These new funds offer simplicity, but with some drawbacks.

By David Enna, Tipswatch.com

Back in late September, financial adviser/author Allan Roth sent me an email pointing out BlackRock’s new offering of 10 defined-maturity TIPS ETFs. Roth, who has been pushing for more useful TIPS ETFs, called this “a step in the right direction.”

I was traveling in Greece at the time and couldn’t take a careful look. But after a quick glance, I decided that yes, these ETFs looked reasonable both in theory and in cost. The expense ratios are only 0.10%.

But I had questions: Who is the target market for an ETF that will be holding only two to six bonds until maturity? Why not just buy and hold the individual TIPS? Would these ETFs provide tax-reporting benefits in a taxable account? Are these ETFs targeted at customers of assets-under-management financial advisers (which would dramatically increase the cost to investors)?

A few weeks later, Roth wrote an article for ETF.com on the BlackRock offerings, with the subhead: “Here is why I bought all 10 of them.” From the article:

I spoke with Karen Veraa, head of U.S. iShares Fixed Income Strategy at BlackRock, about these new ETFs. She confirmed that the purpose of the new ETFs is for the investor to buy and hold until maturity. She noted that buying the individual TIPS directly can be complex with large bid-ask spreads. She also said the tax reporting is simplified with annual 1099s issued. …

I like these ETFs and asked John Rekenthaler at Morningstar to give me his views. He responded: “I highly approve of these new funds.”

By the way, Allan Roth is not an assets-under-management financial adviser. He charges an hourly fee and would not benefit financially if his clients used these iShares ETFs.

A contrary view was offered by financial author and adviser Dr. William Bernstein on a recent “Bogleheads on Investing” podcast. Host Rick Ferri asked him about the new “bullet” iShares TIPS ETFs, and after praising TIPS as an investment, he said:

The bullet shares, unless I misunderstand them, don’t make a bit of sense to me. … Why would you buy one or two bonds that mature in any given year. … when you can buy the bond yourself for zero expense? That doesn’t make any sense.

Bernstein’s reaction (which I think is sound) set off a debate in the Bogleheads forum, with contributors weighing in on both sides.

Let’s take a look

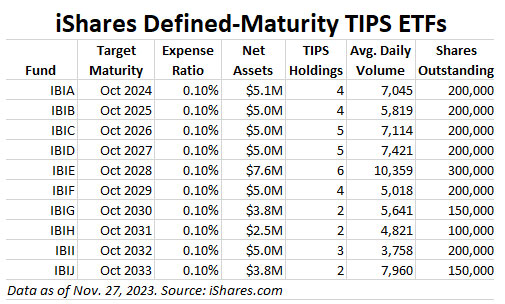

The iShares suite of defined-maturity TIPS funds offers maturities for 2024 to 2033. In other words, you buy the ETF — probably intending to hold to maturity — and then after a defined period, it distributes all proceeds and closes down.

A few things to notice right away: 1) These are extremely small funds with only about $5 million in net assets, versus $19.7 billion for the giant TIP ETF, also from iShares. 2) The number of bonds in each fund is also tiny, ranging from 2 to 6. And 3) The average daily volume is minuscule, which could create bid/ask spread problems. The TIP ETF, by contrast, trades 2.8 million shares a day.

Why do the offerings end in October 2033? Because there are no TIPS maturing from years 2034 to 2039, and then from 2040 to 2053 only a single TIPS per year trades on the secondary market. It would make no sense to create an ETF holding one bond. But I would expect iShares to launch a 2034 ETF some time next year after the second new 10-year TIPS is auctioned in July.

The limited span of maturities means these ETFs aren’t the total solution for building an inflation-protected ladder of investments to cover 20 to 30 years. Roth notes:

Though these new ETFs don’t solve a 30-year safe withdrawal rate, they could be perfect for uses such as bridging the gap while delaying Social Security by building an eight-year ladder at age 62 and waiting to age 70 to begin distributions.

What is the investment objective?

Let’s look at one of these investments, IBIE, which has a target maturity date of Oct. 15, 2028. It holds six TIPS, the most of any of these defined-maturity funds.

This ETF was launched on Sept. 13, 2023, so it has very little performance history. At this point, Morningstar has no performance data on its IBIE page. The ETF launched with a price of $25.22 and now trades at about $25.29.

iShares says the ETF is designed to mature like a bond, trade like a stock. It says: “Combine the defined maturity and regular income distribution characteristics of a bond with the transparency and tradability of a stock.”

