By David Enna, Tipswatch.com

Here’s a strange fact: Despite the surge higher in 10-year real yields over the last 16 months, no new-issue TIPS of this term has received a coupon rate of 1.50% or higher since July 2009. That’s true even though daily 10-year real yields crossed the 1.50% threshold in September 2022 and hit a peak of 2.52% on Oct. 25, 2023.

It is just the way the January and July auctions have turned out for this 10-year term. In January 2023, real yields dipped to about 1.22% (the auction got a coupon rate of 1.125%) and then in July 2023, down to 1.49% (the auction got a coupon rate of 1.375%).

This trend might be broken Thursday, when the Treasury auctions a new 10-year TIPS, CUSIP 91282CJY8. The real yield to maturity and coupon rate will be determined by the auction results.

Definition: A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation each year until maturity.

Some thoughts about CUSIP 91282CJY8:

- This will be the only TIPS — up to this point — maturing in 2034. A second will be created in the July 2024 auction of another new 10-year TIPS.

- The Treasury set the auction size at $18 billion, the largest in the 26-year history of 10-year TIPS. Will the market comfortably soak up that additional supply? The Treasury seems at least a little concerned, based on a recent Reuters report.

- This TIPS will have an inflation index of 0.99896 on the settlement date of Jan. 31 because of slightly negative non-seasonally adjusted inflation in November. Principal balances will also decline 0.1% in February, based on December inflation. Big money investors will be adjusting their bids based on these facts.

Real yields have been volatile over the last week, but at this point the Treasury’s estimate for a full-term 10-year TIPS is a real yield of 1.69%, down 14 basis points in a week. The most recent 10-year TIPS trading on the secondary market closed Friday at 1.66%.

It’s impossible to say where we are heading into next week. Tensions are building yet again in the Middle East. China isn’t happy with Taiwan’s election. The U.S. Congress may sink toward another government shutdown, while deficits continue surging higher. Plus, markets are closed Monday for the Martin Luther King Jr holiday.

The result is volatility, but we are used to that.

So let’s assume that this TIPS gets an auctioned real yield of 1.69%. That would be the 3rd highest real yield for this term since April 2010, but well below recent reopening auctions of this term: 2.094% in September 2023 and 2.180% in November 2023. The coupon rate would be set at 1.625%.

