For investors seeking safety and inflation protection, volatility brought strong opportunities.

By David Enna, Tipswatch.com

All things considered (financially speaking, that is) 2023 was a pretty good year. Maybe even very good.

The U.S. inflation rate dropped from 6.4% in January to 3.1% in November. The S&P 500 index rose a sweet 23.9% before dividends, dishing out a total return of 26.2%. The total bond market had a total return of 5.7%, following a disastrous -13.1% in 2022.

And 2023 was also a good year for investors looking for safe returns in Treasurys, money market accounts and bank CDs. The 13-week T-bill started the year at 4.53% and ended it at 5.40%, offering a solid year of high yields.

A combination of moderately-high inflation and recent declines in real yields also created a decent year for funds invested in Treasury Inflation-Protected Securities. The broad-based TIP ETF had a total return of 3.81%, and the shorter-term-focused VTIP came in at 4.62%.

Good news. Also, I have something positive to share, but you have to read to the end of this article to find out what it is.

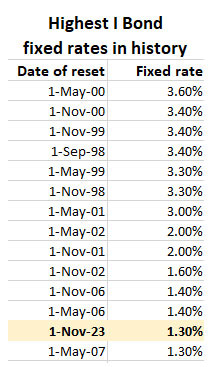

I Bonds make history

The U.S. Series I Savings Bond started the year with a fixed rate of 0.4% and a composite rate of 6.89%, annualized for six months. The variable rate at that time was 6.48%, the 3rd highest in the history of this investment. That’s a very attractive return, but things were about to get better.

On April 28, the Treasury announced that the I Bond’s fixed rate would rise to 0.9% for purchases from May through October. The composite rate fell from 6.89% to 4.3%, but with I Bonds, a higher fixed rate is always the more-attractive option since it stays with the investment for up to 30 years.

And then on Oct. 31, Treasury set the I Bond’s fixed rate at 1.3% for purchases from November 2023 to April 2024. The composite rate rose to 5.27%. While this wasn’t the highest I Bond fixed rate in history, it was the highest since November 2007, 16 years ago.

At the time, it looked like the I Bond’s fixed rate could continue rising in 2024 as the Federal Reserve continued raising short-term interest rates. But then, in November and December, the Fed made clear that the rate-hiking cycle is over and interest rates are likely to begin falling (gradually?) in 2024.

On Oct. 31, just before the last I Bond’s fixed rate reset, the 10-year TIPS had a real yield of 2.46%. Now that has fallen 74 basis points to 1.72%. If real yields were able to hold steady at this level, it’s possible that the I Bond’s fixed rate could fall to just 1.2% or so on May 1. But the next reset is likely to be lower than that.

This means that the 1.3% fixed rate on the I Bond could have marked a high point. It is a historically attractive rate and makes I Bonds an attractive investment through April. I will be writing an I Bond buying guide in early January, and will provide more thoughts then.

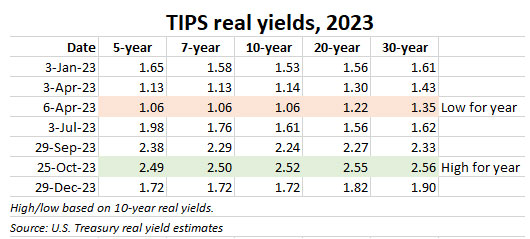

A volatile, but good, year for TIPS

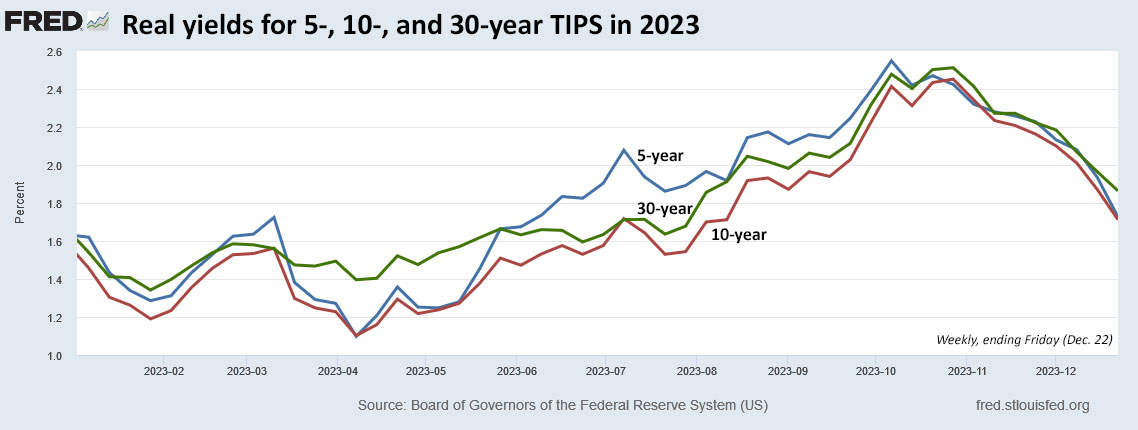

Real yields (meaning yields above U.S. inflation) had a rather wild ride in 2023, as shown in this chart:

