By David Enna, Tipswatch.com

The Treasury on Thursday will offer $20 billion in a reopened 5-year TIPS, CUSIP 91282CJH5, creating a 4-year, 10 month Treasury Inflation-Protected Security.

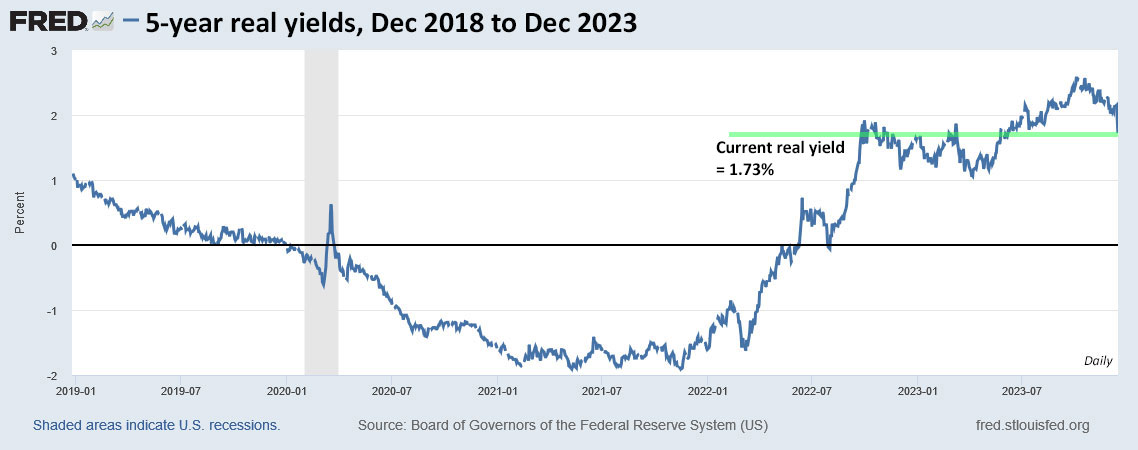

The TIPS to be reopened, CUSIP 91282CJH5, trades on the secondary market and could have been nabbed by investors just a month ago with a real yield to maturity of 2.37%. At Friday’s close, according to Bloomberg Yields Curve, that yield has now fallen to 1.73%. That’s a drop of 64 basis points in one month. Incredible.

And continued volatility is likely next week, right up to the auction’s close at 1 p.m. EST Thursday.

How attractive is this TIPS?

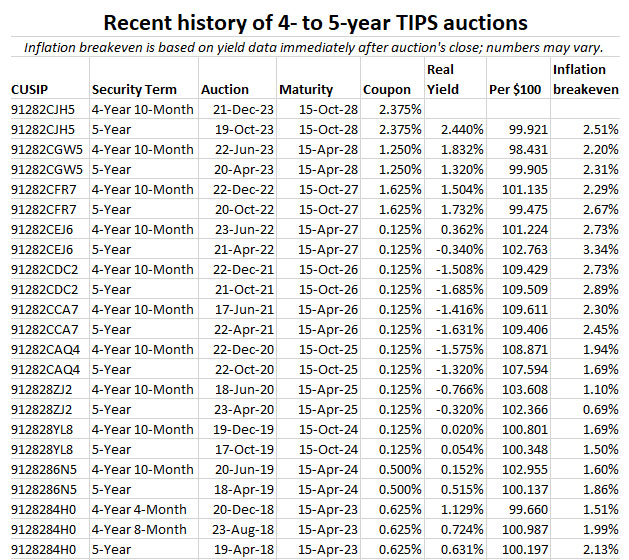

While a real yield of 1.73% seems suddenly disappointing, it is still attractive by historical standards. It could be the third or fourth highest yield for any auction of this term going back to October 2008, 48 auctions ago. Just look at the auction history for 5-year TIPS over the last year:

- Dec. 22, 2022, reopening, real yield of 1.504%

- April 20, 2023, new issue, real yield of 1.320%

- June 22, 2023, reopening, real yield of 1.832%

- Oct. 19, 2023, new issue, real yield of 2.440%

A real yield of 1.73% fits into this mix, but of course we’d all love to have bought heavily on Oct. 19 when the above-inflation yield hit 2.440%. (If you recall, this was actually a disappointing result for many investors. How times have changed!)