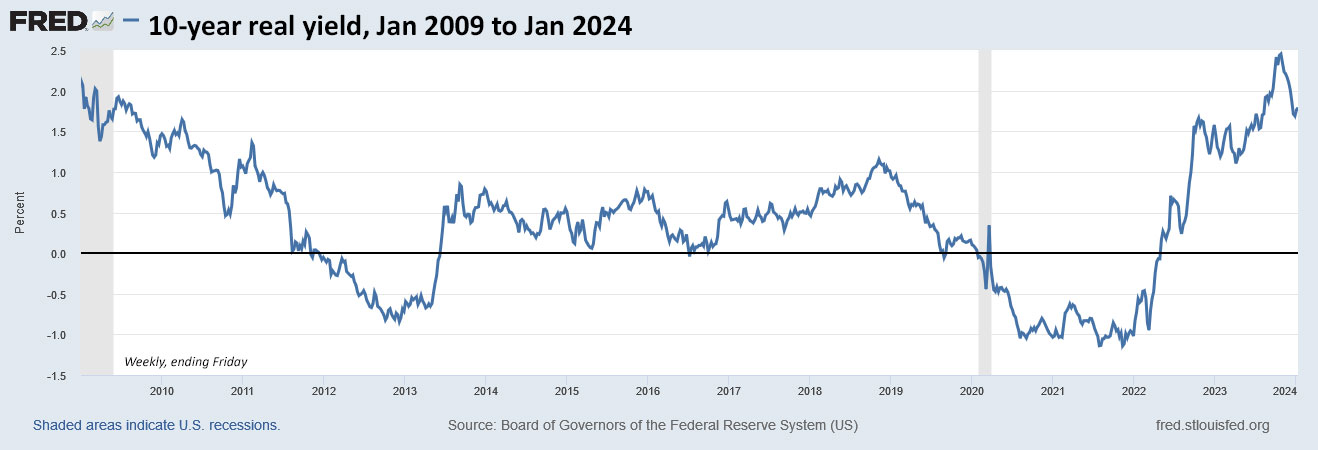

Exciting? Not really. Disappointing? No. It is what it is, a historically attractive real yield for a 10-year TIPS. Here is the trend in the 10-year real yield over the last 15 years:

Pricing

Because this is a new TIPS, the coupon rate will be set to the nearest 1/8th percentage point below the auctioned real yield. That means the TIPS will have an unadjusted price below 100. Add in the fact that the inflation index will be 0.99896 on the settlement date, and you have a near guarantee that this TIPS will auction with an adjusted price below par value of 100. The only unknown factor is a small amount of accrued interest based on the as-yet-undetermined coupon rate.

What does this mean? If you are placing an order for this TIPS at auction, you can be fairly certain your cost will be very close to or below par value. That makes things easy. If you want $10,000 par, the price should be right around $10,000, either at TreasuryDirect or any brokerage that doesn’t charge a commission.

Inflation breakeven rate

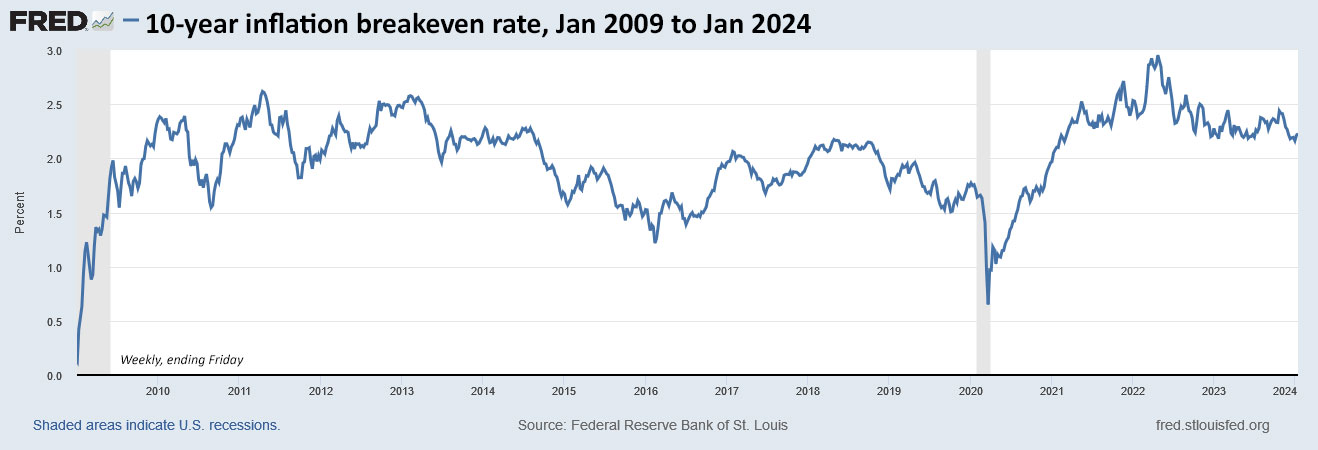

With the Treasury estimating the yield on a 10-year nominal Treasury note at 3.96% on Friday, CUSIP 91282CJY8 currently would have an inflation breakeven rate of 2.27%, which aligns closely with recent auctions of this term. This looks very reasonable to me. Here is the trend in the 10-year inflation breakeven rate over the last 15 years:

From this chart, which shows recessions in shading, you can see that the inflation breakeven rate drops drastically when economic distress strikes. Those are opportune times for investing in TIPS, at least versus a nominal Treasury. As those times worsen, the Treasury generally steps in with quantitative easing, and TIPS investments benefit.

