Annual core inflation hits 6.6%, a 40-year high. This isn’t good news for financial markets.

By David Enna, Tipswatch.com

Here is it, the most important Inflation Day of the year, setting in stone the inflation-adjusted variable rate on U.S. Series I Savings Bonds, plus determining the Social Security cost-of-living adjustment for payments beginning in 2023.

So, what happened? All-items inflation rose 0.4% in September on a seasonally adjusted basis, and is now running at 8.2% year over year, the Bureau of Labor Statistics reported. Both of those numbers where higher than consensus estimates, meaning this inflation report could roil the stock and bond markets. Core inflation was 0.6% for the month and 6.6% year over year, also higher than estimates. At 6.6%, core inflation is now at a 40-year high.

I’ll get back to the inflation report, but let’s first dig in to the big news of the day.

New I Bond variable rate

Investors in Treasury Inflation Protected Securities and I Savings Bonds are interested in non-seasonally adjusted inflation, which is used to adjust principal balances for TIPS and set future interest rates for I Bonds. For September, the BLS set the inflation index at 296.808, an increase of 0.22% over the August number.

For TIPS, this means that principal balances will be increasing 0.22% in November, after falling 0.04% in October. For the year ending Nov. 30, TIPS balances will have increased 8.2%. Here are the new November Inflation Indexes for all TIPS.

For I Bonds, the September report was the last of a six-month series that will set the I Bond’s new annualized variable rate, which will go into effect for I Bonds purchased from November 2022 to April 2023. Inflation increased 3.24% over that period, so the I Bond’s new variable rate will be 6.48%, annualized. Here are the numbers:

All I Bonds, no matter when they were issued, will get the 6.48% variable rate for a full six months. The starting month will depend on the month the I Bonds were originally purchased. Investors can still purchase I Bonds in October and receive a full six months of the current rate, 9.62%, and then six months of 6.48%. That creates an annual return of 8%+ for a very safe investment.

The one question lingering out there is “Will the Treasury raise the I Bond’s fixed rate at the November 1 reset?” I think the Treasury should raise the fixed rate, but it’s a tossup on whether that will happen. Most I Bond experts think the rate will stay at 0.0%.

My recommendation is to load up on I Bonds in October. If the fixed rate rises in November, you’ll be able to purchase a new allocation of I Bonds in January, up to $10,000 per person per year, and benefit from the higher fixed rate.

A recent Wall Street Journal headline suggested that I Bond interest rates were about to “come down to Earth,” but no, 6.48% is an extremely attractive interest rate in October 2022. I Bond investors should continue holding this investment through the six months of 6.48%, annualized. The rate is the third highest in the 24-year history of the I Bond.

• Confused by I Bonds? Read my Q&A on I Bonds

Social Security COLA

The September inflation report was the third of three — for July to September — that will set the Social Security Administration’s cost of living adjustment for 2023. The SSA uses a three-month average of a different index, the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), to set its COLA.

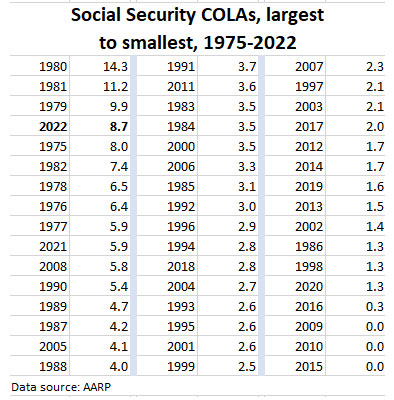

For September, the BLS set CPI-W at 291.854, which produced a three-month average of 291.901, an increase of 8.7% over the same average for 2021. That means the Social Security COLA will be 8.7% for payments beginning in January. That increase actually outstrips overall U.S. inflation, which has increased 8.2% over the last year. Here are the numbers:

This will be the fourth-largest increase in the history of the Social Security COLA, which was first launched in 1975, and a large bump higher than last year’s 5.4% increase. And for the second year in a row, the Social Security COLA was higher than official U.S. inflation, 8.7% vs. 8.2% for the September to September period. Here’s a look back at the COLA’s history:

The Social Security Administration says the average monthly benefit for U.S. retirees is $1,666, so an 8.7% increase will raise that monthly benefit to $1,811, or about $145 a month. If you are in the Social Security “limbo” period — older than 62 but not yet taking benefits — your future benefits will also climb by this percentage.