Beginning in August, I tried to emphasis that we had entered a fantastic period for building a long-term TIPS ladder to provide inflation-protected cash well into retirement. I was fairly aggressively adding to my investments in late August and September, a bit before the October high but mostly hitting my target of real yields above 2.0%.

At this point, my TIPS ladder is complete, but I am still looking to buy the new 10-year TIPS at auction on Jan. 18, 2024. By doing that, I can fill the missing 2034 rung on my ladder.

Here is the year-long trend in real yields for TIPS, showing how yields dipped in the spring (especially for the mid- to long-term), rose dramatically and flattened out through October, and then tailed off to end the year at levels at bit higher than they began the year:

Let’s look back at the year in newly issued TIPS:

CUSIP 91282CGK1, 10-year TIPS

- Originating auction on Jan. 19 with a real yield to maturity of 1.220% and a coupon rate of 1.25%.

- Reopening on March 23, with a real yield of 1.182%, the lowest for this maturity at auction in 2024.

- Reopening on May 18, with a real yield of 1.395%.

Throughout most of 2023 and even continuing today, the real yield of the 10-year TIPS has been the lowest — or near lowest — on the TIPS yield spectrum. Not sure why. The 5-year and 20-year yields have consistently been higher.

CUSIP 912810TP3, 30-year TIPS

- Originating auction on Feb. 16 with a real yield to maturity of 1.550%, the highest auction yield for this term since June 2011. The coupon rate was set at 1.50%.

- Reopening on Aug. 24 with a real yield of 1.970%.

A 30-year TIPS is a highly volatile investment. Even though the February auction got a historically high real yield, the market value of this TIPS plummeted in the months ahead as longer-term real yields soared.

As of today it is trading with a real yield of 1.90% and a price of about 91.09, a drop in value of about 7.8% since the originating auction. But things were much worse in late October when the 30-year yield hit 2.56%.

CUSIP 91282CGW5, 5-year TIPS

- Originating auction on April 20 with a real yield to maturity of 1.320%, which at the time I called an “attractive result.” (Things would get much prettier later in the year.) The coupon rate was set at 1.250%.

- Reopening auction on June 22 with a much higher real yield of 1.832%.

Real yields hit their 2024 low in April and then began climbing through October. The April auction, in hindsight, ended up being “just OK.”

CUSIP 91282CHP9, 10-year TIPS

- Originating auction on July 20 with a real yield to maturity of 1.495% and a coupon rate of 1.375%. A bit disappointing at a time when real yields seemed to be trending higher.

- Reopening auction on Sept. 21, with a real yield of 2.094%. Much better!

- Reopening auction on Nov. 21 with a real yield of 2.180%.

By the fall reopenings, CUSIP 91282CHP9 ended up being one of the most attractive TIPS offerings of the year, but investors could have gotten higher yields by buying in the secondary market in October, when the 10-year real yield soared (briefly) to 2.52%.

CUSIP 91282CJH5, 5-year TIPS

- Originating auction on Oct. 19 with a real yield to maturity of 2.440%, setting the coupon rate at 2.375%. This auction hit just as real yields were surging, so it ended up being a highly attractive investment, despite some confusion by investors.

- Reopening auction on Dec. 21 with a real yield 1.710%, down a whopping 73 basis points from the originating auction two months earlier.

These two TIPS auctions demonstrate the dramatic effect of the “Fed pivot” in early December, which sent both nominal and real yields tumbling lower.

Final thoughts

I am happy about the financial events of 2023, which gave me the opportunity to stash away “emergency” cash in high-yielding T-bills and also to build out my TIPS ladder to 2043. Many of those investments had real yields at or above 2.0%, which didn’t seem possible just a few months ago.

For TIPS, this was the year of the secondary market, allowing purchases across the yield spectrum when prices looked attractive. Because real yields rose so high so quickly, it was a time for action, not sitting on the sidelines.

