Caution: Consider carefully the long term and high volatility.

By David Enna, Tipswatch.com

The U.S. Treasury on Thursday will offer at auction $9 billion in a new 30-year Treasury Inflation-Protected Security. For an investor who can handle the long term and high volatility of a 30-year TIPS, this auction deserves a careful look.

- The Treasury’s real yield estimate for a 30-year TIPS closed Friday at 2.17%, up 26 basis points since February 1. That’s a strong move higher, triggered by elevated inflation fears in the wake of the higher-than-expected January inflation report.

- If the yield holds at 2.17% at Thursday’s auction, it would be the highest auctioned real yield for any 29- to 30-year TIPS since February 2011.

- A yield that high would set its coupon rate at 2.125%, matching the highest coupon rate for any TIPS auction of this term since February 2010.

Definition: A TIPS is an investment that pays a coupon rate well below that of other Treasury investments of the same term. But with a TIPS, the principal balance adjusts each month (usually up, but sometimes down) to match the current U.S. inflation rate. So, the “real yield to maturity” of a TIPS indicates how much an investor will earn above inflation each year until maturity.

So in this case, a real yield to maturity of 2.17% means this TIPS would out-perform U.S. inflation by 2.17% over the next 30 years. That is historically attractive. Getting a coupon rate of over 2.0% is also attractive, in my opinion. It offers a buffer of protection during deflationary periods, plus generates current income that should easily cover the “phantom tax” problem for TIPS in a taxable account.

Here is the trend in the 30-year real yield over the last four years, showing real yields have backed off the highs of late October 2023, but remain historically strong. Obviously, yields could continue rising. Impossible to predict.

There are dangers

There are only two types of investors who should seriously consider buying this TIPS: 1) An investor who is committed to holding to maturity, no matter the ups or downs of market pricing, as part of a structured 30-year plan to set aside inflation-protected cash for the future, and 2) A speculator who believes this TIPS can be sold at a profit in the near- to mid-term future.

A 30-year TIPS is highly volatile. In 2023, the February 30-year TIPS auction generated a real yield of 1.55%, the highest in 12 years. The coupon rate was set at 1.50%, also a 12-year high. It was an attractive result, at that moment. But … with the 30-year real yield currently at 2.17%, that TIPS (CUSIP 912810TP3) is now trading with a price of 85.96, meaning it has lost about 14% of its value in one year.

The investor in that TIPS who intends to hold to maturity will do fine collecting 1.55% above inflation over 30 years. But an investor who can’t stomach that sort of volatility probably isn’t happy. It takes an iron will to invest in a 30-year TIPS and then hold to maturity.

Pricing

This TIPS will carry an inflation index of 0.99952 on the settlement date of February 29. That means any investment at this auction should result in a cost close to the par value. In other words, an investor placing an order for $10,000 in par value should end up paying slightly less than $10,000. But a small amount of accrued interest will raise the cost slightly.

The par value of a TIPS — $10,000 in the example above — is guaranteed to be returned at maturity if severe deflation sets in. For a 30-year TIPS, this really isn’t an issue. But buying a new TIPS at par value is still “nice,” in my opinion.

Inflation breakeven rate

With the nominal 30-year bond closing Friday at 4.45%, this new TIPS currently would get an inflation breakeven rate of about 2.28%, slightly below the rates of the last two auctions of this term. This number seems reasonable. Inflation over the last 30-years, ending in January, has averaged 2.5%.

Here is the trend in the 30-year inflation breakeven rate over the last four years, showing the current rate is close to the typical rate seen since July 2022:

Final thoughts

I won’t be a buyer of this TIPS because its 30-year maturity doesn’t match my probable lifespan for holding to maturity. (My TIPS ladder extends to 2043, when I will be 90. Hope I make it.)

But the auction is intriguing because the real yield is attractive. For an investor who can conceivably hold this TIPS for 30 years, and can tolerate its high volatility, CUSIP 912810TY4 deserves a strong look.

This TIPS auction closes Thursday at 1 p.m. EST. Non-competitive bids at TreasuryDirect must be placed by noon Thursday. If you are putting an order in through a brokerage, make sure to place your order Wednesday or very early Thursday, because brokers cut off auction orders before the noon deadline.