In addition, Medicare costs will be falling in 2023 for most retirees, with a typical person paying about $63 a year less for Part B coverage.

September inflation report

Once again, we get a starkly negative U.S. inflation report, with both all-items and core inflation coming in above consensus estimates. And this happened even though gasoline prices fell 4.9% in September, a trend that seems to have reversed in October.

Today, at 7:55 a.m., the S&P 500 futures were up 36 points. Now, one hour after the inflation report was issued, the S&P index is down 68 points, about 2%. The real yield of a 5-year TIPS on the secondary market has soared to 1.95%, up about 15 basis points this morning.

The BLS noted that “increases in the shelter, food, and medical care indexes were the largest of many contributors” to the higher all-items inflation. Again, this is evidence of inflation spreading throughout the U.S. economy, even as the economy seems to be slowing. Key findings from the report:

- The food index continued to rise, increasing 0.8% over the month as the food at home index rose 0.7%. Food at home prices have increased an astonishing 11.2% over the last year.

- The index for fruits and vegetables rose 1.6% in the month.

- Gasoline prices fell 4.9% over the month following a 10.6% decrease in August, but remain 18.2% higher than a year ago.

- Shelter costs increased 0.7% for the month and are up 6.6% over the last year. The rent index rose 0.8% in September.

- The medical care index jumped 1% in September and is up 6.5% for the year.

- Costs of used cars and trucks fell 1.1% in the month, but remain 7.2% higher over the year.

- Apparel costs also fell, down 0.3%.

The BLS noted that core inflation — which removes food and energy — rose 6.6% over the past 12 months, the largest 12-month increase in that index since August 1982.

What this means for interest rates

Federal Reserve officials have been taking very public hawkish positions on future interest rates, and this inflation report backs up their words. Until inflation — especially core inflation — begins to fall toward the 4% range at a minimum, the Fed will have to stick to the plan: Raise short-term interest rates to about 4.5% and keep them there. But so far, core inflation continues moving in the wrong direction, as shown in this BLS chart:

From this morning’s Wall Street Journal report:

“Inflation has built up a lot of momentum over the last year,” said Bill Adams, chief economist at Comerica Bank. “That’s going to keep inflation higher than the Federal Reserve wants it for at least a couple more months—if not a couple more quarters.”

In addition, here are some thoughts from inflation guru Michael Ashton:

“We keep waiting for a clear turn in inflation, and it hasn’t happened yet. … That being said, and while 75bps is pretty much cemented now at the next Fed meeting, I still think that the FOMC is looking for reasons to slow the pace of hikes. Things are starting to break around the world, and there’s no appetite (I don’t think) to test the limits of the system’s fragility right now. But the balance sheet is going to continue to shrink slowly, and that’s a big part of the decline in market liquidity.”

Today’s turmoil in the stock and bond markets is another reality check: The Fed isn’t likely to back down from tightening. Higher interest rates are coming, in the near term at least. The Fed has to maintain its credibility.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. The investments he discusses can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

this is probably the incorrect place to post, but, I missed yesterday as being the last day to purchase I Bonds–because their site crashed? That does not see quite fair–!!!! I thought AT THE LEAST, I could purchase this weekend. And if we purchase on Monday the 31 of OCTOBER, we get bumped into the new rate?

If you failed to complete the purchase by Friday midnight EDT, your purchase will get the new November variable rate (6.48%) plus whatever fixed rate the Treasury sets on Tuesday. Here is more on this topic: https://tipswatch.com/2022/10/28/treasurydirect-this-is-not-acceptable/

If there is a I bond purchase limit of 10k a year, how can a person “load up on I bonds” this October ?