What is your reaction to the volatility of 2023 and the “unknown future” coming at us in 2024? Post your ideas in the comments section below.

Now, the good news …

I have been writing Tipswatch for nearly 13 years (hard to believe, huh?) and for much of that time my focus was more on posting articles on SeekingAlpha.com, where the pay was … er … “decent.” Then SA slashed its payments in November 2020 and I refocused on this website, with advertising supplying the income.

- In 2020, Tipswatch.com got 75,008 page views.

- In 2021, page views rose to 322,154.

- In 2022, that number rose to 992,631.

- In 2023, the number is 1,515,496 as of Dec. 29.

For me, surpassing 1 million page views was a personal goal for 2023, and I ended up breaking through that number by September! One of the great things about this site is the growing community of readers who participate in the comments section and offer tips, opinions and help. (This site received 2,769 comments this year.) Plus, you often quickly point out my errors. Thank you!

I have been lucky, I admit. It quickly became apparent in 2022 that U.S. inflation was surging to 40-year highs and then suddenly the I Bond was paying 7.12% and then 9.62%. Interest in inflation protection was HOT. In the last two years I have been I interviewed by the Wall Street Journal, Washington Post, Detroit Free Press, Marketwatch, CNBC, Barron’s, Money.com, ProPublica, NPR, Kiplinger’s, the AARP Bulletin and others.

Interest in inflation protection remains high, but not quite at the blazing pace of the past year. So maybe 2024 will be a bit more calm. Then again, I think I Bonds could have one more surge of interest before the May 1 reset. That will be fun.

Have a great holiday weekend, everyone!

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I just cashed $10k of iBonds bought at the end of August, 2022, and the interest was $880. I calculate that at about 6.6%. is that right?

OK, the actual gain was 8.8% obviously. You gave up interest for November, December and January. I am figuring your annualized interest over 16 months was 6.3%.

David, I have long term IBonds that I want to pay taxes on this year. Is the first money out the interest portion? For example, 10k investment, current value 30k, a 20k withdrawal would be all interest with taxes on 20k due this year? Thanks.

Pat, you cannot just pull out the interest; a portion will be principal and a portion will be interest.

For anyone with savings bonds, this book is indispensable: Savings Bond Advisor by Tom Adams. While it was last updated 2007 (the author may now be deceased?) most of the information is timeless.

You can find it used at many online vendors.

This info comes courtesy of Amazon (NOTE: the website is no longer accessible; this site of David’s is now my go-to site. No wonder his readership has blossomed. Thank you David for all your hard work. And thank you to the many people who comment — I have learned a lot.) . . .

Savings Bond Advisor will introduce you to the Cinderella of investments, the U.S. Savings Bond. Financial pundits have neglected the Savings Bond for a generation. Meanwhile, millions of Americans have invested significant portions of their money in Savings Bonds. Savings Bonds have been dressing for the ball since the U.S. Treasury introduced the inflation-protected Series I Bond and online accounts at Treasury Direct. After a weekend reading Savings Bond Advisor, you’ll understand how Savings Bonds work, how to open an account at Treasury Direct, the history of inflation, and why the Series I Savings Bond – which protects you from the risk of default, the risk of inflation, the risk of capital loss, and comes with tax advantages – should be the foundation of your savings and investment holdings. Everyone should have a part of their investment portfolio in readily-available emergency funds. I bonds are an easy choice for this low-risk portion of your investment portfolio. If you already have an investment in Savings Bonds, you’ll learn investment strategies that will increase the value of your holdings, estate planning strategies that will save your family money, and tax strategies that will help you avoid the Stinker Bond Penalty, the Double-Taxation Trap, the Deferred-Tax Time Bomb, and hidden interest-rate penalties. You’ll also find out that some older Savings Bonds are a bad choice for almost every investor and what to do if you own one. The book includes access to a web site, http://www.savings-bond-advisor.com, that has the latest information about Savings Bond interest rates and program changes, as well as links to the forms you need to settle estates, replace lost bonds, update bond registrations, and receive the Savings Bond college education tax-deduction. Tom Adams, the author of Savings Bond Advisor, also answers questions from the book’s readers on the web site

Kris

Mr. Adams also used to maintain a blog/website as well. In many ways it was the precursor to this site. He abruptly stopped adding to the site, must have been around 2007, when Savings Bonds became less attractive as investments. I remember he stated that he had answered every question about the mechanics of Savings Bonds and his job was basically done.