As for investment objectives, iShares notes it could be used to achieve multiple objectives. “Use to seek inflation protection with U.S. TIPS, build a bond ladder, and manage interest rate risk.”

Is there a required minimum investment?

No. The minimum investment would be the cost of one share (around $25.29 for IBIE) plus any possible brokerage commission. There are no limits on redemptions. iShares notes there can be a bid/ask spread on purchases and sales. That seems especially likely for an ETF that trades at such a low volume. The iShares prospectus notes:

When the Fund’s size is small, the Fund may experience low trading

volume and wide bid/ask spreads. In addition, the Fund may face the risk of being delisted if the Fund does not meet certain conditions of the listing exchange.

However, even with the small volume for the IBIE ETF, iShares reports that the premium or discount to net asset value has been small, about 6 cents per share. And the median bid/ask spread has been just 0.08%.

Traders in individual TIPS face these same bid-ask issues and at times can have trouble buying or selling TIPS in small numbers. This new ETF resolves the small-lot issue, at least. You can buy as little as one share.

Income and inflation accrual distributions

One of the advantages of owning a TIPS to maturity is that inflation accruals continue to build over time, increasing the amount of principal and also increasing the semi-annual coupon payment as the principal increases. An individual TIPS gets the benefit of compounding, even though the coupon is distributed twice a year.

But one of the disadvantages of a TIPS is that if held in a taxable account, those inflation accruals are subject to “phantom” federal income taxes in the current year, even though they are not paid out. Plus, if your account is at TreasuryDirect, you will face the “dreaded 1099-OID,” the cryptic form reporting your taxable accruals.

In the past, I have written about holding individual TIPS in a taxable account. I am actually OK with that, but after retirement I switched to using a traditional IRA, where money can be raised without tax consequences. See this: “Frightened by a phantom? TIPS are fine in a taxable account, until …“

The ETF plus. These defined-maturity ETFs “fix” the OID issue because inflation accruals will be paid out in the current year, along with the coupon interest. (This is the same way traditional TIPS funds work). That distribution makes these iShares TIPS ETFs more attractive for holding in a taxable account, because it eliminates the phantom income problem.

I assume this also means your broker will provide a single 1099-DIV tax form covering both coupon payments and inflation accruals.

The ETF minus. Distributing the inflation accruals in the current year means that at maturity you will be receiving only the original par value and final coupon payment, since all the inflation accruals would have been distributed.

So to get the full benefits of compounding and true inflation protection you would need to reinvest all inflation-accrual distributions back into these TIPS ETFs or another similar product.

That could be a problem. I am not confident it would be wise to try to create a reinvestment strategy for ETFs with extremely small average daily volumes. I expect that Vanguard, for one, would refuse to do those reinvestments automatically.

For example, Allan Roth ran into a low-volume problem while building his ladder of these defined maturity ETFs:

I thought it would be a piece of cake to buy these, but I was wrong—at least on two of them. Using the Fidelity retail website, all went through except two. For IBIC and IBIF, I got error notifications that the share quantity I entered was greater than the maximum allowed.

How could buying fewer than 25 shares for about $900 be too high? I followed up with Fidelity and eventually found out I was violating Market Access Rules. Fidelity explained that the quantity I was buying was too high relative to the average volume over the past 90 days. They were eventually able to solve it for me, but I couldn’t buy the exact dollar amount I wanted.

Final thoughts: Simplicity is good

These defined-maturity ETFs look good, maybe not for me, but for other investors looking for a simpler way to invest in TIPS, especially in a taxable account. The iShares pitch is “matures like a bond, trades like a stock” and that is appealing.

In just an hour, an investor could conceivably build a “diversified” exposure to TIPS spanning 10 years, with maturities in each year. This isn’t the solution to building a long-term TIPS ladder to last through retirement, but could be used as a bridge to taking Social Security at age 70 or other specific needs lasting 10 years.

The expense ratio of 0.1% is very good, especially if you can make your trades commission-free. But I do warn against using these ETFs in an assets-under-management account, which could wipe out 1% to 2% of your annual earnings.

One other issue is the fact that these funds don’t offer true inflation protection over the long term, since they pay out the inflation accruals in the current year. That is great for people seeking cash flow. But an investor seeking inflation protection would need to figure out a way to reinvest distributions.