I am writing this from Wellington, New Zealand, where I am 18 hours ahead of Eastern Standard Time. I plan on writing on the auction result after it closes on Thursday, but I can’t say when. The auction closes just at the start of a busy travel day, 7 am on Friday for me. Be patient, but you can check this page for the auction result after 1 p.m EST.

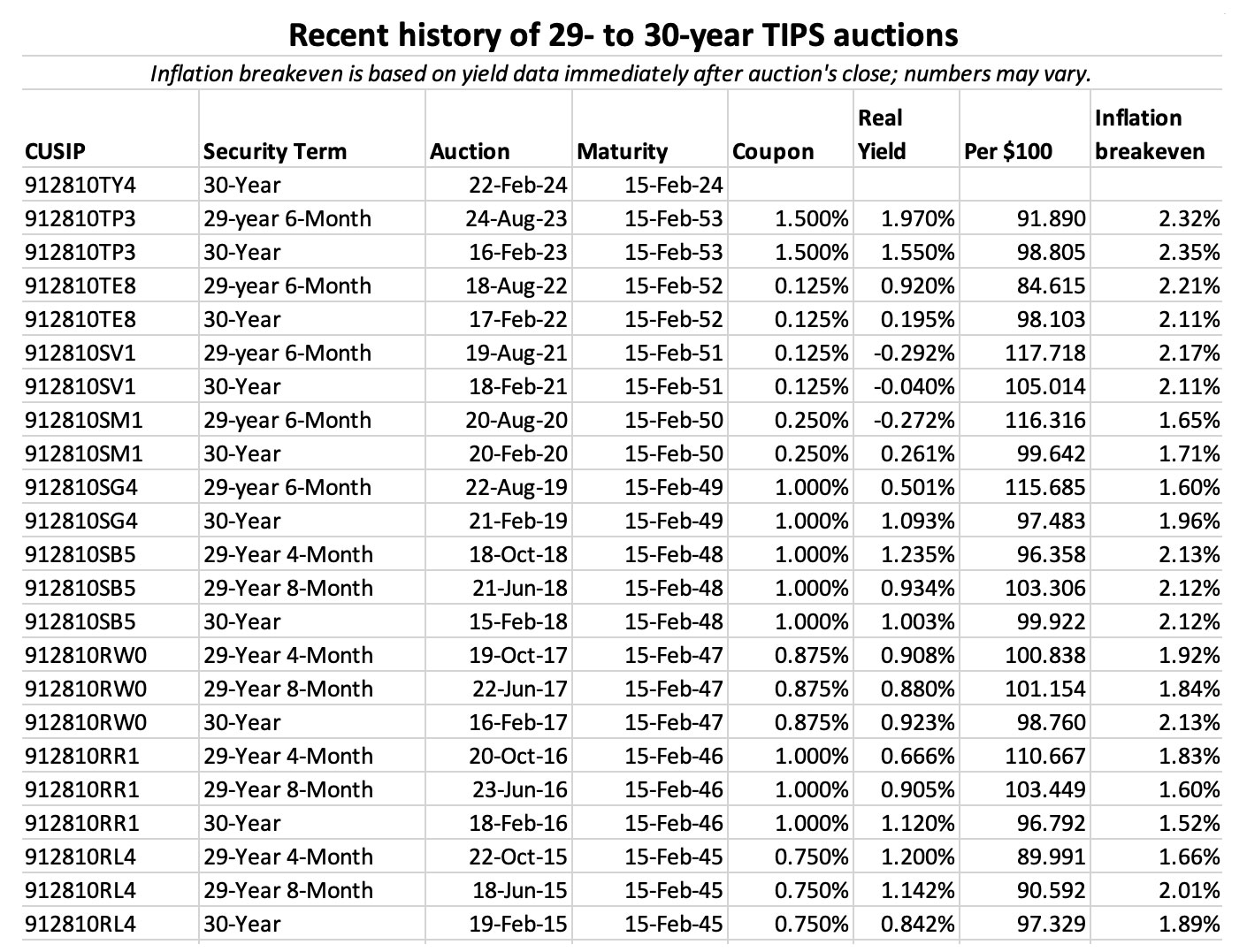

Meanwhile, here are auction results for the 29- to 30-year term over the last eight years:

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear.Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

Pingback: US Treasury – 30 Year TIPS Auction – The Econonaut!