Congrats on the 1M views David, and please keep up the great work. We all appreciate it. Happy New Year!

David, Thanks for an excellent recap of the world of TIPS. As you know, I remain bullish on TIPS and described why in my SeekingAlpha article series. Earlier this year I completed my TIPS ladder. It, along with Ibonds bought decades ago comprise 25% of my all weather portfolio. They are a key contributor to my modest capital preservation return goal of about 5.5% per year (as someone who is a conservative, older investor). Wish I had captured more of the 2-2.5% yields that we may not see again for a long time. But 1.7% above inflation is still attractive IMO.

Congrats on your well deserved success on this site! Impressive stats. I gain great insights and value from your work. Wishing you all the best for another successful 2024.

Ralph Wakerly

Thank you, Ralph! Just a year ago you helped me out on a well-received article for this site: “TIPS funds vs. TIPS ladder: An investor weighs in” … Still good advice in 2024 https://tipswatch.com/2023/01/08/tips-funds-vs-a-tips-ladder-an-investor-weighs-in/

Hi David, late last year an aunt passed away. Not only am I the executor of her estate but am also an heir. Her investments include I bonds purchased mostly from 1998 through 2003 with a face value of $75,000. Because she never married there is no co-owner on these bonds. Is it allowable to pay the income tax on bond earnings from estate cash funds from the purchase date through to the date of death and then have the bonds put into my name until their expiration date in a few years. Or must they be redeemed losing the last few years of the 3%-plus fixed rate?

Great question, but way beyond my expertise. Too bad she didn’t name a co-owner or beneficiary. Your solution seems sensible but you’d need advice from a CPA or estate lawyer, I think.

I’m no estates expert, but I think the basis of those I-bonds should be stepped up to their value on the date of death. No reason to redeem them if you don’t have to, just transfer them to her heir(s). I recommend using a CPA experienced in estate tax returns to prepare the estate’s final tax return and advise you on questions like this.

According to Kiplinger’s Tax Letter, my answer above is wrong. You can elect to have the accumulated pre-death interest included on the estate’s tax return, or include it on your tax return when you redeem the I-bond. A CPA can figure out which is most advantageous to you (the estate may have deductions that could reduce or eliminate the tax on the accumulated interest on the I-bonds)

Here is information from the IRS, under the section decedents, which appears to back up your idea for paying taxes up to the date of death:

https://www.irs.gov/publications/p550#en_US_2022_publink10009922

When my father passed away he had a large stash of paper and electronic savings bonds (I and EE series) that had not reached maturity. Paper bonds can be converted to electronic form and transferred to a co-owner or beneficiary without having to be redeemed. They continue earning tax-deferred interest until the original maturity date in the beneficiary’s name. Treasury Direct reissued the bonds in electronic form less than six weeks after we sent them via registered mail. The process was relatively fast, but it helped that we included a cover letter with names of any Treasury Direct representatives we spoke with on the phone. We also included a detailed list of all paper bonds and serial numbers.

If you have paper savings bonds, be sure to include Form 4000, which requires an official bank stamp and signature (medallion signature not required even though it says so on the form): https://www.treasurydirect.gov/forms/sav4000.pdf

If your aunt’s savings bonds were already in electronic form, you will need to submit Form 5511, also with a bank signature: https://www.treasurydirect.gov/forms/pdf5511.pdf

For savings bonds without a named co-owner or POD designation, you will need to submit form 5536: https://www.treasurydirect.gov/forms/sav5336.pdf

Had a similar situation when my Mom passed away a couple of years ago. For us, the best deal was to pay accumulated income tax up to the 1st of the month of her date of death. This was made part of her personal income tax for that year. The bonds were still held in her estate until they hit 30 year maturity several months later. While in the estate, any interest accumulated goes on her annual estate tax return.

You should be able to retitle the I Bonds in your name through the probate process. Will not need to sell and lose that great fixed rate.

What do you think about TipsLadder.com to create a TIPS ladder? I’m new to TIPS and retirement. In my mid-sixties, with a small iBond portfolio and T-bills aplenty (mostly 4 week to 3 month) I’m considering locking in a TIPS ladder to provide $20,000 income per year. Based on my reading, it appears if I’m going to do this, the sooner the better due to probability of lowering interest rates. Do I have that right? I’m also considering a portion of my bond allocation to be in long term nominal bonds, and municipal bond funds because I’m in high state tax bracket and figure diversification is good. If anyone cares to chime in, thank you.

