By David Enna, Tipswatch.com

As expected, rising gasoline prices pushed U.S. inflation higher in August, rising a seasonally-adjusted 0.6% for the month and increasing 3.7% year-over-year, the Bureau of Labor Statistics reported today.

Core inflation, which removes food and energy, rose 0.3% for the month (higher than the expected 0.2%) but annual core came in at 4.3%, lower than the expected 4.4%. That most likely means core inflation was close to expectations, before rounding.

Nothing too shocking here, but the bump higher in annual all-items inflation from 3.2% in July to 3.7% in August is certainly an unwanted trend. Gas prices are felt immediately by the consumer, something the Fed and Biden administration can’t ignore.

The BLS noted that the rise in gasoline prices (up 10.6% for the month but still down 3.3% year over year) accounted for more than half the all-items increase in inflation. Shelter costs were the largest factor in core inflation, increasing 0.3% for the month and 7.3% for the year. Shelter costs have increased 40 consecutive months, the BLS said. Other items from the report:

- Food at home prices rose a moderate 0.2% and are now up 3.0% year over year.

- The index for dairy decreased 0.4%.

- The energy index as a whole was up 5.6% for the month.

- Apparel costs rose 0.2%.

- The index for hospital services rose 0.7%.

- Prescription drug costs rose 0.4%.

- Costs of motor vehicle insurance rose 2.0%, the biggest one month jump since 1976.

- Airline fares declined 8.1% but are still up 4.9% year over year.

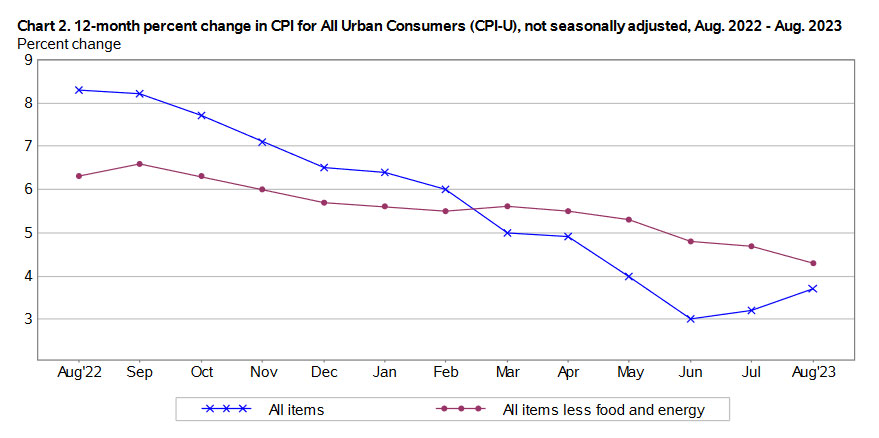

August’s price increases came a year after inflation slowed dramatically in 2022, primarily triggered by a deep fall in gasoline prices. Now that trend is reversing. Here is the 12-month trend for all-items and core inflation, showing that core inflation continues to gradually fall while the trend has turned upward for all-items inflation:

What this means for TIPS and I Bonds

Investors in Treasury Inflation-Protected Securities and U.S. Series I Savings Bonds are also interested in non-seasonally adjusted inflation, which is used to adjust principal balances for TIPS and set future interest rates for I Bonds. For August, the BLS set the inflation index at 307.026, an increase of 0.44% over the July number.

For TIPS. The August inflation index means that principal balances for TIPS will increase 0.44% in October, after rising 0.19% in September. Here are the new October Inflation Indexes for all TIPS.

For I Bonds. The August inflation report is the 5th of a 6-month string that will set the I Bond’s new inflation-adjusted variable rate, which will be reset Nov. 1 for all I Bonds (the starting date depends on the original month of purchase). Inflation from April to August has increased 1.72%, which at this point would translate to a variable rate of 3.44%. But one month remains.

If non-seasonal inflation increases 0.2% in September, you’d get a variable rate of 3.84%, higher than the current 3.38%. Nothing is certain, of course.

Here are the data so far:

What this means for Social Security COLA

The Social Security Administration uses a different inflation index — CPI-W — to determine the next year’s cost-of-living-adjustment. And it looks only at the average of three months of data, from July to September. For August, the BLS set the CPI-W index at 301.551, an increase of 3.4% over the last year.

For the COLA, the only 2022 number that matters is the three-month average from July to September 2022, which was 291.901. The average of the July and August CPI-W indexes was 3.0% higher. One month of data remain. I have been projecting an increase in the range of 3.0% to 3.2%, which could end up a bit too low.

What this means for future interest rates

The Federal Reserve has consistently signaled that it plans to hold short-term interest rates steady at its Sept. 19-20 meeting of the Federal Open Market Committee. While this August inflation report could deliver a psychological jolt to the U.S. consumer, the Fed will probably view it as “expected.”

However, core inflation of 4.3% is unacceptably high, so the Fed must continue its commitment to keeping rates at high levels, probably well into 2024. From today’s Bloomberg report:

The report complicates the picture for Fed policymakers, who meet later this month to set rate policy. While they’re likely to look through a temporary bump in energy prices, the shelter component is still running hot and gains across other categories could give them pause. The broader economic picture could also support another hike: The labor market, while showing cracks on the margin, remains tight.