Reinvesting is quite simple for traditional high-volume TIPS funds like TIP, SCHP or VTIP. But the very small volumes of these iShares funds could cause problems. iShares notes: “No dividend reinvestment service is provided by the Trust” and it suggests contacting your broker to see if it can be done on the secondary market.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I’d be interested to hear your take on the new LifeX funds, another income solution which is offered in a TIPs-based version. Here is a link to an archived version of yesterday’s Barron’s article on them: https://archive.is/ZskuR

It strikes me as an interesting idea, but the 1% haircut seems steep. It does seem like it essentially turns into an inflation adjusted annuity though.

I read this article this morning and I admit to being baffled about how the fund works. And the 1% expense ratio is an alarm bell. From the site: “Distributions provided by each LifeX fund are not guaranteed or otherwise backed by an insurance company or by any third party … you may not receive monthly distributions as described, and you may lose any or all of your investment.” This is a very complicated endeavor, with about 30 funds just on the inflation-protected side. Every fund is limited to men or women born in a certain year, so the potential market is limited.

That is a _very_ good point. The limited market for a given issue could be more problematic than both the complicated structure/mechanism(s) and the 1% ER.

David asked that I report back on an issue I raised in a prior post: reinvestment of distributions from the new iShares fixed maturity TIPS ETFs. I had checked the box for reinvestment at initial purchase in a Schwab IRA, and I can now report that it occurred with the October 2033 maturity ETF (IBIJ). Schwab received what they characterized as a “dividend” on December 20 and bought fractional shares at the next day’s opening price of $25.92. There was no Schwab fee. I have not analyzed bid-ask spreads. Volume on the reinvestment date for this ETF was lower (4,200) than its average (7,453 per Yahoo Finance over an unspecified number of days). Interestingly, IBIJ’s daily volume has varied a lot over the last 6-7 weeks–between 900 and 43,400 shares/day.

Bottom line for me: reinvestment in these ETFs 1) is “routine,” at least at Schwab, and 2) should be considered forthese ETFs when the plan is to hold them to maturity. Another likely use which I have not yet done: it would be possible to invest cash distributions from one’s individually held TIPS in similarly dated iBond TIPS ETFs as a counter to reinvestment risk over the duration of the individual TIPS.

Excellent information, thanks.

I was going to ask how can they payout the inflation accrual if the fund does not receive it, just like you don’t receive it with an individual TIPS held. If they are having to sell TIPS after they have declined in value to payout the inflation accrual then it seems like a bad investment. Just own the individual TIPS to maturity and there is less risk of loss.

i have a question regarding LTPZ 15+ Year U.S. TIPS Index ETF and TLT 20 year + treasury bond ETF. both bottomed out on the price charts october 23rd. both have gone up in price quite a bit since then. the upward move looks identical in both ETF’s charts. one is deflationary the other is inflationary. how can this be happening?

Both are bond funds and the net asset value of bond funds goes up when yields — either nominal or real — go lower. Yields have been falling 30 to 40 basis points in the last 45 days, so the values of both of these funds have gone higher. These are similar funds because of their duration. No matter the inflation rate, TIPS yields tend to track higher or lower along with nominal yields, with some variations.

Larry Fink and BlackRock have moved to stakeholder (not shareholder) advocacy. That doesn’t bode well for returns. It’s OK to be woke as an individual, but not by using other people’s money.

I’m a little confused by this article’s title. Am I right that it should read “iShares” and not “iBonds”?

I actually changed the headline to say iShares (about 15 minutes after posting) instead of iBonds, but somehow it reverted back to the original. The company is BlackRock, the ETF division is iShares and its collection of bond ETFs of all types are called “iBonds.” After I posted the original article, I realized that would be confusing and so I just went with iShares. Not sure why the headline reverted back to iBonds. I personally hate that name because of the confusion it can cause with the U.S. savings bonds.

I believe the 1.3% above any inflation I-bonds are good… but the fixed rates that are currently going down as rapidly as they went up look like a better 5-year or more savings plan than TIPS… Of course, I may be very wrong… my crystal ball is fogged up as usual. I’m just not going for any TIPS bond ETF for sure. Best wishes though…

The I Bond’s fixed rate could end up being very attractive by April, I agree.

“A bird in the hand…” as the old saying goes…

Now that I am retired with a reduced income, yet an income, I was thinking of ceasing the tax return strategy for buying additional I Bonds. But now I am having second thoughts.