TipsLadder.com is an excellent tool. Read the instructions carefully. Depending on when you want the ladder to end you will need to bridge the gap from 2034 to 2039 when there are no TIPS on the secondary market. However, a new 10-year maturing in 2034 is coming Jan. 18.

There is no way to know where real yields are heading. Most people are guessing down, but there are factors like the huge U.S. deficits that could keep yields high. Right now real yields are in the 1.75%+ range, which I think is still attractive. I also mix some nominal Treasurys and CDs into my holdings, all maturing within 5 years.

Thanks for your reply. Forgot to add: thoughts on building out 30 year, 20 year, 10 year? There’s longevity in my family, so I figured 30 year. My understanding is if I needed more money sooner, I could sell these bonds, which I understand can be volatile, so perhaps at loss of principal. In my case, is it recommended to buy ladder at one time, using secondary market along with upcoming 10 year Tips auction?

Donna, I built my ladder out out to 2043, when I would supposedly be 90 years old. This is a highly personal decision. My wife has an entirely different set of investments (no inflation protection) so in combo we are very diversified.

Great review of 2023! Congrats on 1m+ views. Re I-Bonds: while 1.3% fixed rate might be a high for now, it looks like real rates are likely to be in the 0.5-1% range for the near term. Hopefully 0% fixed rates on I bonds and negative rates on TIPS are behind. The 0.5-1% I bonds are generally very competitive rates and should match the return of rolled 5 year CDs with all the additional benefits.

David, Love your work, which has made me more comfortable purchasing TIPS. However, I am wondering if you can help elucidate the one key question no commentator I can find has addressed: What combination of market forces drives real rates? Another way to ask the question might be: Who sells inflation protection (apart from the US Gov in their auctions)? For real rates to explode higher as they did during the latter half of 2022, there must have been significant selling of inflation protection. By whom and why? Thanks for any insight.

Real yields usually track along with nominal yields. When yields on nominal Treasurys rise, real yields also rise. The gap is the inflation breakeven rate. In 2022, both nominal and real yields surged higher as the Federal Reserve raised short-term rates and began letting its balance sheet decline. (In the 2020 to early 2022 era, it was aggressively buying Treasurys, forcing yields down.) Plus, foreign investors (like central banks) were buying less U.S. debt. Plus, the U.S. was running very high deficits, meaning more supply to buy up.

Well, if it were that simple the historical inflation breakeven line would be much flatter than it is, right? https://fred.stlouisfed.org/series/T10YIE

Sure, inflation expectations are constantly changing and that does effect the real yield versus the nominal yield. But notice in that chart that inflation expectations almost never hit 3.0%, even though the 10-year inflation average was above 3% for all years ending in 1976 to 1998. So in reality the inflation breakeven rate is fairly flat as the market continues to dismiss the potential of future inflation.

I had the same reaction to David’s previous response. In this response, David makes another important point about inflation expectations having stayed under 3%. However, the situation at hand, right now, is the possibility of the Fed prolonging “higher for longer” narrative while the “surprise” decline in inflation continues or accelerates. This will take the real rates higher, fast, unless the Fed also acts fast. As always, the next 2-3 economic data will tell us a lot about how it plays out for the rest of the year (really?, noooo). I guess, managing transitions from rate increases to pause to cuts is not easy.

Specifically, I-Bonds with 1.3% fixed rate feels like peak for this cycle. I will buy for my and my wife I-Binds as soon as I feel a bit more clarity from the upcoming 2-3 economic data releases. I am also looking forward to long-terms (7+ years) nominal US Treasury rates to go up, so that I can lock in risk free income. These rates may go up because of the continued debt driven supply of the treasuries and strong economic growth (driven by AI fueled productivity…sorry for my technology bias….yes, both my wife and I are borderline nerds….:))

Sounds like a good argument for buying TIPS! Is there a publicly available resource for charting the total return over time of each issued TIPS?

Eyebonds.info is the best source for this; just be patient in deciphering the information: http://eyebonds.info/tips/tipslist_mat.html

The volatility in the inflation breakeven is most obvious when you run the FRED graph at it’s max duration (which starts late ’03/early ’04)

David, this may be a little off topic and I know you are not a tax/financial advisor, but I think many of us might be interested in your thoughts about the tax implications and the strategies surrounding redemption of I Bonds acquired in the late 1990’s and early 2000’s with high fixed rates and when the limit was $30k (with many of us holding purchases in both spouse’s name and in back to back years). For example, does it make “cents” to hold to maturity and just pay the tax then; would it be better to do early redemptions; can you start paying the tax annually before maturity if you did not make the election initially; or something else all together? Thank much, PFM

It’s a great topic and a dilemma I am also facing. But the tax hit is still 5+ years away. It is something I will write about in the future, I hope.