TIPS make sense when inflation expectations are running high as it is presently.

In such an environment, the term-equivalent treasury securities also make sense as the inflation breakeven rate also seems to edge higher alongside real yield / coupon rate of TIPS.

Given the table of historical numbers for TIPS and treasuries, both make sense and at many given points, buying treasuries straight out makes even more sense when breakeven rates are at their historical highs.

Why?

Simply because you can set your attention FREE TO BE and not check monthly CPI numbers etc. The more your ATTENTION is FREE TO BE, the more joy there is to be found in life!

I personally find 5 year or less, whether TIPS or treasury securities as optimal for me for many reasons:

1. Fluctuations in prices easy to stomach

2. Tax situation relatively easier to predict in 5 year out chunks into the future

3. Definitely heirs will not take our hard earned money and spend responsibly as it is not hard earned for them, rather easy money. So i would rather spend adequately to satisfy hunger, shelter, clothing, medicine and basic education existential problems while I am alive rather than expecting my heirs to use inheritance to make a meaningful difference in this world we live in. Existential problems like hunger whether in humans or birds and animals around us is pressing concerns for me than my heirs eating an expensive plate of food in Beverly Hills with inheritance. This also gives me more satisfaction HERE and NOW than heirs can ever give after I am gone!

I agree with your approach, thanks for sharing your thoughts. My threshold is also 5 year for the reasons you articulated. I will just elaborate something that you may have already implied in your comments. Looking for more fun while spending our money, over and above what our children and grandchildren do for fun, NOW and HERE may be worth looking into.

The UPMOST and DEEPEST SATSIFACTIONS that can be had in this world is in selflessness.

The human body-mind complex is simply designed in THAT way by the POWERS that be.

I can travel, eat good food, etc. whatever works for my body-mind NATURE. These are fleeting satisfactions but we have a choice whether to indulge or not. Nothing wrong in moderately pursuing for our selfish enjoyments.

But buy a few bags of unsalted mixed nuts and feed the birds in your backyards – to see their satisfaction is more satisfying and everlasting than eating nuts and getting fleeting sense satisfactions for ourself! This is in my experience. And I also learnt not to chase the squirrels away alleging they are feeding on bird food but instead give them 1 nut at a time so they don’t hoard or bury that comes instinctively for them TO DO but eat to their satisfaction – this satisfaction I see in their face gives me more happiness than overfeeding children and they pushing their plates away and making a face at you………….so how much to spend on these highest satisfaction while sitting in your own backyard? As much as you possibly can afford to – I see if you are generous, it still only runs around 300 bucks a month in costco purchases of peanuts in skin bags, unsalted roasted cashews, unsalted raw walnuts, grapes and the like! 🙂

Whatever remains after I am gone, children can take but by then my children will also have gained a taste to feed whatever comes to the backyard looking for food!

Also, what is more valuable than money for my children to inherit that I wish to leave behind is a HABIT of HUMAN VALUES (LOVE, TRUTH, NON-VIOLENCE, PEACE, RIGHT ACTION) ……….this they WATCH and LEARN from my words and actions based on HUMAN VALUES in their growing years.

That way, in my deathbed and afterwards, they won’t fight each other “dog eat dog” over matters of paper money that can’t buy happiness no matter how much you over-indulge selfishly!

instead they will sit around me in my deathbed and talk about matters of charity and how to help mankind to elevate them from hunger, physical and mental pain suffering, poverty, illiteracy, lack of clean water and the like.

I will close my eyes in peace as they fill my ears with peace!

I love my avian friends, but I don’t spend $300 a month on them. A few suet cakes a month. Maybe some birdseed later.

30 years tips probably have few individual buyers, although a great tool for the right person. You first have to be aware of tips as not promoted much by financial advisors. You have to be not scared off by the volatility but still believe that 30 years of a small real bond return won’t be beaten by stocks, and have to be wealthy enough to be willing to give up the likely better stock returns.

Also the nearly zero coupon tips are likely a better deal for the hold to maturity and spend as a tips ladder even if the years don’t match up exactly.

Buying 2051 and 2052 double to be spend in 2051 – 2054 likely is a better deal (at 0.125 coupon) as no reinvestment risk for interest payments.