From the Wall Street Journal:

Fed officials signaled last week they were preparing to hold interest rates steady at their meeting next week, and Wednesday’s inflation report isn’t likely to change that outcome. Whether it is enough to lead officials to raise interest rates again in November or December largely depends on whether inflation firms up in the coming months.

If gas prices continue to rise and eventually spread an inflationary effect to food and transportation costs, the American consumer will feel the pinch. And demands for higher wages would likely follow. That is something the Fed won’t be able to ignore.

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

I am using the calculator at tipsladder.com to help construct a 10 year TIPS ladder. One of the choices offered by the calculator is whether I want the bonds for each year with the “best yield” or the “lowest inflation adjusted principal”. As expected, the overall ladder using bonds with the lowest inflation factor has a slightly lower yield of 2.29% vs 2.36% for the best yield ladder – both calculated as the entire ladder’s XIRR (i.e. extended internal rate of return).

I understand why the higher inflation adjusted bonds provide a lower yield ( i.e. they haver farther to fall if there are extended years of deflation), but my question is how to evaluate this difference. How much higher yield should I expect to offset the greater deflation risk built into the best yield bonds?

With the 10 yield approaching 1.9 percent in mid September, would you guess at this point that the fixed portion of IBonds will likely be higher than the current 0.9 percent set through October. I know we have several weeks to go before the 10 year yield can be evaluated..

My guess is that the fixed rate will rise. Conditions can change, though.

David, what are your thoughts on todays 10 year TIPS announcement?

I will be posting a preview article on Sunday morning. Real yields have dipped a little this week but that 10-year still looks attractive, at about 1.89% real yield and a price of about 95.35. It will be interesting to see how yields trend before next Thursday.

Does it make sense to sell a shorter term TIPS and use the money to extend out in TIPS?

For instance, I bought quite a bit of April 2027 TIPS at 0.96% which sounds low now. If I sell some of that position and buy a July 2032 TIPS at 1.93% with the proceeds, do I essentially wind up getting 0.96% through April 2027 and the 1.93% thereafter (minus some modest bid/ask spread on the sell)? Or perhaps this cannot be a clear answer because it depends on what the path of the money that was coming out in April 2027 takes out to April 2027. I am clearly confused.

Probably this has been covered in another column in this excellent site. If so, I’d like to get a link to that.

My suspicion is that you would have to sell the April 2027 at somewhere in the range of a YTM of 2.14%. That was the Real Yield Rate listed for a 5 year yesterday.

https://home.treasury.gov/resource-center/data-chart-center/interest-rates/TextView?type=daily_treasury_real_yield_curve&field_tdr_date_value_month=202309

Might be a bit more or less depending on a number of factors including only three and a half years left out of the five. So you would be trading off that against the gain in real yield on a different TIPS replacing it.

Expanding a bit on my reply. That April 2027 TIPS (91282CEJ6) was listed for offer on my trading platform with a yield to maturity ranging from 2.199 to 2.25% depending on minimum quantity purchased. That is versus the yield you stated you purchased it at of 0.96%, so you would have to offer it cheaper to make up for the higher going yield. For example, going by the sell offers I see listed, selling $5,000 face value with $2.81 accrued interest owed to you might get you a total of $5020.32 (less commission if any) at a price of a bit under $93 per $100 face value.

Thanks Paul. Still not clear on the total calculation which might boil down to what the real yield is after paying the penalty in the previous buy-sell. Probably I should just hold to April 2027.

This position represents just 13% of my full current inflation adjusted bonds (iBonds + TIPS). The rest is at more favorable rates.

I don’t have a strong opinion on this because I don’t ever sell a TIPS before maturity. Both of these TIPS are going to be trading at fair market value, so you in essence would be extending your maturity out five years. The April 2027 TIPS appears to be trading at about 92.50 but has an inflation index of 1.081 so you’d probably just about break even on the sale. I own that April 2027 TIPS, too (I bought it at the original auction and reopening). I track par x inflation index and my current accrued principal is about 8% above my cost. That TIPS, issued in April 2022, has benefited from very high inflation in the following months.

Thanks. I will just hold the position. That rate might be low in today’s market but as a retiree I just look for a decent real return.

I also own this TIPS and plan to hold it, as I do for all, to maturity. I will like to share the obvious on Brokered CDs, Bonds, I Bonds, and TIPS. These products, in our portfolios, show mark to market pricing and change all day. As interest rates have been going up, there is a lot of red for our such holdings. If we bought them to keep them to maturity then it is all noise. However, if we decide to trade before maturity and it shows red, then we need to take into consideraton recovery of the negative plus more from the new buy to justify the trade. Just stating the obvious…best

Agree.

The trend for CPI-U has me thinking we could see a November I-Bond composite rate of 4.75-5%. That is enough for me to wait for that November 1 rate and not buy in October. That final reading, and then the elusive fixed rate will be deciding factors!

I agree. With real rates higher we could see a bump in the fixed rate for those yet to make any 2023 purchases.