Watch out for the IRMAA Medicare surcharges if redeeming lots of I Bonds in a single year, especially if you are single.

Paul, I suggest you first determine the current interest accrued for your I-bonds for each year they mature. That will give you a feel for the current liability. From there, you can do some general projections to see where that figure could end up.

As you get closer to the year they mature, assess your other income sources to get an idea of your taxable income. With such great fixed rates, you will want to keep the bonds for as long as possible. However, depending on your other income sources you may have to redeem some early to manage your specific tax situation. If you are/will be on Medicare, you need to be aware of the IRMAA income levels. You could also be pushed into higher marginal tax rates.

For those who live in states with income taxes, revel in the fact that your state will not touch one single penny of the interest!

I once learned from an accountant that you can change to declaring the interest on a yearly basis. BUT, you have to do it for ALL your bonds (ie, you can’t cherry pick) and the year in which you do that, you have to declare all the interest to date and then, going forward, it would be on an annual basis. If you have a lot of I-bonds, it’s likely not going to be a viable option.

David, thanks for the comments. I was a little late to the party, so I only have a blended fixed rate of 2.2% on the I-Bonds in question. Using an average inflation factor of 2.8% for an annual 5% compounded growth rate the accumulated taxable interest is still significant. Looking at individual years, obviously some are much higher than others, but none are acceptable (for tax purposes). We don’t have state taxes to worry about, but the Medicare issue just makes matters worse, ouch. My wife and I are both on Medicare, in excellent health and there is an 11-year difference in our ages. In my annual letter I have scheduled that, in the event of my death, my spouse could redeem two or three bonds per year, starting now, and along with her other income, she would be fine financially, and the tax hit would not be that bad. Unfortunately, I haven’t died, yet!! I think early redemption is the only answer. Of my six bonds maturing each year, I think I will hold two or maybe three bonds (especially the bonds with the highest fixed rates) until the year of maturity. Then, I have a couple of skipped years where I can redeem two or three bonds just one year early (actually, depending on the original month of purchase I would loose something less than a years worth of interest). I can then roll the dollars over to new I-Bonds (or the best available investment at the time) and buy another 30 years to maturity. With the current fixed rate, the hit isn’t that bad. So, I think I will model the redemption of two specific bonds now, rolling them over to new I-Bonds (1.3% fixed) and, along with our current income, what is the tax impact. Then (the hard part) compare that to what would happen if the same two bonds were held to maturity along with our projected income at that time. There are a few wild cards that I can think of such as future tax rates, our deductible health expenses, and so on, but I can’t control those. David, again, thanks for your input, I guess we should be happy that we are in a position to have to pay the tax man.Paul M.

If you want to make the election to pay the tax on I bonds annually, then you must report the interest on your tax return on every I bond you have ever owned. Then report a years interest at a time going forward.

Congratulations on the “over 1m views”! Here’s to a great 2024 for all of us.

Eagerly awaiting the I-Bond buying guide!!!

Thanks for your work here. This is where I came in 2022 to learn about alternative inflation-hedged options after I bought my limit of I-Bonds (I’m rolling those 0.0% I-Bonds into 1.3% bonds this year). My first TIPS purchase was the comparatively poor 5/8% 10-year of July 2022, but I’m happy with the portfolio I’ve built overall (including some of the 5-year auctions of October and December last year).

I’ll probably be buying more TIPS this year, even though the coupons will likely be lower. If the Fed really does start cutting, the inflation will hang around a while…

I also own that July 2032 TIPS. I bought at that auction and then again in September 2022 when the real yield was 1.248%.

We found this site thanks to ZeroHedge

Congratulations, David, and happy new year! I’ve been an avid follower of your blog since early 2022 and greatly appreciate your detailed analyses on TIPS, I Bonds and other fixed income investments. I probably never would have added TIPS to my portfolio without your guidance. Here’s hoping 2024 sees continued progress on inflation and more decent opportunities for long-term inflation protection.

Mr. Enna:

Congratultions on a great year. With knowledge that you and Mr. Bodie have provided, we have been investing in TIPS and I Bonds since 2015. They now constitute a significant part of our assets and provide great peace of mind. Like you, we took advantage of the exceptional windows of opportunity that occured in 2023.

