Real yields at 2% are too good to pass up. Or am I wrong?

By David Enna, Tipswatch.com

OK, it’s a silly headline. I am not really day-trading in the Treasury and fixed-income markets; I’ve only been buying and not selling. But I have dramatically stepped up purchases in the last four months.

All this started in mid-2022, as the Federal Reserve began ratcheting up short-term interest rates. At that time, I worked out a strategy to space out purchases of 13- and 26-week Treasury bills and then roll the investments over, always allowing access to part of the money within 4 weeks. I wrote about that strategy in July 2022 and followed up in August 2022. Those investments are still rolling over, now yielding 5.5%+.

At the same time — mid 2022 — I began liquidating my holdings in Schwab’s U.S. TIPS ETF (SCHP) and very gradually began using that money to buy individual TIPS, both at auction and on the secondary market. Real yields were rising, finally, and by November 2022 had hit decade-plus highs. Unfortunately, that trend reversed in the early months of 2023, with the 10-year TIPS real yield falling from 1.73% on Nov. 3, 2022, to 1.06% on April 4, 2023. So my buying spree slowed down.

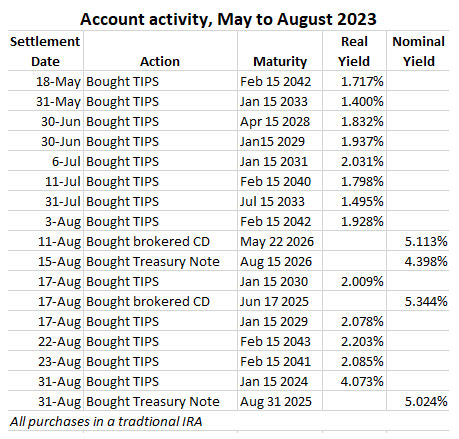

Fast forward one month to May 2023 and real yields again began rising, up more than 40 basis points by the end of that month. So I began buying TIPS again, and a bit more aggressively. As it turned out, a new strategy formed: to build a TIPS ladder through the year 2043, with near-equal amounts in each year. To do this, I began liquidating my holdings in Vanguard’s short-term TIPS ETF (VTIP).

I’ve been doing this in a traditional IRA brokerage account at Vanguard, so taxes are not an immediate concern. My strategy combined buying longer-term TIPS (5 years or longer) combined with some nominal investments in the 2- to 3-year range, to prepare for paying future RMDs from this account. Plus I will need investable money in 2024 through 2029 to buy 10-year TIPS in each of those years to complete the ladder. (There are currently no TIPS maturing from 2034 to 2039.)

Here is what I have been doing since May 2023:

My ladder-building strategy is nearly complete, but I am still looking to fill out the years 2040 to 2043 with amounts equal to the earlier years. I am hoping to nail down 2.0%+ real yields for each of those investments in coming weeks. Some days I can find them on the open market; most days I can’t.

On the nominal side, I have been looking for decent yields to provide cash in my early RMD years (2026 and 2027). This IRA account also has a 20% holding in Vanguard’s Total Bond ETF (BND) and 20% in Vanguard’s Wellington Admiral (VWENX). So I have some flexibility for those future RMD withdrawals.

And I should point out that about 10% of my TIPS are old-school purchases that remain in a taxable account at TreasuryDirect. All those, except one, will roll off by 2029.

What is the strategy?

Any investment can look dumb in a few months. I could have been in cash for the last 12 months and just bought all these TIPS at the top of the yield cycle last week! But here’s my advice: When you are putting your money into a very safe investment with a known decent return: Buy without regrets. When you see real yields that are historically attractive, go ahead and invest. As long as you have a plan.

Yields could keep going higher, obviously. Maybe even much higher if you take a dire view of the U.S. borrowing needs in the next few years. Site reader Amit this week provided a link to this video, laying out a very bearish view of the U.S. bond market:

I have no idea who these guys are or anything about their “All-In” podcast, but the speaker, David Friedberg, makes valid points about the potential extreme level of borrowing needed to fund U.S. deficits in the near future. That could lead to higher nominal yields, which would also drag real yields higher, most likely.