People are using the “gift box” strategy to pre-load I Bonds for granting in future years. Here is an explanation: https://tipswatch.com/2022/10/23/want-to-stash-i-bonds-in-a-gift-box-do-it-by-wednesday/

Pingback: Ignore the fixed-rate drama; buy I Bonds in October | Treasury Inflation-Protected Securities

I just got my AARP Bulletin in the mail. In the “Social Security Checks To Jump” article, some guy called David Enna predicted that “If nothing else happened, the increase would be 9%.” Well, 8.7% wasn’t that far off, now was it? And, who would have thought that the funky way of calculating the COLA would work in our favor (again)?

Then there’s the totally bizarre market reaction to today’s inflationreport. That 1.90% yield on the 5 year TIPS didn’t last long. At the end of the session it back down to where it started the day. And stock? They went up over 2%. That’s right, the CPI-U goes up higher than predicted, and the markets just shrug it off. Actually, ignored it is more accurate.

The good news is what this portends for next week’s 5 year TIPS new issue auction. If the CPI-U had gone down significantly it would have given the FED some cover to ease up a little bit. So, now there’s no excuse for people talking-up a FED “pivot”. Of course, that won’t stop them from trying. After all, annualized inflation went down from 8.3.% to 8.2%!

I did that interview with AARP more than two months ago, so a lot “happened” but I was pretty close anyway, since the reporter specifically asked, “what if inflation doesn’t go up at all?” … Yeah, the stock market yesterday was totally baffling. I can’t figure that out at all. But the stock market soaring actually helps keep the Fed on course.

i saw you mentioned the Cleveland Fed’s Nowcaster CPI estimates in a recent tweet. ended up being highly accurate for the yoy measurements for this month, at least. any other CPI/PCE inflation estimators that you’ve found useful, or do you take them all with a grain of salt?

That Nowcasting site is “at least something,” I’m glad they do it. They’ve generally been on the high side for monthly inflation, but this month were on the low side. Just shows you how hard it is to predict inflation even a half month out. (The October prediction is a scary 0.8%) Here is the site for readers who are interested: https://www.clevelandfed.org/our-research/indicators-and-data/inflation-nowcasting.aspx

David, why is the fixed rate expected to remain at zero? If you look at the average TIPS real yield across maturities (which is currently positive 1.71%) on the day prior to the reset date, you get these stats:

Avg TIPS Real Yield Avg I-Bond Fixed Rate Observations

0.20% – 0.40% 0.10% 3

0.40% – 0.60% 0.07% 6

0.60% – 0.80% 0.20% 3

0.80% – 1.00% 0.30% 1

1.00% – 1.20% 0.50% 1

1.20% – 1.40% 0.17% 3

1.40% – 1.60% 1.10% 3

1.60% – 1.80% 0.55% 2

1.80% – 2.00% 1.10% 3

Yes, I agree, and I wrote an opinion piece on why the Treasury SHOULD raise the fixed rate: https://tipswatch.com/2022/10/02/opinion-treasury-should-raise-the-i-bonds-fixed-rate/ … But the common opinion among I Bond experts is that the Treasury can stand pat because demand for I Bonds will remain very strong well into 2023. We’ll see on Nov. 1.

I always thought that the Treasury offered I-bonds as a way for the little guy to save for retirement, not as a way to fund the gov’t. Isn’t that why they limit the purchase amount to $10k. It’s basically the only way for savers to earn a non-negative actual (not market implied) real yield.

Thanks for calculating the variable rate. I used to do it, but then I found your excellent website so I don’t have to anymore. Those 3% fixed rate I-bonds I bought in the early 2000s are looking pretty good now. They will be yielding about 10% for an entire year. However, I am not looking forward to the tax hit in the early 2030s. I may sell some a little before maturity depending on interest rates and tax bracket.

I calculate a 6.47% annualized I-Bond rate unless they round up.

