By David Enna, Tipswatch.com

There were no surprises in today’s Treasury reopening auction of $20 billion in CUSIP 91282CJH5, creating a 4-year, 10-month Treasury Inflation-Protected Security.

The real yield to maturity came in at 1.710%, which exactly matched the when-issued prediction used by bond traders. In the hours before this auction, this TIPS was trading on the secondary market with a real yield of 1.69%, so today’s investors got a 2-basis-point boost.

Definition: A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation each year until maturity.

In its originating auction on Oct. 19, 2023, CUSIP 91282CJH5 got a real yield to maturity of 2.440% and its coupon rate was set at 2.375%, the highest for any 5-year TIPS since the very first TIPS auction of this term in history, which generated a coupon rate of 3.625% on July 9, 1997. Market conditions have changed dramatically in the last two months, as shown by the 1.710% real yield generated by today’s auction.

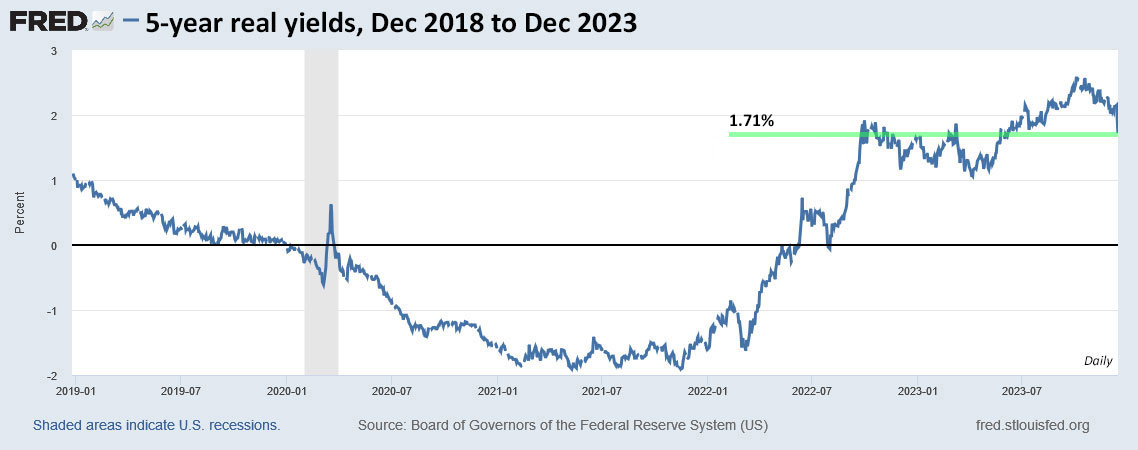

While 1.710% was well below the October auction’s real yield, it remains high by historical standards, as shown in this chart of real yields over the last 5 years:

Pricing

Because the auctioned real yield of 1.710% fell well below the coupon rate of 2.375%, investors had to pay a premium for this TIPS. This is how the Treasury reported the auction results:

The unadjusted price was 103.046880 and the inflation index will be 1.00453 on the settlement date of December 29. Let’s look at the cost of a investment of $10,000 par value for this TIPS at today’s auction:

- Par value: $10,000

- Coupon rate: 2.375%

- Auctioned real yield: 1.710%

- Adjusted principal: $10,000 par x 1.00453 = $10,045.30

- Unadjusted price: 103.046880

- Cost of investment: $10,045.30 x 1.03046880 = $10,351.37

- Plus, accrued interest of about $48.88

In summary, an investor who purchased $10,000 par value paid $10,351.37 for $10,045.30 in principal and will now collect future inflation accruals and a coupon rate of 2.375% on the principal balance until maturity on Oct. 15, 2028.