I personally have never done the tax-return purchase. If you like the strategy, it’s possible you’d want to do it one more time, since real yields eventually could be declining.

I’m thinking this year is a great opportunity for a tax return I Bond. As long as you file on time, you’ll get the 1.3% fixed rate. Towards the end of April, if it looks like the fixed rate will drop in May, then you can buy another $10,000 with 1.3% fixed. I have done the tax return I Bond for the last couple years, and I wouldn’t miss it this year. I still have one 0% fixed to dump though.

> from 2040 to 2053 only a single TIPS trades on the secondary market

Can you explain what you mean by that? Is it due to insufficient volume?

Because I own multiple TIPS that I purchased on the secondary market with maturity years of 42/43/44.

One TIPS per year.

Hi, David.

Based on a limited sample of one (last year was the first year I received a “dreaded” 1099-OID), at least in my experience, I did not find the level of complexity in taxes that you alluded to above.

I buy individual TIPS for my ladder via Fidelity. The end of the year Fidelity tax statement made everything very clear….it was just a matter of copying the 1099-OID data provided by Fidelity into my tax software.

Perhaps it will be more complicated when I do my 2023 taxes, but so far, I don’t perceive this as a huge drawback to an individual TIPS ladder (at least via Fidelity….I don’t know about other brokerages).

I’ve never owned a TIPS in a taxable brokerage account, so I haven’t seen their 1099 forms. I am sure they are as clear as all the others. The problem is the crazily confusing forms created by TreasuryDirect. I wrote about that earlier this year: https://tipswatch.com/2023/01/24/treasurydirect-1099s-how-to-find-your-tax-forms-decipher-them/

The complexity in taxes would be more apparent when buying TIPS in secondary market for deep discount or even a premium.

What makes TIPS unappealing in taxable account is you either have to get enough of a coupon rate/amount of interest/cash flow just to pay taxes on accrued principal in same year of accrual even though you cannot get in hand until redemption.

So if you live off of interest income or don’t have sufficient funds to pay taxes on accrued principal, then TIPS buying in taxable account can become complicated

I invested in a TIPS ETF at a time of epic inflation which continued an upward trend after I placed the trade and I promptly lost 8% of value. The best explanation I’ve heard for why this would happen is… it’s complicated…

I’m done with TIPS ETFs.

A TIPS investment is still a bond investment, and when real yields rise, the value of the underlying TIPS decreases. Real yields rose well over 200 basis points over the last 18 months, which lowered the value of all nominal and inflation-protected TIPS.

Understood. And doesn’t that defeat the purpose of buying TIPS in the first place? Zvi Bodie says that the returns on the TIPS Fund and individual TIPS should be roughly equivalent. I haven’t done an analysis, but that doesn’t appear to be the case. What is your view?

My view: TIPS can be best used to supply needed cash in the future with a series of defined maturity dates. You know you will get a safe, inflation-protected return upon maturity. With a TIPS fund, there is no defined maturity and no certainty of return on the date you decide you need to cash out. I’m more comfortable owning individual TIPS.

Based on my reading of the prospectus the target ETFs have their own complexities and potential unintended consequences.

The first is that they in fact track an index of TIPS, which is different from buying an individual security. (The investment guidelines only require 80% of the ETF to be actually invested in TIPS.) For example, the 2026 ETF currently consists of five bonds that mature in 2026. The index is rebalanced monthly; If a new TIPS maturing in 2026 is issued, it will presumably be added to the index and the ETF will need to buy that issue at prevailing yields. The prospectus reads, “The Fund does not seek to return any predetermined amount at maturity or in periodic distributions,” which is the opposite of what I want from my TIPS ladder. Another implication of the index is that with the ETF you cannot pick a particular security in the target year; for example I like TIPS that have the lowest inflation-adjusted principal because those have the most valuable protection against deflation, but others might like, for example, the lowest or highest coupon.

The second issue is the periodic income. The ETF distributes income monthly, and those distributions include both interest payments and principal inflation adjustments. The ETF may or may not have the cash income to make those distributions; if they don’t (e.g., small coupon, large inflation adjustment) they have to sell some holdings to make the payments. In addition, six months before the maturity of the ETF (not the underlying bonds) the ETF starts moving into cash and you earn a cash yield.

Third, the ETF may avoid some tax complexities, but it creates others. One is that a downward adjustment in TIPS principal due to deflation may result in having to record some distributions as “return of capital,” which reduces the tax basis used to calculate gains and losses. I don’t know whether brokerage firms are set up to report these correctly on your annual tax statements.

