By David Enna, Tipswatch.com

After weeks of financial gloom and omens of disaster, we finally had a “Goldilocks” week in the U.S. financial markets. For example:

- Debt-limit crisis? Solved.

- Jobs report? Positive.

- U.S. dollar? Stronger.

- Oil prices? Still falling.

- Stock market? Up 4% in a month.

- Fed interest rate strategy? Temporary pause.

- Inflation expectations? Falling.

All is good, right? But that last one — inflation expectations falling — has me wondering: Do we really think inflation is under control, just 11 months after the U.S. annual rate of inflation hit 9.1%? I am not so sure, but the financial markets continue to bet that inflation will fall to traditional levels … very soon.

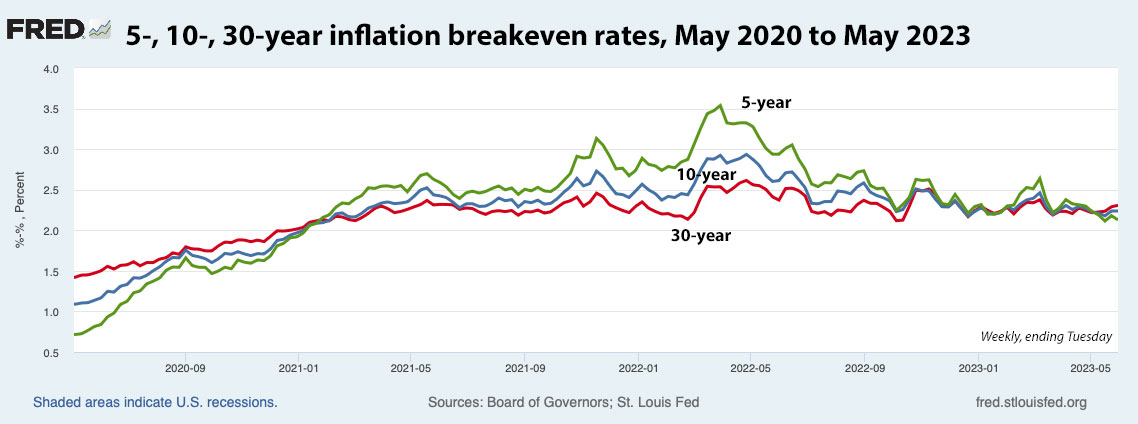

Here is a look at inflation breakeven rates over the last 3 1/2 years, reflecting the difference in yield between a nominal Treasury and a Treasury Inflation-Protected Security of the same term:

One immediate takeaway from this chart is that the inflation breakeven rate is a lousy predictor of future inflation. It measures investor sentiment, and sentiment is often very wrong. Nowhere on this chart can you find inflation expectations signaling future inflation of 9%, 6%, or even 5%, numbers we saw every single month from May 2021 to March 2023.

This chart shows that inflation expectations did widen out in early 2022, catching a hint from the highest surge in U.S. inflation in 40 years. But only the 5-year breakeven ever touched a level above 3%. (Inflation over the last 5 years has averaged 3.9%. Over 10 years, 2.7%. Over 30 years, 2.5%)

I am amazed that the financial markets believe inflation will average less than 2.25% across the entire maturity spectrum of TIPS, from 5 to 30 years. That certainly could happen, but my gut says inflation will run higher, especially if we have entered a new era of global price pressures.

Instead, the markets seem to be pricing in sunny skies (surging stock market) and economic gloom (falling inflation expectations) at the same time.

This view is shared by inflation analyst Michael Ashton, who posted a commentary this week titled, “Is Inflation Dead … Again?” His focus is on inflation expectations through the end of the year:

But here is something that seems very weird to me. Prices of short-dated inflation swaps in the interbank market suggest that NSA headline inflation is going to rise less than 0.9% for the entire balance of 2023. … The market is pricing that between June’s CPI print and December’s CPI print the overall price level will rise 0.23%…less than ½% annualized! …

Headline inflation between June and December last year rose only 0.16%, leading to disappointing coupons on iBonds and producing proclamations that inflation was nearly beaten. Here’s the thing, though. The second half of 2022 it made perfect sense that headline inflation was mostly unchanged. Oil prices dropped from $120/bbl the first week of June, to $75 by mid-December. Nationwide, average unleaded gasoline prices dropped from $5 to $3.25 during that time period. …

A comparable percentage decline would mean that gasoline would need to drop to $2.32 from the current $3.58 average price at the pump. …

Naturally, it’s possible that inflation will suddenly flatline from here. I just don’t feel like that’s the ‘fair bet’.