Inflation breakeven rate

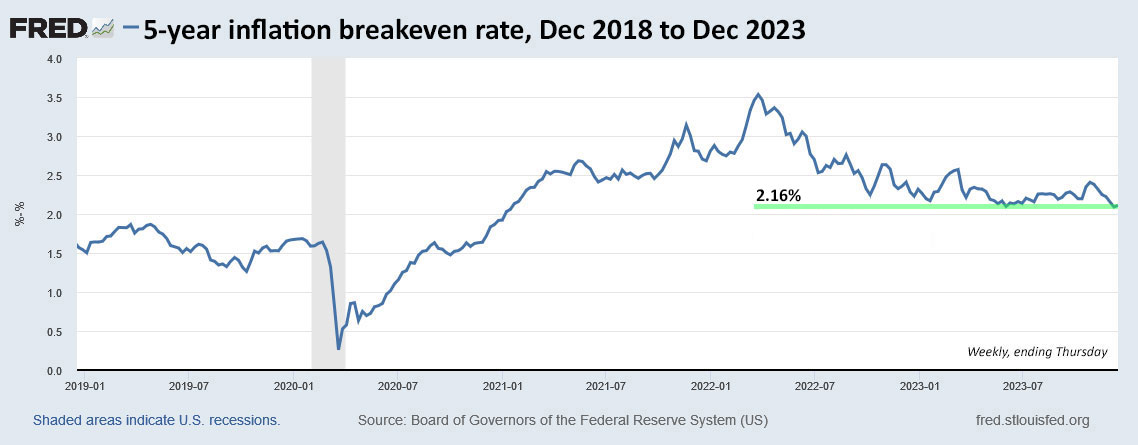

With the 5-year Treasury note trading with a nominal yield of 3.87% at the auction’s close, this TIPS gets an inflation breakeven rate of 2.16%, much lower than results for this maturity in recent auctions. The market is now pricing inflation through the next five years very close to the Federal Reserve target of 2%. Which raises the question: Is the market crazy?

Whatever happens over the next 4 years, 10 months, investors in CUSIP 91282CJH5 at today’s auction got a low-risk, appealing result, especially versus the 5-year nominal Treasury.

Reaction to the auction

It looks like the auction went off almost exactly as expected. The bid-to-cover ratio was 2.55, indicating decent demand. The TIP ETF, which holds the full range of maturities, barely budged after the auction’s close. Everything points to a ho-hum result.

I’ve noted in recent posts that we seem to entering a new era for Treasury yields, with somewhat lower yields likely over the next several months. At the least, yields should stabilize at current levels until the Federal Reserve reveals more exact information on its future moves.

This was the last TIPS auction of 2023. Later this month I will write a recap of the year in inflation protection, including I Bonds. The next TIPS auction will be Jan. 18, 2024, with the release of a new 10-year TIPS.

Here is the history of CUSIP 91282CJH5, which at its originating auction generated a real yield of 2.440%, the highest for this term in 15 years.

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Advertisements

Can someone please comment about the ease and cost of owning TIPS in a taxable account? I’ve heard mixed ideas from “the phantom income that is taxed is similar to reinvested dividends, which is no big deal” to “never invest TIPS in taxable.” I’m considering a sizable ladder in taxable brokerage account.

I recently built a sizable 10 year TIPS ladder in a Vanguard taxable account. I’m expecting to pay taxes on the coupon payment and increase in principal as it’s reported by Vanguard, but I knew that in advance. My main requirement was to have a reliable regular income built from a decent return, and paying taxes along the way was ok for me. Also, it’ll be nice not to have a big tax bill at maturity.

Thank you, Boglehead!

I wrote about this in April 2021: https://tipswatch.com/2021/04/02/frightened-by-a-phantom-tips-are-fine-in-a-taxable-account-until/

All my original TIPS investments were at TreasuryDirect in a taxable account. I have held all of those and have 8 remaining there, most with attractive fixed rates. These investments are coming in handy now that I am retired, because when they mature I have pre-paid the taxes and there is almost no tax consequence. But since I retired and was able to transfer my 401k to a traditional IRA, I now do all my TIPS purchases there because I can easily raise money there by selling other assets.

I think the “phantom tax” issue is over-hyped, because a TIPS in a taxable account is no different from any bond fund in a taxable account, where you are reinvesting dividends. You have to make sure you have cash flow to cover the taxes each year. Because TIPS now have real yields of 1.64%+, the coupon rate is almost certain to cover taxes on the inflation accruals.

I agree with David above, that the phantom tax issue is “over-hyped”. You eventually have to pay taxes on any alternate investment in taxable anyway.

I have not seen this mentioned, but I can think of two hypothetical reasons that TIPS could potentially do better in taxable than in tax-advantaged accounts:

1. The current tax cuts are due to expire at the end of 2025. If they are not renewed, at least part of the tax you pay on TIPS will be at the current rates.

2. Since you pay your tax on TIPS in taxable over time, rather than in a bulk sum at withdrawal from a tax deferred account, it is possible that when you withdraw the funds from your tax-deferred account the lump sum gains could be high enough to push you into a higher tax bracket.

My strategy is to first fill my tax-deferred account with TIPS and then continue buying in my taxable account up to my desired amount.

There is a third reason that TIPS could potentially do better in taxable than in tax-advantaged accounts. The income earned on TIPS in the taxable account is not subject to state income taxes. The income earned on TIPS in tax-advantaged accounts is.

You are exactly right!