Here is the five-year trend in the 5-year real yield, showing that the current yield remains attractive by comparison to years of severely depressed rates:

Pricing for CUSIP 91282CJH5

If we assume that this TIPS will auction with a real yield of 1.73% (things will change, but let’s assume) then it will get a price of about 102.98, according to the Bloomberg data. Why so high? Because this TIPS has a coupon rate of 2.375% — set by that Oct. 19 auction — well above the current market real yield. It will also have an inflation index of 1.00453 on the settlement date of Dec. 29.

With that information, we can speculate on the pricing, using a purchase of $10,000 par as an example:

- Par value: $10,000.

- Adjusted principal on settlement date = $10,000 x 1.00453 = $10,045.30

- Cost of investment = $10,045.30 x 1.0298 = $10,344.65

- Plus, accrued interest, probably about $49.

So, in summary, an investor purchasing $10,000 par at Thursday’s auction will pay about $10,345 for $10,045 of principal and then receive inflation accruals and a coupon rate of 2.375% through the maturity date of Oct. 15, 2028.

This is a similar price to what you would pay on the secondary market, of course. On Saturday morning Vanguard was showing an ask price of 102.98 and a real yield of 1..73%, right in line with the Bloomberg data. But come Monday, things will change.

Inflation breakeven rate

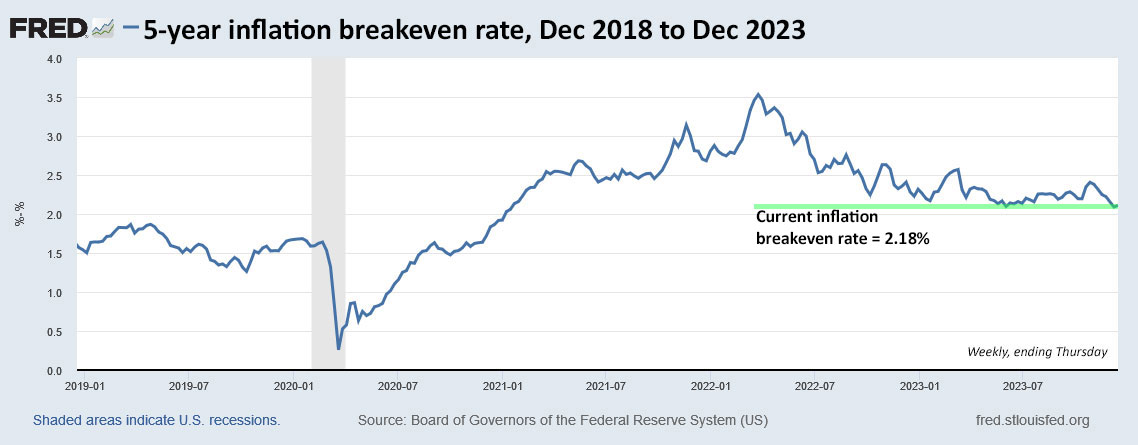

With a 5-year nominal Treasury yielding 3.91%, this TIPS currently has an inflation breakeven rate of 2.18%, well below recent auctions of this term. That is a plus for investors. It means this TIPS will outperform the nominal Treasury if inflation averages more than 2.18% over the next 4 years, 10 months. Over the last 5 years, inflation has averaged 4.0%.

Here is the trend in the 5-year inflation breakeven rate over the last five years:

Final thoughts

I won’t be a buyer because my TIPS ladder is fully loaded with 2028 maturities.

I know from feedback from readers that this particular TIPS won’t be attractive to many, either at auction or on the secondary market. Why? Because it will carry a premium price and additional principal. And a lot of investors don’t find that appealing. Does it really matter? Probably not. And sitting on the sidelines could just mean facing lower real yields in the near future. It’s a dilemma.

In the last two days, I have been tempted to say that the bond market is over-reacting to the Fed’s potential actions. The Fed, in theory, will cut short-term interest rates by 75 basis points next year. (The market thinks the cuts will be much more substantial.) The Fed is NOT launching quantitative easing and in fact will continue tightening through 2024 by reducing its balance sheet.

Future short-term rates shouldn’t have a great effect on current mid- to longer-term Treasurys. The 10-year TIPS yield has fallen 35 basis points in four days. Why? That is a real question for the markets to consider.

Plus, the Treasury next year will continue ramping up auction sizes. In fact, Thursday’s reopening auction is for $20 billion, the highest in history for an 5-year TIPS reopening. Consider this: As of this week, the U.S. public debt stood at $33.8 trillion. One year ago it was $31.3 trillion. That is an increase of 8%. How far can Treasury yields really fall?