[ (296.808/287.504) – 1) = 3.2361% x 2 = 6.4723%]

Yes, the inflation rate is rounded to the nearest hundreth, then doubled. That means the variable rate will always have an even number in the hundreth decimal spot. From the Federal Register:

§ 359.11 What is the semiannual inflation rate? …. “The rate of change over the six-month period, if any, will be expressed as a percentage, rounded to the nearest one-hundredth of one percent.”

FYI, the Wall Street Journal posted a story today with your same error, and that is an error I also have made in the past. I tend to remember my errors!

Yes, that works. Thanks for the clarification.

FYI

Recent WSJ article excerpt:

Bipartisan legislation introduced in the Senate last month would raise the cap on purchases from the current $10,000 to $30,000 when CPI holds above 3.5% year-over-year for a period of six months or more.

All that means is at least one member of both parties signed on to the legislation and sent it to the appropriate committee for consideration. It doesn’t mean the legislation will necessarily make it to the floor for a vote (many bills die in committee) let alone get the 60+ votes it needs to get passed any filibuster, then get passed in the house (and survive any reconciliation between the two chambers) and be signed into law by the president.

For now its “just a bill on capitol hill” (as the old schoolhouse rock PSA song went).

I have a couple I bond questions maybe you know the answer too. I tried to use the treasury direct site but most of the answers seemed to be on “page not found”. The first question is: I have purchased my 10k limit of I bonds and I also purchased 10k as a gift for my wife. She has done the same for me. Can I now purchase another 10k as an additional gift for her? I understand I can not give her the gift if she has already reached a yearly limit. Wondering if I can accumulate in the “gift box” if my time horizon is longer. The second question is whether the 10k a year maximum is based on when you physically purchased the last I bond. I purchased in April. or is it possibly just based on the calendar year? So could I purchase next years allotment in January 23? Thanks

I am not an expert on the “gift box,” but I can tell you that TreasuryDirect is currently spinning off an error message for people who try to use the gift box after reaching their personal $10,000 cap. It probably is a glitch caused by site changes. Under the existing rules, as we know them, you could purchase more in the gift box but you will be limited to $10,000 in distributions each year to each person.

The $10,000 limit is for the calendar year, so you will both be able to buy more I Bonds in January.

Thank You

David do you plan an analysis of the 5 year Tips, 91282CFR7 scheduled to be auctioned on 10/20/22? I am traveling next week and it looks good to me at this point. Do you think the coupon interest rate will be set greater that 0.125%?

Thank you for all the good information.

Yes, I will be posting a preview of that auction on Sunday morning, if all goes well. This one is going to be unusual and highly attractive, in my opinion. It should end up with a strongly positive coupon rate, at least 1.5%, maybe even 1.625%, or higher. Plus, it will have an inflation index of 0.99982 on the settlement date of Oct. 31, meaning that it should end up with an adjusted price that is below par. You have to go back to April 2010 to find a new-issue 5-year with an auction price below par.

Thank you for your expertise

I have been educating myself on TIPS – and am thinking of buying the upcoming 5 year and holding to maturity. So your post will be very much appreciated. the 5 year breakeven rate seems to be 2.38 as of yesterday – so I think over 5 years this is a better bet than nominal 5 year treasury. thanks again.

AR, good work! This is correct, the 5-year breakeven was 2.38% at the market close yesterday. Historically, that’s a bit high, but not by standards of 2022, with inflation running at 8.2%. I recently bought a 5-year nominal Treasury yielding 4.24%, which is also very good. I like 5-year nominals with a yield over 4%.

Can you explain the difference in the .22% (TIPS/I-Bonds) increase versus the .4% CPI report?

I Bonds and TIPS track non-seasonally adjusted inflation, while the official monthly inflation report is seasonally adjusted. These often vary a bit month to month, but balance out over a year.

If tips are also inflation adjusted and they have a real yield as of the last month or so are they not a better deal?

Great question. I Bonds have some strong advantages: ease of ownership, better deflation protection, a flexible maturity, tax-deferred interest, can never go down in value. TIPS are a more complex investment, but getting a 1.9% real yield on a 5-year TIPS certainly makes the TIPS very attractive versus an I Bond.