The rest of 2023

For I Bond investors and Social Security recipients awaiting new COLA numbers, inflation rates from July to December are likely to be disappointingly low. That is highly likely because non-seasonally adjusted inflation generally runs higher than the headline number from January to June, and then lower from July to December. This has been a consistent result over the last several years.

And I agree that the inflation picture is likely to look more rosy by the end of the year, especially for the all-items number, which includes food and energy. The Cleveland Fed is forecasting that the U.S. inflation rate will fall to 4.13% in the May report, coming June 13. That would be positive news, but I suspect it’s an optimistic forecast. It also sees core inflation falling to 5.3% from the current rate of 5.5%.

But inflation-watchers need to realize that these late 2023 numbers could be a head-fake, setting up a time of continued inflation above the Federal Reserve’s target of 2%. If the markets are right in seeing inflation running at 2.24% for the next 10 years, I’d have to agree that the worst of the inflationary danger has past. But we will have to wait and see. And that’s not a gamble I’m willing to take.

Next steps?

Even though short-term nominal interest rates are very attractive today on safe investments, I recommend sticking with some exposure to longer-term inflation protection. I was buying TIPS and I Bonds through a decade of lower-than-expected inflation, and finally in 2021 to 2023 that strategy paid off with much, much higher-than-expected inflation.

We might see U.S. inflation seem to wane in coming months, and it may or may not reflect a longer-term reality. I’m saying it is smart to hold on to some level of inflation insurance in your portfolio.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I am preparing to buy 5-year TIPS reopen this month. The current price is $97.80 with 1.25% coupon. Treasury Direct says “When a TIPS matures, you get either the increased (inflation-adjusted) price or the original principal, whichever is greater”. My question: if hold to maturity with big deflation, is $97.80 or $100 guaranteed?

Thanks.

When you put in an order for $100 for a TIPS, you are guaranteed to get $100 at maturity no matter what happens with inflation, and even if you paid $98.70 at the reopening auction or on the secondary market. However, you will also be paying for additional inflation-accrued principal, so that could put the cost of your investment over $100. Either way, the $100 par value is guaranteed to be at maturity, even if deflation strikes.

I just read all of the above, as always, very helpful and informative. Yes, predicting inflation, stock market, rates, etc. is hard but we do act based on our instincts and risk tolerance. I strongly believe that asset allocation based on our needs is the best strategy without following any percentage splits.. I am going to be 68 later this year, so I have a relatively limited time to recover from another finacial crises. First & foremost, I must have enough liquidity using zero risk, cash like ( US Treasuries, I Bonds, TIPS, CDs, & MM funds) investments, to pay all my bills for the next, at least, 10 years or more (of course this depends on our cost of living – a big topic on needs based vs. wants based living). For the remaining portfolio, I go for equities using low cost, tax efficient broadbased ETFs, such as VOO & VTI, and a handful of stocks ( plan to hold them for years) with bias towards technology (because I spent all my professional life with technology and I think I know what I am doing, while speed learning AL if there is such a thing, :)) & healthcare (favorable demographics). In short, a barbell approach. Specifically, interested only in: 1. <= 10 Year TIPS; 2. will continue to buy I Bonds, like I have been buying for the last 12+ years or so, for a long time; 3. Love taking advantage of T Bill yields now; and, as I said before, it will take longer than most think in bringing inflation close to 2%, so we have the next 18 to 24 months, or longer, to have fun with 1-2 years US Treasury yields. Yes, it will be intresting to see what impact upcoming large auctions have on the short end of the yield curve as the US Treasury manage their cash needs. BTW, I started buying TIPS with some conviction only after I joined this blog last year. There is so much to learn.

If the implication is that holding stocks for years decreases the risk, I would suggest professor Zvi Bodie’s refutation of this fallacy.