Best in the New Year.

GVE

I feel that I am relatively new to reading and participating on this blog. I have learnt so much and not just only about TIPS but also about how to analyze inflation in general, IRA to Roth IRA conversions, about selecting the right Medicare options, and from discussions and strategies related to managing cash flow/income during retirement. I Bonds was primarily thing I understood well, before getting lucky to find this blog. Thanks a million (certainly a celebratory and well deserved number for David) for all your help. Wishing you all a Happy, Healthy, and Prosperous 2024.

Congratulations, David, and Happy New Year!

Under Final Thoughts you wrote, “I am happy about the financial events of 2024…”

I hope you can write that again next December!

😊

Thank you Editor Karlos! I have fixed my error.

Hi. My spouse and I will be selling our 0% ibonds ($10,000 each) in early January. I’m leaning toward buying $10,000 of the current offering. Can I sell and buy on TreasuryDirect without having to send the money to my bank and then back to TreasuryDirect? I guess the interest on the initial $10,000 would need to be sent to my bank at least. Thanks!

My plan (subject to learning more from this site) is to cash in my 0% bonds on Jan 2 (sacrificing 3 months of 3.38% interest) but to wait until end of April to buy new ones, in order to get 5+% interest on the cash in the interim.

I like this plan. The 0.0% I Bonds will be earning less, 3.94%. I doubt short-term rates will fall that far by April.

Dave & David, I plan on doing this too, though it will take some transferring because TD doesn’t make it easy to add another bank.

How long do you think the MMFs will pay 5%? I don’t understand how their rates are set. I suppose finding a CD that matures in April might yield a little more.

The best money market funds will generally have a yield less than the 4-week (currently 5.60%) and 13-week (5.40%) T-bill. When the Fed begins cutting interest rates in 2024, those numbers are going to start declining. But we don’t know when the Fed will do that.

Vanguard’s main money market funds are currently paying 5.32%. Money market fund interest rates are based on rates on short-term Treasuries and other securities that the money market funds buy. I’m no expert but I believe they are greatly influenced by changes in the fed funds rate. A 3-month CD at a good rate could be a good option, or buying 13-week Treasury bills (currently paying 5.25%) which are being auctioned on 1/2 and 1/8.

I just added another bank in a few minutes, as I am hoping to use my Fidelity account for most future transactions. (Tired of getting “0” interest from my regular bank account between investments.). I believe the tab I used is under the account management section,

Thanks, Ann. I’ll look into it. Maybe it’s easier now. Fidel also what I want to add

I clicked on Bank Information and it locked my account! I called to unlock the account and the robot said wait times were over an hour. 😐

Karlos- wow, that’s not right! Hope it’s not too much of a hassle to get it fixed. Last time I talked to a rep, I couldn’t remember the answer to my security question. She gave me some hints.

I couldn’t get through on the phone yesterday, but got through after waiting about 15 minutes on the phone today and got the account unlocked. I was able to add another bank account and redeem the iBonds. Phew!

You could use your TreasuryDirect 0% Certificate of Indebtedness as the destination for the I-Bonds you are redeeming, then use the same to pay for the new ones when the funds are there. It takes a couple of business days to process. When you start the redemption process, TD will tell you when the money is expected to be available before you hit the button to submit. I actually set up a redemption of a 0% fixed I-Bond on 12/28, with completion expected on 1/2.

And, yes, the proceeds TD says I am to expect on January 2 from my December submission do include the full interest for December.

When you did this, does TD consider the 0% I-bond to be redeemed in December or in January? (If the former, you’ve foregone one month of interest that you could have had by waiting until January to redeem, no?)

WordPress is messing with me a bit, not sure what I did to anger the site gods LOL. I seem to have resurrected a really old defunct account that is causing me headaches. Anyway –

The amount reflected in the transaction does show the correct total for a January redemption. No interest was given up. Again, TD does show you the transaction details before you hit the submit button to finalize.

thanks, that’s good to know!

You don’t have to redeem the entire amount if you don’t want to. For example, if you have a Series I (IAAAA) with 0% fixed interest worth $11,210, you can redeem $10,000 into zero-percent CoI and buy $10,000 (IAAAB) at current fixed-interest rate, and still have $1,210 of IAAAA left to hold and redeem at a later time.