Fourth, while buying individual TIPS in the secondary market may incur a markup for small investors, the ETFs can trade at a premium to their net asset value. The 2026 ETF seems have mostly traded at a premium of .05% to 10%, but it spiked to .40% on October 9.

Fifth is the lack of scale. The prospectus points out several times in all-caps, boldfaced type, that this can can lead to higher tracking error, read: the fund can’t easily adjust the relative weights of the five TIPS holdings to match its target index.

I’m a fan of ETFs generally, but in this case I’m in Bernstein’s camp.

You did a nice job summarizing potential pitfalls. Some of the “issues” you raise, though, aren’t really issues. For example, no new TIPS will be issued in 2026 and so indexing is not an issue, for that year or any year up to 2029. There will be two new 5-year TIPS maturing in 2029 and then every year through 2033. Those are the only additions — two new 5-year TIPS per year. For those years 2029 to 2033 I’d expect shares will be added along with the new TIPS, which appears to have already happened for the 2028 ETF.

I think you are on target though in thinking there’s a lot to learn and discover about the way these ETFs will operate. I don’t think they are risky, but we don’t know exactly all the policies, procedures, payouts, etc.

As mentioned in the main article and the comments, a primary concern with these funds would be the low volume possibly causing poor execution or bid/ask spread.

All but one fund has more than its initial 100K shares in the market. Before buying a new ETF, I usually try to look at its characteristics to ensure that it has a low closure risk, such as looking at its issuer, current AUM, and its AUM over time. Closure could mean unexpected tax consequences.

Also, I’d want to verify how brokerages handle these ETFs at maturity. I understand that at least some brokerages charge a “reorganization fee” when an ETF dissolves, so it may make sense to sell before defined maturity bond ETFs “mature” if one’s brokerage charges such a fee.

Hard pass here. Sounds like a financial product in search of a problem. Happy holding iBonds till I need the money. Not happy with the current rate but they’re a small part of the total plan/portfolio and no tax issues until redeemed. Unrelated, but the WSJ had an interesting article last week about Goldman Sachs bailing from their attempt to become a player in consumer credit and banking. We’re the cows they’re trying to milk. This ETF seems to just be a similar effort.

These type ETFs have a weakness that is buried deep in the prospectus. You will buy your shares at a fixed price with a certain mix of bonds purchased at a certain price. Over the years bonds in the ETF are bought and sold at different prices. This dilution will cause your yield to change vs what you bought the shares at. I experienced this with other fixed maturity bond ETFs as interest rates swung 2 years ago. I went back to individual bond purchases.

I think there is a mitigating factor helping these iShares funds as opposed to larger, more complex defined-maturity bond funds. These are only holding 2 to 6 TIPS and there shouldn’t be much buying or selling to change an investment mix. But, yes, at times the funds will probably be buying additional par value or selling some to pay distributions.

I wonder if iShares will stick with these products if volumes remain so low or will they end up on ETF Deathwatch and eventually be liquidated.

It’s a legitimate concern. But if these are really intended to be held to maturity, the trading volumes should continue to be very small.

It shouldn’t matter how many TIPS they hold, if the funds grow large than $5 million each (which one would hope they would) then the real yield of the future TIPS purchases will overwhelm that of the initial ones. In other words, you’re not locking in the real yield – a huge disadvantage vs just buying TIPS directly.

I think your comment and many of the others raise the potential pitfalls in investing in a new product with zero track record. We really can’t be certain exactly how it will perform. When you buy an individual TIPS, you buy certainty of a return over inflation when held to maturity.

How can these funds pay out the inflation accruals on an annual basis without selling the TIPS in the fund to realize the gains?

I am not sure of the process, but I am assuming that the fund would need to sell some TIPS to cover the inflation accrual. In most years, that would be about 2% to 3% of the total, but the market value could vary. I believe these funds will have quarterly payouts. The TIP ETF generally pays a monthly dividend that covers the inflation accruals, but with a giant fund that isn’t a problem.

From the IBIE prospectus: “…the Fund may be required to make annual distributions to shareholders that exceed the cash it has otherwise received. In order to pay such distributions, the Fund may be required to raise cash by selling portfolio investments.”

The IBIE prospectus notes that distributions will end in May 2028 and will be invested as a cash position until the final payout in October 2028.