Yes, rebalacing can certainly help control the risk. Unfortunately, my greed and fear comes in the way of timing the rebalancing AND I am not a fan of Robo or automated rebalancing. However, going forward, I am trying to follow the “take profits” mantra and don’t look back. I try not to buy speculative stocks, though, as a confession, at times, I have been unable to resist the temptation…well, this blog is not about stocks…so apologies for digressing.

Rebalancing controls the risk. It doesn’t eliminate it. 2022 was the classic example, with both stocks and bonds declining sharply.

Len, you can help control the risk of stocks (or any investment) by rebalancing.

If we think of wealth in terms of ‘ utility’ then this Wall Street myth was disposed of circa 1974 by Paul Samuelson. Or are we keeping the number of years of annual expenses bet on the risky asset constant?

I try not to predict inflation and interest rates., unless I really have to. My strategy is to stick with very short duration T-bills (4 and 6 months), which also happen to pay the highest rates now. I sort of ladder them. I buy new T-bills so that the last day of settlement is the exact day when the old one matures, just about every month.

But I do have to watch for the inflation top. This is difficult, because it is more-or-less a prediction of lower future rates. Late last year, there was some notion that inflation had peaked, so I bought a bunch of longer term (three year) brokerage CDs, which were paying about 4.9%. It was a head fake on inflation, as it started up again. Core CPI turns out to be very “sticky” (an economics term for when some change they expect to happen but does not). So I have probably 80% in very short term T-bills. They are easy to unload if necessary, no commission, high liquidity. So far I have kept all my T-bills to maturity.

JOLTS data suggest employment is still very strong. Core inflation is running at 5% or so. Powell will keep raising, especially if he wants to get core CPI down to 2% as he says (good luck with that). If he stops raising, he will appear to have capitulated to the stock market. The stock market is fairly easily manipulated by the big players, so of course they will push for lower rates. The numbers I watch are JOLTS, core CPI, and core PCE. Higher, longer.

A question about terminology. When a phrase like “headline inflation is going to rise less than 0.9% for the entire balance of 2023” is used, does it mean the inflation rate will drop from 5% (or whatever the latest print was) down to 0.9%, or that it will rise 0.9% from the current print, say to 5.9% in this hypothetical? Or something else? In other words, when you say “inflation is going to rise,” do you mean the price level is going to rise by x per cent, or rate of inflation is going to rise by x percentage points? Or something else?

It does mean a 0.9% increase across all remaining months of 2023 — May to December. Last year we had exceptionally high inflation in May (1.1%) and June (1.37%). But then, from July to December, inflation increased just 0.17% in total across those six months.

Thanks, but still don’t get it. So are saying with “from July to December, inflation increased just 0.17% in total across those six months,” that the annualized rate of inflation for those six months was around 0.34%? Seems impossible. If true, it’s a big victory for the Fed. Once again, when you say “inflation increased” by x amount, do you mean the price level increased, the inflation rate increased, or something else? (This is just a terminology question. Sorry if I am being dense!)

The non-seasonally adjusted inflation index for July 2022 was 296.276 and for December 2022 it was 296.797. That’s an increase of 0.176%. However … that turned around in 2023, with inflation up 2.2% from January to April. But still, you can see the trend with annual inflation falling from 9.1% in June 2022 to 4.9% in April 2023.

OK, I think I get it now. When you say “inflation increased” by x amount, you are saying the price level increased by that amount. You are not saying the inflation rate increased by that amount.

I know most investors often use laddering and diversification as opposed investing whole lump sums into bonds of a particular duration.

But I have a sizable lump sum of cash sitting in a taxable MM account that needs to be invested. I’d like to safely lock it away for 10 years while yields are relatively good, with my sole purpose being to preserve it’s buying power (rather than attempting to beat inflation). I don’t expect to need this money before maturity. My selected choices are:

10 year TIPS bought at auction

10 year Bank CD (fdic insured)

10 year Treasury Note

Despite taxes (if inflation gets too high), wouldn’t the TIPS obviously be the closest “guarantee” if my only goal is to preserve buying power for the 10 years? I understand that if inflation does subside and remain lower (along with lower interest rates) over the 10 years, the other two options will turn out to be the better investments, but with the primary goal being as stated, isn’t the TIPS obviously the safer bet? And isn’t any credit risk as low as it gets and the exact same for all three?