I’ll be using a taxable account. I need coupon interest payments to help pay the taxes on the annual inflation adjustment. In higher inflation years this can be important. The 0.125 coupon would not cover the taxes generated by a 1% inflation adjustment. A 2% coupon covers the taxes generated by a 9% inflation adjustment. This assumes a 22% tax bracket. If the yearly inflation hits 13.55% like it did in 1980 I’m be scrambling to come up with the cash.

I appreciate your notes. However, most of your posts cite the highest real yield since ‘sometime after 2008’. While that is true it’s not very useful. Rates were artificially held close to zero during this period & don’t make for a very apt comparison. Rates before and just after the turn of the century are more comparable IMO. Real yields were much higher then.

Thanks for your insight.

Aggressive Federal Reserve intervention didn’t begin until mid-2011, so the period from 2008 to 2011 is relevant, in my opinion. Over a very long period, 2% over inflation has been considered an “acceptable” return on Treasurys. Rates can go higher, I agree.

I really don’t see the appeal of a 30-year TIPS for anyone planning to hold to maturity. The odds it outperforms a broad market index fund over 30 years seems incredibly small. How do they sell $9 billion worth?

Of course, an individual investor in this TIPS almost certainly has a stock market allocation. This fits in the fixed income side of allocation. A TIPS ensures receiving an inflation-adjusted return, which is unique. Who is buying? Mostly foreign central banks, insurance firms, hedge funds.

Pension funds as well, or they should. I am getting a pension when I retire so I am less interested in long term fixed income. Short term fixed income, and effectively short term fixed income like my I Bond stash, meets that need for me to sleep at night should something catastrophic happen.

Because the odds of experiencing a catastrophic loss in the stock market increase with time.

Because with a $100 investment now, I’m assured that I can take my spouse for a half decent dinner on her 68th birthday and collect enough for a cup of coffee per year in the meantime.

I’m definitely a buyer.

Try to think of TIPS as an insurance policy rather than an investment. You buy insurance on your house or car every year. At the end of the year, you don’t say, that was a dumb purchase because I didn’t have something bad happen to me. You say, I protected my downside risk AND got the benefit of the thing I was protecting.

The same is true for a TIPS investment. If you’re right and the US stock market performs magically for the next thirty years as it as for the last thirty, well I get the benefit of my stock investments AND my TIPS insurance policy back, plus 2% real. Great, sign me up for David’s next vacation.

But if you’re wrong and the next thirty years in the stock market look like, say, the Japanese market has for the last 30, well, my “TIPS insurance policy” pays off and I’m not homeless in my old age. In short, it’s not about making a killing it’s about protecting yourself from the worst possible financial outcomes.

The high (2.125%) coupon is not desirable in my case. The odds that my children or widow will remember to reinvest the 2.125% coupon is essentially zero. Instead, I just bought the 2052 912810TE8 because it’s virtually a zero-coupon (0.125%), and the bond factor is still pretty low. The advantage is that it puts the reinvestment on autopilot as virtually all of the “interest” (the inflation adjustment) goes into the principal automatically. If you are of a certain age, this is a factor to consider. If young, not so much from an actuarial standpoint.

If I buy I would be looking for the coupon to cover the taxes on the coupon and inflation adjustment. A higher coupon increases the probability of not being short during higher inflation years.

I’m 68 so the behaviour of heirs is a concern.

The ultimate 1st world problem

Another consideration is that the duration of the 2052 is longer than the 2053 (and presumably 2054) due to its low coupon. Doesn’t matter if holding to maturity but the 2052 will be more volatile. If you’re intending to sell early if real rates drop, then 2052 will be a bigger winner (but also a bigger loser if rates rise).

To David and others,

Is there an age where it no longer makes sense to buy 30 year TIPS?

Assume you are not planning on leaving it to an inheritance, will be purchased within retirement account and will hold for full 30 year term.

Is the age cutoff based on life expectancy or simply comfort level?

See my comment above. Life expectancy is a factor if you have heirs.

Hi David,

How about buying & perhaps ultimately leaving this upcoming 30 year TIP as part of an inheritance to children who might hold the investment to maturity?

I like your idea, but my kids would just sell it off immediately!