True. But you will owe income tax on whatever portion you do redeem. In your example I’d guess it would be your tax rate on about $1,079 since you are redeeming about 89% of the total. It isn’t a huge amount, but not to be ignored either because the IRS doesn’t like it when such things are ignored.

You can’t do this, If you sell your 0% I bonds, your going to get the 10,000 + in your bank account, then you buy the new ones. When you buy t-bills and do automatic reinvestment, in that case when the T-bill matures, you only get the interest. Sending you the proceeds and then taking it back for the new T-bill is not what they do.

Whatever one I Bond (or portion of an I Bond) you redeem is sent to one destination that you designate, whether it is to your 0% Certificate of Indebtedness of your TD account or to a bank account you have attached to your TD account. As I think Chris is saying, the interest and principle are not separated from the single lump payment. How you do or don’t divide it after that is entirely up to you.

Hello David,

Thank you so much for writing your interesting and informative newsletter, and congratulations on your success in 2023! Wishing you and your family a very happy Year of the Dragon 🐉 🐲 with many enjoyable travels!

Cheers,

Sabine Nooteboom

Congratulations on the great success of your independent website! I’ve learned a lot through your writings and made some investing decisions that I probably wouldn’t have without the insights provided here. Overall, just a great opportunity in the 2023 fixed income marketplace to get substantial positive real return with little risk to principal.

Treasury Bill and CD rates are falling markedly. How does this atmosphere play into past columns and comments about redeeming I Bonds with 0% fixed rates?

T-bill rates are actually holding up nicely (so far) and so are many bank CDs. The 13-week T-bill is down only 3 basis points this month. My general advice on redeeming I Bonds is: “Redeem when you need the money.” But I can definitely see the logic in redeeming 0.0% I Bonds to purchase 1.3% fixed-rate I Bonds in 2024.

I redeemed my August 2021 and February 2022 0% fixed rate I-Bonds on November 2nd and bought 5.4% 16-month no-penalty FDIC-insured CD’s on Raisin.com. They still have a 12-month 5.41% no-penalty CD available as of this morning. Both new customers and the current customer receive a referral fee, but I won’t include mine without permission.

This is the way to go if you believe you will need this money in the short term. If not, then getting 1.3% above inflation for many years, tax deferred and free of state taxes, also makes sense.

Good points David. I’ve been debating whether or not to use some of my RMD next month for I-Bonds, but if I do, I think it needs to be a 5+ year decision. It appears that we’re heading for some under 3% 6-month inflation rates, with the past two months being negative, and I’m trying to (1) guess how a likely future composite I-Bond rate that’s under 4% will compare with other options; and (2) decide whether I would rather go with a short-term option without a 3-month penalty for more short-term liquidity. Could you lend me your crystal ball? Thanks.

Hi David, Happy 2024 🎉 Thanks for all the amazing and detailed education you consistently provide. It’s so appreciated! Wishing you a healthy and prosperous year with lots of travel.

Cheryl

Hi David, I always look forward to your email messages. The $116,000 in I-Bonds that I purchased between late December 1998 and late October 2001 will be worth $473,680 as of January 1st. I’ve told my wife many times that I would cry if we ever had to redeem them early (I’ve been smiling for the past 25 years!).

Wow, those were great investments with fixed rates of 3.4% and 3.0%. As the maturity date approaches (now only 4+ years away for some) you’ll want to devise an exit strategy. You could be facing a big tax hit, plus higher Medicare payments for a year or two. Are you thinking about gradually reducing your holdings as 2028 approaches?

I’m thinking we’ll be able to stay within the standard Medicare premium range, but I’ll keep an eye on it. We will owe a chunk of taxes! A bit under $120k in I-Bond interest in 2028 + about $45k in taxable Social Security benefits + about $35k RMD would be just below the current $206,000 Medicare premium threshold. I expect this threshold to creep up to around $225,000 by 2028. I was lucky in April 2000 when I only had $14,000 available to buy the 3.4% fixed rate I-Bonds, so I was able to scrape together additional money to buy $12,000 in 3.6% I-Bonds in May 2000. Actually, they were letting us use credit cards at that time, so I was also earning 5% rewards on my GM MasterCard and taking advantage of the extra month paying off the charge card in full each time.

That credit card deal was sweet. I bought a lot of bonds during the early 2000’s. I’m working on converting IRAs to Roth’s so I won’t have to deal with as big a tax hit when the bonds mature.

Yes, me too. I’ll be making Roth Conversions in 2024-2027, none in 2028-2031.