Laddering (two auctions annually) has proved superior to any other strategy I have tried over the years for TIPS. Some would say direct obligations of the Treasury are safer than FDIC insured accounts but I can’t imagine what disaster scenario they envision. I am sticking with TIPS for inflation protection.

I’d agree that a direct Treasury obligation is “safer” than an FDIC-insured account, but the difference is so close to zero that it doesn’t matter. Treasurys avoid state income taxes, a nice plus.

I’d agree if your goal is to preserve buying power for 10 years, without concern about the overall nominal return, the 10-year TIPS looks like a great option. It will outperform official U.S. inflation by 1.5%. This is the reason I have been trying to stretch out maturity dates to up to 20 years to lock in attractive real yields. But I am not working with a lump sum all at once.

Thank you for replying, David. Regarding the lump sum problem I have: Since although TIPS YTM is fixed upon purchase, the principle is going to self adjust with inflation ( interest will begin to rise), as opposed to regular Treasury Notes and CDs, where principles do not “self adjust” at all with changes to inflation/interest rates, making laddering at least somewhat less important with TIPS if sole goal is protecting buying power. Is my thinking valid here?

Good points I would say. But I long ago gave up trying to anticipate changes in interest rates or inflation. The experts? Just guessing it becomes obvious. ” It’s tough to make predictions, especially about the future.” The late, great, Yogi Berra.

I’m with you, very skeptical that the inflation dragon is slain. Money supply still looks very high, and the debt ceiling has been raised – how will that make inflation go away?

Agree the breakeven TIPS inflation numbers look much too low. You’d think there would be an implied insurance premium for unexpected inflation protection.

“I’m saying it is smart to hold on to some level of inflation insurance in your portfolio.”

That last sentence seems like your entire overall thesis. Not only does it makes sense, but it reached the general public consciousness the last two years, particularly as I Bond rates soared. This raises three important questions:

1) Why can’t one just wait until inflation (say above the Fed’s target rate) rears its ugly heading and then invest in inflation protected investments like TIPS and I Bonds at that time?

2) Assuming most, if not all, of your readers take your concluding statement at face value, what percentage of a portfolio do you recommend for inflation protection?

And here’s a question that’s a little whimsical (and of course unknowable but fun to ponder):

3) If 2022 was the year of buying I Bonds and TIPS, and 2023 is the year of buying T-Bills in the 13-26 Week range, what is 2024 going to be year of? The stock market?

Great questions:

1) TIPS and I Bonds are unique investments in that they often become a “better deal” as inflation rises. For years, when inflation was low, TIPS had negative real yields and I Bonds have a fixed rate of 0.0%. Now TIPS and I Bonds are more attractive, certainly. But with I Bonds, it’s wise to by them every year anyway, because of the $10,000 purchase cap.

2) My personal investment goal is to have 15% of my portfolio in inflation protection. That was hard to do over the last decade when TIPS were unattractive, but easier today. (I am probably close to that goal, but not quite hitting it.)

3) I have no idea where the stock market is heading, but I devote 35% of my portfolio to low-cost stock funds and re-balance when needed. A wild idea is that medium- to longer-term bond funds could do very well in 2024 if the economy tanks and the Fed swoops in with a rescue.

Interesting that you settled on 35% equities. The long time allocation of the highly successful Wellesley Income Fund (since 1970).

I owned that Wellesley Fund for years, but moved on when I converted my entire traditional IRA to fixed income.

I think the mistake that is made, every asset needs to keep up with inflation during inflation.

Stocks pay you for inflation before it happens. Ibonds and Tips pay you when it is here then these go back to nothing like your stocks did during inflation. For many years my Ibonds paid the low fixed rate(while the market zoomed). Volatility is a different issue.

Useless to try to forecast inflation. Why bother? All that matters is do you want to be long or short an inflation option at these prices? In the long run equities will do better depending on your entry price. Simply put these prices are too high to work out in the not too distant future. Besides if you’re not going to be in 100% equities, you have to hold something else,. TIPS for the bill

Welcome back from vacay. Looks like we avoided the debt ceiling debacle!

It will be interesting to watch Treasury markets this week, because Treasury will be ramping up auction sizes to load up its reserves. Should be plenty of demand at these interest rates, though.