Right now we are in more of a neutral zone. The Fed is still doing quantitative tightening, which means it is lowering its $4.7 trillion balance sheet of Treasurys. But there have been indications QT could end this year. If that happens, TIPS yields could decline along with nominal yields.

Is this TIPS a ‘must buy’?

Although I am planning to buy a sizable investment Thursday, I wouldn’t call this auction a must buy. That will depend on something we can’t know: the future. 1) If you think real yields will be heading steadily lower in 2024, then buy at this auction. 2) If you want to fill a 2034 slot on your TIPS ladder for an investment that will be held to maturity, then buy at this auction. (Or soon after on the secondary market.)

But if you think real yields will be in flux through the year, then you will have plenty of opportunities to buy on the secondary market or at two more reopening auctions for this TIPS (in March and May) and then a new TIPS in July and two more reopenings later in the year.

However, keep in mind that finding CUSIP 91282CJY8 on the secondary market in small lot sizes could be difficult for a few weeks, even more than month.

I Bonds vs. TIPS?

The U.S. Series I Savings Bond currently has a permanent fixed rate of 1.3% for purchases through April. It appears CUSIP 91282CJY8 will have about a 39-basis-point advantage, which I think makes this competition a toss up. I Bonds have a lot of advantages over TIPS, but purchases are limited to $10,000 per person per year unless you use your tax return to get paper I Bonds or add to your holdings through the gift-box strategy or trusts.

As things stand, I definitely plan to buy I Bonds up to the limit this year, very probably in April. After that, I will strategically add to my TIPS holdings. The two investments are compatible — I Bonds for future cash needs and TIPS for defined inflation-protected payouts in future years.

What’s next?

This TIPS auction closes Thursday at 1 p.m. EST. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

You can track the Treasury’s daily yield estimate after the market close each day on its Real Yields Curve page. But remember that the bond market is closed Monday. I hope to post the results soon after the auction closes on Thursday.

Meanwhile, here is a history of the last five years of auctions of this term:

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I tried to buy this on Treasury Direct, but the only thing available on the TIPS purchases page is a 30-year version. When will it be available on TD (or is there another page I need to access)?

You were too late for this one. (Your post shows january 18th 1:25pm posting).

Noncompetitive Closing Time 12:00 Noon ET

Competitive Closing Time 1:00 p.m. ET

Did you order before those time?

Unfortunately, no. I’ll have to keep an eye out if Treasury offers it again.

@rlgreenjr, This same TIPS will be reopened at auction twice: On Thursday, March 21 and then again at sometime in mid-May. Of course, circumstances can change. It also seems to be trading today in the secondary market on Vanguard’s platform, with a real yield of 1.8%, settlement date of Jan 31.

Dave, this does look good. Trying to understand what this will mean over 10 years. So let’s say the real yield tomorrow for the 10-year TIPS auction lands at about 1.80%, and the coupon rate is say 1.70%, and the break even rate is about 2.30%. And let’s also say that the nominal yield tomorrow for a 10-year note is about 4%. Does this mean if one picks up some of the 10-year TIPS tomorrow that if inflation is above 2.3% over the next 10 years that the combined increase in principal and the coupon payments twice a year for a new 10-year TIPS at auction tomorrow will be more than the 4% nominal yield from coupon payments twice a year and principal of a regular 10-year note at the end of 10 years? I’m trying to figure out what the gain can be from a 1.7% coupon payment on an inflation protected principal over 10 years when comparing tomorrow’s TIPS to a T note. Thanks for all the help.

If the real yield is 1.8% an investor in this TIPS will receive a return 1.8% above inflation over the next 10 years. (The coupon rate would be 1.75% and the investor would get the TIPS at a slight discount.) The coupon rate is paid out semi-annually based on the current inflation-accrued principal. So the principal does keep growing with inflation, but the coupon payment is paid out immediately. With a nominal Treasury note or bond, the principal remains the same over time and so does the coupon payment, in your example 4%. With a TIPS, the principal increases with inflation and the coupon payment increases when the underlying principal increases.

