By David Enna, Tipswatch.com

I am traveling today so this will be a brief post.

So … it looks like the Federal Reserve’s wariness on inflation has been justified, at least based on data from the January inflation report.

The Consumer Price Index for All Urban Consumers increased 0.3% in January on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 3.1%.

Both the monthly and annual numbers came in higher than expectations, and I had even heard discussions on CNBC of a possible “2-handle” for annual inflation coming out of this report. It didn’t happen. Core inflation also was higher than expectations, coming in a 0.4% for the month and 3.9% for the year.

Once again, the BLS pointed to shelter as a major driver of overall inflation, with shelter costs rising 0.6% in January and 6.0% for the year. Food-at-home prices also perked up at 0.4% for the month, after running at 0.2% for two consecutive months. Gasoline prices were down 3.3% in the month and 6.4% for the year.

The annual trend in U.S. inflation shows that core inflation seems to have stabilized at an annual rate right around 4.0%:

What this means for TIPS and I Bonds

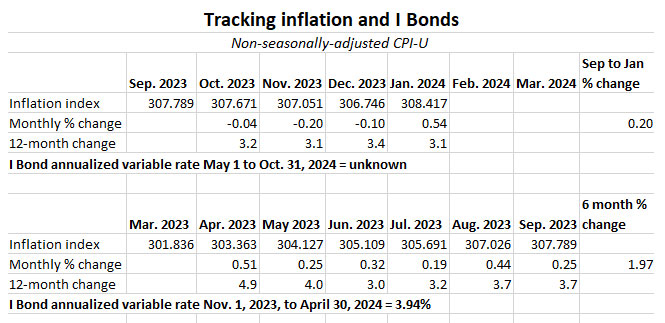

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances for TIPS and set future interest rates for I Bonds. For January, the BLS set the inflation index at 308.417, an increase of 0.54% over the December number.

For TIPS. The January report means that principal balances for all TIPS will rise 0.54% in March, after falling 0.20% in January and 0.10% in February. The Treasury hasn’t posted the new March inflation indexes for all TIPS as of yet. When it does, this link should work.

For I Bonds. The January inflation report is the fourth of a six-month string that will determine the I Bond’s new inflation-adjusted variable rate, to be reset on May 1 and eventually roll into effect for all I Bonds. In the October to January period, inflation has increased just 0.20%, which would translate — for now — to a variable rate of 0.40%, much lower than the current 3.94%. The next two months are likely to increase that number; I’d say 2.0% certainly looks possible.

Here are the data so far:

This is all the time I have this morning. I am off!

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I think I’m going to pull the trigger and buy my $20,000 in I Bonds at the end of the month. It starts the one and five year clocks earlier and the eight week Treasury rate, at 5.40%, is not much higher than the 5.27% I Bond rate. I don’t see the real rate increasing after April either, and even if it did I still have the tax refund which I could try to buy $5,000 in.

I ended up buying our 2024 allocation at the end of January, paid for by a set of 0.0% I Bonds I sold three days later. But I am still looking at a gift box purchase coming up later, probably end of April.

I’ve been taking a hard look at the 30 year TIPS auction next week. With real rates around 2% I think they are a more attractive 30 yr bond vs the iBonds 1.3 fixed rate.

4 week TBills, I like it, I love it, I want more of it!

Yes………….thats a good WATCH and WAIT state-taxfree strategy for now! I share the LOVE!

That’s what I’ve been doing since February last year. I had already bought I-Bonds the previous years with the high variable rates, but zero fixed rates. I wasn’t too impressed with the 0.4% nor 0.9% fixed rate. When the 1.3% came around, I switched out a set I-Bonds with 0% fixed. Otherwise 5%+ T-Bills makes more sense/cents. I’ll probably switch out another set of 0% I-Bonds, but TBD where we stand (ie will the fixed rate have a chance of going up more; probably not, but nobody knows).

+0.5% each of the next two months would result in 1.2% x 2 = a 2.4% I-Bond inflation factor.

+0.2% each of the next two months would result in 0.6% x 2 = a 1.2% I-Bond inflation factor.

Add the 1.3% fixed rate for I-Bonds purchased by the end of April or an unknown fixed rate that will be announced on May 1st.

For someone in their 70’s looking for a short-term investment, these do not look very attractive.

However, as a person in their 70’s looking to reduce taxes by moving cash to ibonds (from a taxable account) before RMDs at 73, the current rates look pretty good to me.

Have a great trip