not selling any bonds with lower rates and buying new as I do not want to tie my money for 1 additional year.

I consider this Aprils’ purchase to be a replacement for an older one with a 0.0 fixed rate. I will be cashing that one out on September 1 to minimize the penalty based on the original purchase date and the new variable rate.

I’m with Bob. I think you should only hold onto old, low rate I-Bonds if you are still trying to accrue more I-Bonds.

Otherwise it’s definitely worth it to take the 3-month penalty. Whether you can risk locking up your money for a year depends on your specific situation. For me, it’s worth cashing out my 2022 bonds and getting the new rate since my May 2023 I-bonds are now freed up if needed.

I think this is a fair rate and removes buyer’s regret for purchasing earlier in the year.