The main thing to focus on is the real yield to maturity. Whatever that is, that is amount you will be earning above inflation for the term of the TIPS if you hold to maturity. Read these pages for deeper information:

Thank you

Wednesday evening update: The Treasury’s estimate of the 10-year real yield closed at 1.80% after a two-day surge higher. The most recent 10-year TIPS trading on the secondary market also closed a 1.80%. Looks good for the Thursday auction, but anything can happen …

1.81% – I would say pretty good considering the start of the week.

if buying ANY BONDS in secondary market to capture a higher REAL YIELD vs. what is anticipated in auction, this article explains so clearly about taxation of market discount bonds, OID etc. http://www.projectinvested.com/markets-explained/taxes-and-market-discount-on-tax-exempts/

Wow, it looks like the longer-dated treasury note and bond rates are moving much higher today (back into the 4.0-4.4% range). Dave, will this increase in nominal yields help boost rates for the large 10-year TIPS auction on the 18th? How will the breakeven rate be impacted? Still not sure how to proceed. New to TIPS. Thanks for helping to make sense of this volatility.

Yields moving higher is a good sign for Thursday’s auction, but things can swing the other way in the next two days or even just before the auction’s close.The inflation breakeven rate has moved slightly higher, to 2.3% as of this afternoon.

Will keep watching. Thanks. Is a 2.3% breakeven getting too high? I think the average over the years is about 2.5%?

2.3% is pretty normal for recent auctions.

You were so right, Dave. I see the 10-year par real yield went up to 1.77% today.

Are the 2 interest payments expected for the 1/15 coupon payments or this is the mistake? I’m seeing 2 interest payments of $3.13 and $3.31 in my Fidelity account for the $1000 nominal CUSIP 91282CEZ0 (10yr TIPS maturing in 2032, coupon rate 0.625).

“Bank error in your favor.” They’re making the corrections now. Looks like the higher amount will be correct.

I see what they did. They calculated the interest payment using the par value rather than the inflation-adjusted principal value. So the lower one will get reversed.

David, why do you think that the yield curve remains so inverted, with the short end so high (5.3% on 4-week bills) and the long end so low (3.8% on 5-year notes)? When, or under what circumstances, do you think the yield curve will revert to the mean and become upward sloping again, as it oughta be?

The Federal Reserve controls the short end by setting its federal funds rate, which is currently in the range of 5.25-5.50%. The market sets the longer-term rates and seems to believe 1) that Fed rate cutting will begin soon and/or 2) the U.S. economy is weakening. But the market is ignoring the building U.S. deficit, which will require ever-higher Treasury issues. So sometime in 2024 you could definitely see the short-end rates fall and the longer-term rates rise.

The free market drives this inversion. The Fed is not interested in fairness, if they were, then none of the rates could be less than the rate of inflation.

It is unfair to expect to borrow money for a rate that ensures the money that is returned will have less value than the money that was borrowed, but this is exactly what happened for many years.

OOPS! I inserted quotes and didn’t realize it was going to mess up the entire entry. My apologies.

Edited:

Hi David, Looking forward to April when you guide us toward a decision about buying/not buying I Bonds then!

You wrote: I Bonds have a lot of advantages over TIPS, but purchases are limited to $10,000 per person per year unless you use your tax return to get paper I Bonds or add to your holdings through the gift-box strategy or trusts.

Perhaps as your boilerplate whenever you mention additional ways to purchase I Bonds, you could say this:

I Bonds have a lot of advantages over TIPS, but purchases are limited to $10,000 per person per year unless you use your tax return to get paper I Bonds or add to your holdings through gift-box, trusts, or business-owner strategies.