So the Treasury market has a lot to work out. Meanwhile, I will be posting the auction results soon after the 1 p.m. ET close on Thursday. Here’s a history of recent auctions of this term:

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Thursday’s premarket shows real yields heading lower: 1.69% for this TIPS at 8:25 a.m.

Wednesday pre-market update: CUSIP 91282CJH5 is trading with a real yield of 1.71% and a price of 103.06.

Mr. Enna, On December 10th you wrote “Since Nov. 1, both the the 5-year and 10-year TIPS yields have averaged about 2.2%, which at this point would equate (possibly) to an I Bond fixed rate of about 1.3% to 1.4%.” . Of course the 5 year TIPS is now around 1.77 but can you please explain the equivalency point you mentioned above. It will help me decide if I should buy in this auction or just buy I Bond in January.

Thanks for educating us about TIPS and I Bonds.

In this calculation, I simply take the Treasury’s 5- and 10-year real yield estimates from Nov. 1 (the last reset) to today. You can download a .csv file of that data from this page: https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_real_yield_curve&field_tdr_date_value=2023 …. As time goes on, if the current trend continues, this average is going to slide lower and lower toward the current 1.75%.

Once I have the average number, I apply a ratio of 0.65 to that number to get an estimate of the likely reset of the I Bond’s fixed rate. This is NOT an official formula, just an estimate.

I absolutely do NOT wish to start, or engage in, any kind of political discussion here.

But considered just in terms of financial safety and future expectations, does anyone else fret that the issuer of all the bonds covered on this website is $33 trillion (i.e., 33 million million) in debt, with that amount growing steadily larger every year?

I keep buying I Bonds, but I’m also nagged by the thought that, in some future year, a lot of people, myself included, are going to be left wondering, “What on EARTH were we thinking?”

It’s a problem, but I do believe the U.S. will pay back investors in I Bonds and Treasurys. If it doesn’t, big problems for all assets.

I agree that there would be nation wide problems much greater than the loss of our money. Still, to know that the U.S. debt to GDP is greater than that of Argentina seems impossible, but that is what I am seeing.

U.S. Debt:GDP 129%

Argentina Debt:GDP 79%

Different economies. Different positions on the world financial stage.

Demonstrating the skillful use of hyperinflation to manage government debt?

Right, Argentina accepts hyperinflation as a consequence of their solution to managing government debt. The U.S. is right there with Japan, Greece, Singapore, Spain.

I believe that there will be an inflation rebound. The nice thing about I Bonds is that we can liquidate them at anytime after the first year, and we always have 6 months to determine if we want to buy them or if there is a better investment to purchase at the time.

I don’t have much of an understanding of these things, but I think that a big difference is that the US can easily sell its debt. The EU probably could, to some extent, but doesn’t want to play that game and I don’t know if any other country or blocs could at this point. Nevertheless, I think it is a dangerous game to play.

Don’t forget their previous defaults and the resulting higher interest rates they have to pay as a result.

I frequently see references to “the Fed easing” and “the Fed tightening.” Can you explain in simple terms which of these Fed actions leads to higher TIPS real rates and which one leads to lower rates? Thank you.

When the Fed eases, it basically does two things: 1) lowers short-term interest rates, and 2) begins buying Treasurys of all types, including TIPS, which basically is creating money. Easing will cause TIPS real yields to fall, even to levels well below zero, as we saw much of the time from 2011 through 2020. When the Fed tightens, it raises short-term interest rates and sells off its stockpile of Treasurys. This tightens the money supply and causes real yields to rise with less demand for Treasurys, since the Fed is not longer swooping in and buying all the supply.

I’m buying a little at this auction. Rationale is that the fixed rate is better than the i-bond fixed rate. (And I have enough I-bonds that I don’t need the liquidity). Given that my investment portfolio statement calls for holding some inflation-protected bonds, this appears to be the best option currently available. Duration is 5 years. Seems to fit with all my t-bills too, adding some duration.

Deep regrets about October of course! ☺

“ Over the last 5 years, inflation has averaged 4.0%.”

While factually accurate, I wonder if this is a fair representative sample since inflation spiked in two of those years up to 9% due to pent up demand, the pandemic reopening, stimulus spending, and supply chain issues.

Although we can’t predict inflation, the historical average is a bit lower than that, the downward trend from 9% to 3% is clear, and interest rates are starting to follow suit. Economists are predicting 2% inflation in 2024. If you’re in the fixed income market, 8, 13, 17, and 26-week T-bills are still earning an annualized rate of 5.4% and the 2 Year T-Note is still above 4.4%. Those seem reasonably attractive.