Thank you, David! Can you point me to an article on fixed rates. To better understand what conditions and interest rates tend to raise or lower them? If there’s a rhyme and reason. I’m new to TIPs. Thanks

Donna, I probably should not have used the term “fixed rate” when referring to TIPS, because the proper term is “coupon rate.” (I assume you were talking about TIPS and not I Bonds.) You can read my page on the terminology of TIPS to get a better understanding … https://tipswatch.com/tips-in-depth/

I purchased some of this reopening. As you say, it’s still not a bad result, but it does not look good going forward. Real rates are declining. Do you think that trend will continue or could the trend reverse? Gundlach (so called bond king) thinks the 10 year will be 6% by 2025.

In the near term, I could see real yields declining into 2024 as the Federal Reserve settles on its rate-cutting plans. But other factors (quantitative tightening combined with increased Treasury debt loads) could put pressure on longer-term yields. A few months ago, lots of analysts were suggesting a 6% yield on the 10-year nominal “was possible.” Now, not so many. It’s possible, of course. Depending on how inflation goes, a 6% nominal yield would indicate a 10-year real yield of possibly 3% or higher.

Anyone have a clue as to how to treat the premium paid (which is not a de minimis amount) for tax purposes?

you will find out when you get the 2023 Form 1099. You may find they will report a bond premium, which would reduce your taxable interest

I’m no tax expert and I am just as confused as everyone else on when a capital gain or loss may be reported. In my experience, I have had very small gains reported in the past; not at all significant. It gets reported on the 1099 issued by TreasuryDirect. I don’t have any TIPS in a taxable brokerage account, so no experience there.

IRS Publication 550 provides all the details you need to know about Original Issue Discounts starting on page 12 of the 2022 version. Jumping to the punch line, your broker, if you held the instrument through a broker, should give you Form 1099-OID, or a similar statement, if the total OID for the calendar year is $10 or more. Just enter the amounts per the instructions.

In this case you’re paying a premium so there would not be OID for that. There may be OID for inflation adjustments though.

Pub 550 also provides all the details on how a premium paid on a taxable bond is handled. Unless you instruct your broker that you do not want to amortize premium, your broker will report income on the bond amortizing the premium. Your broker may report the amount of premium amortization for a tax year separately from the amount of gross interest income in boxes 11 and 12 of Form 1099-INT or box 10 of Form 1099-OID or may report net interest in boxes 1 and 3 of Form 1099-INT or box 2 of Form 1099-OID. Either way just follow the instructions with the form you get.

As I had already purchased the Oct bond I recently purchased $5000 of the April 15 2028 1.25% bond. The unadjusted price was 97.334276 and the accrued interest was 11.39. According to the WSJ Tips page the accrued principal was 1.025, When I calculate the cost I come up with 97.334276*1.025*50+11.39=4999.771 but I was charged 5004.2. They came up with a principal amount of $4992.81. Why? There was no transaction fee.

(And yes I know I am really cheap watching every penny).

The Wall Street Journal abbreviates the accrued principal, dropping off one decimal point. So it actually probably was slightly higher. The “principal” amount the broker shows is the actual price you paid, before the $11.39 accrued interest. (This is NOT the principal amount, which would have been something like $5,125.)

Ok. So the actual accrued principal was 1.02591. I am surprised the WSJ doesn’t round up. Anyway, thank you so much for your quick response. I thought I was probably doing something wrong.

I participated today for the first time via TreasuryDirect in this TIPS auction. After the auction, my TreasuryDirect account shows my requested par value, but does not tell me what allocation I actually received. From official results notice it looks like all non-competitive bids were accepted. Should I assume my allocation will be the full par amount I requested? Does it always work that way? Thanks

Yes, if you place a non-competitive bid, all your requested par value will be delivered. All non-competitive bids are automatically accepted at the high yield.

Thanks

You can sign up for emails and get notice of all auctions and the results. Here’s the report on this one.

Description: 4-Year 10-Month TIPS

Term: 4-Year 10-Month

Series: AE-2028

Interest Rate: 2-3/8%

High Yield: 1.710%

Price: $103.513682

Allotted at High: 90.05%

Accrued Interest*: $4.88885

Total Tendered: $51,039,734,700

Total Accepted: $20,000,009,700

Issue Date: 12/29/2023

Dated Date: 10/15/2023

Original Issue Date: 10/31/2023

Maturity Date: 10/15/2028

CUSIP: 91282CJH5

*Per $1,000

To sign up for the emails. https://www.treasurydirect.gov/mailing-lists/

To sign up for emails showing auction results for all Treasury issues, go to this page: https://www.treasurydirect.gov/mailing-lists/ The one you want is “Auction Results Press Releases” … I have used this for years.

thanks!!