It would be easy to provide a link to your readers who own businesses and don’t know about the wonderful ability to purchase another $10k/year through a business account with Treasury Direct: https://thefinancebuff.com/buy-i-bonds-business-sole-proprietor-llc.html

Even if you don’t have personal experience with a business account, it would be generous of you to share that option with your readers. It could make the difference of many thousands of dollars to them over the long run!

Thank you!

I am a little confused by this discussion.

David, you state . . . the inflation breakeven rate drops drastically when economic distress strikes. Those are opportune times for investing in TIPS, at least versus a nominal Treasury. As those times worsen, the Treasury generally steps in with quantitative easing, and TIPS investments benefit.

Why would it be good to have a more deflationary CPI? Wouldn’t that cause the fixed rate to decline (for me, a high fixed rate is preferable)? I can see that when inflation picks up, then you are doing better than the nominal you could have bought, at that time, but compared to what you could do (when inflation/rates increase) you are not doing as well.

PS — This is my 3rd attempt to post this (prior posts via WordPress have not gone through; I hope, somehow, the past attempts don’t have a delay and this gets repeated multiple times!).

At these times of high stress, the market tends to way over-price the potential for deflation over a longer term. (Of course, it could happen, but rarely does). For example, in Nov 2008 the 10-year inflation breakeven rate fell to 0.10%. The 10-year nominal Treasury yield was 3.20% and the 10-year TIPS real yield was 3.10%. That was a spectacular time to buy TIPS. Inflation over the next 10 years actually averaged 1.8%, giving the TIPS an annual return of 4.9% versus 3.2% for the Treasury.

So, when the inflation breakeven rate dips to an extreme low, it is unlikely that inflation will actually fall that low over the term of the TIPS. Right now the inflation breakeven rate isn’t low. It is at a more neutral level, even slightly high by historical standards.

David, do you think it makes any difference whether I buy tips in an IRA or an HSA? (I’m 50 so the IRA will be accessible penalty-free when this tips matures. I’m only dabbling because I think keeping money in stocks for another five years or so will give a better return & I prefer iBonds.)

Thanks,

Karlos

Can you buy an individual TIPS in your HSA account? Most of the set-ups I have seen have fairly limited investments. Or would it be a TIPS fund?

My HSA is with Fidelity. I have to put the money in after tax and then claim the deduction the following year when I do my taxes. I have the five-year from last November in there.

It probably doesn’t matter which it’s in.

Correction: I bought the 10-year that was first issued in July in my HSA in November.

Asset location is a hot topic. The asset allocators suggest the trad IRA is the place for your taxable bond allocation since withdrawals will be taxed as ordinary income. Long term capital gains for stocks are best in tax-free or taxable accounts rather than being converted to ordinary income at withdrawal time in a trad IRA.

Now if you’re a liability matcher instead of an asset allocator, then the HSA is a great place to have some inflation protection for those future expenses, especially at real yields north of 1.5%. And you avoid the taxation that some say ruins the inflation protection of TIPS making the HSA an ideal location. Our HSAs are at Fidelity, too, and it’s nice to have the option to buy individual TIPS to hold to maturity.

Thanks, T Lee. The asset location for tax efficiency debate makes my head spin.

Definitely a buyer here. I like to keep it simple and buy at auction even though Vanguard brokerage does an excellent job of accounting for cost basis, etc. I can forsee real yields dropping, but not leaning very much ( I will be a buyer at the July auction as well.)

What do you think of dollar cost averaging into this bond; 1/3 now and 1/3 at each reopening? I would get over 5% on the cash until the reopening and the volatility may work for me in building the ladder (particularly if we get a couple more deflationary CPI readings).

Not a bad idea. It could work for you, or against you. Back in 2022 I started nibbling into TIPS — buying small quantities as yields were rising — and some of those don’t look so great now, but they did benefit from some high inflation. We could be heading into the reverse situation now, but there is no way to know.