If you believe inflation will remain at that 4% average over the next five year period, an I Bond getting 1.3% fixed above thar with all its other liquidity and tax deferred advantages seems like a good bet, not as great at 2% though. As for this 5 Year TIPS reopening, the change in the last month is striking and seems a lot less attractive, but that might be recency bias.

Sure, you can make that argument. But if you look back at inflation breakeven rates over the last two decades, you rarely saw a number higher than 2.5%, and inflation surged to 9.2%. Inflation over the last 10 years has averaged 2.8% and over over 30 years, 2.5%. A few years ago (2016), after years of extremely low inflation, you would have seen numbers like 1.3% for the 5 year and 1.8% for the 10 year. The real question is: Have we entered a new era of higher inflation — even slightly higher? I doubt inflation will average more than 4.0% over the next five years, but it could easily be somewhere near 3%.

My guess is the average inflation, for the next 5 years, to be between 3 to 3.5%, representing a new normal, though the front end (up to 2 years) of this five year period will see around 4% inflation, because of the sticky services inflation. IMHO, Fed’s mandated focus on inflation should not be underestimated, Powell does not want to repeat the mistakes of Arthur Burns, Fed chair from 1970 to 1978

Given the above belief, I will mostly stay with T-Bills while keeping an eye on 2-3 year notes. Yes, it does require active management by me. I have nothing better to do…:)

I pay attention to climate change. I suspect that will be the black swan that will upset the 30 year average inflation rate.

Ex. rice prices are at 15 yr high.

Even Federal Reserve Chairman Jerome Powell said in 2021 that climate change risks the world economy and that, “there is no doubt that climate change poses profound challenges for the global economy and certain the financial system.”

If I may use a baseball analogy, I strongly believe that services inflation is just getting warmed up in spring training. We haven’t seen the regular season yet, never mind the World Series. The next 2-3 years are going to dish up nasty surprises (already baked in the cake) even if the US economy stagnates (since for various reasons beyond the scope of this site, productivity is now locked in a box). I feel sorry for Mr. Powell and the other members of the Federal Reserve, as they’ll be powerless to influence or direct things in any way, shape, or form.

It does feel like the treasury market has overreacted, especially given Powell’s caveats and the subsequent (albeit mild) walk back by the Fed vice chair. Add to that, services inflation is still running hot and the huge and growing federal debt that David discussed. I suspect we will see yields rise gradually from this low point.

I have about two-thirds of my 10year ladder funded. I’m going to wait before filling in the rest.

Sometimes, we get lucky – other times, we are late to the party!

But there is always some opportunity or other in FIXED INCOME other than TIPS and TREASURIES where you get the YIELD dictated by MARKET – supply/demand including TUG of WAR between BULL-BEAR speculators moving yields one way or other.

IF current yield is important one can stick to T-BILLS which also has the state and local tax-free advantage that boosts return…………if one wishes to have a higher current yield and with a chance for a longer duration, one can consider CALLABLE CD’s available in brokerage firms like Fidelity, Schwab etc. For example, you can get for 5% yield 5 year CD’s with NO CALL PROTECTION and a call date 6-9 months out onwards hoping they won’t call and spread money between similar issuers with similar yields.

the trade-off is IF it gets called, then one will perform LESS BETTER than 6-9 month T-bills that are giving STATE-TAXFREE yield of 5.3+%.

Likewise, one can also buy Agency bonds / GSE’s 5 years or less like Federal farm credit bank (brokerage firms have new issues every day) that are also STATE TAX FREE, rated on par or better than US Government debt (AA+/AAA issuer/issues) but these do not have the backing and guarantees such as US Government debt.

Also, CD’s and AGENCY bonds are NOT LIQUID and the BIG FISH takes advantage when you try to sell it before maturity if need arises. For example, if current market for 5 years is at 4.3%, when you sell your agency bonds, you will have to GET BIDS from dealers and they will discount your bonds so much where they will get a YIELD of 5.3% on it! So that is the thing one must know about.

HIGHLY LIQUID I-bonds are always an option if inflation is a concern but the dollar amount you can buy may be be too little if you have more money to invets than 10k

Agree the market overreacted, Bought my first tip in Oct- 5 yr. Beginner’s luck. Unfortunately, it was a timid beginner and I just barely dipped a pinkie in. No matter. Thanks to this site, I learned enough to try it. Thanks!