So there is always the possibility that buying at today’s decade-high real yields could look bad into the future. But because these investments are Treasury Inflation-Protected Securities, if held to maturity they will deliver a return of about 1.8% to 2.0% above inflation. That is a certainty.

These investments are part of an asset allocation in a single account — a traditional IRA — that just needs to keep pace or exceed U.S. inflation for the investments to provide what I need: A stable flow of cash until I reach age 90. So I am buying now to lock in that real return, an opportunity we didn’t have in the decade-long stretch of ultra-low yields.

I know a lot of readers are also adopting this “safe-withdrawal” strategy, first promoted by financial author Allan Roth in his October 2022 article, “The 4% Rule Just Became a Whole Lot Easier.” This strategy, as Roth notes, is only possible when real yields are above 1.7% — the range we are seeing today.

So with that in mind, I have been acting to build this ladder of very safe TIPS investments through 2043. It’s not day-trading, but it has become an obsession, I’ll admit.

• Now is an ideal time to build a TIPS ladder

• Confused by TIPS? Read my Q&A on TIPS

• TIPS in depth: Understand the language

• TIPS on the secondary market: Things to consider

• Upcoming schedule of TIPS auctions

* * *

Feel free to post comments or questions below. If it is your first-ever comment, it will have to wait for moderation. After that, your comments will automatically appear. Please stay on topic and avoid political tirades.

David Enna is a financial journalist, not a financial adviser. He is not selling or profiting from any investment discussed. I Bonds and TIPS are not “get rich” investments; they are best used for capital preservation and inflation protection. They can be purchased through the Treasury or other providers without fees, commissions or carrying charges. Please do your own research before investing.

There is an argument against buying a TIPS ladder 10 or more years out. With a long term investing horizon of 10 or more years, it’s practically guaranteed you will do better with equities. Especially 15 to 20 years. What do you think?

I’d agree that low-cost stock index ETFs are likely to outperform a TIPS ladder over 10+ or 15+ years. That’s why I maintain a 35% asset allocation in those EFTs, mostly in taxable accounts where they get some tax advantages. My overall exposure to TIPS and I Bonds is about 15% of my total portfolio; that has long been my target and I am finally reaching it. The idea of a TIPS ladder is to ensure safe, predictable, inflation-protected future withdrawals, all the way up to age 90 for me.

All this work for 15% of your portfolio? 🙂 I’m impressed in a positive way because you’ve helped a lot of people understand TIPS. But I’m also surprised that you haven’t fallen more totally in love with your “anvil.” (The way I tend to do.)

Ah yes … I don’t pay any attention to the stock market and don’t trade stocks. However, “my” portfolio includes my wife’s holdings, and she owns zero TIPS. So It all works out to 15% in inflation protection.

We built our 25 year TIPS bond ladder for a couple reasons: extremely attractive real YTMs (avg 2+% over the term); and the intention to increase our equity allocation over time with some of the maturing proceeds (currently 30/70 with the intention to arrive at 70/30 in 25 years). This allows us to sleep well at night during market gyrations, plan for future RMDs to minimize taxes, and build up the Roth IRAs prior to starting Social Security. Personally, I think TIPS/I-Bonds and low-cost, cap-weighted Total Stock Market ETFs are the only risk-adjusted free lunches available to regular investors, and I am trying to take full advantage of them.

I get why TIPS are arguably a risk-adjusted free (or better IMHO) lunch, but not why you say that of low-cost, cap-weighted Total Stock Market ETFs. You may mean that diversification is a free lunch, which is true, but only up to a point, due to the correlations going to one in a crisis, meaning they are diversified within a category (equities) but not truly diversified across asset classes. In any event, they are still much riskier than TIPS. At least that’s how I see it, but I’d certainly be interested in your insights and those of Tipswatch if he cares to comment. Thanks!

BondGuy and Rick, I do wonder whether the cap-weighted total U.S. stock funds are getting more risky because of their heavy weighting in about 7 stocks, which dominate the index. Still, probably the best alternative for the stock portion of the portfolio. I also have a holding in VIG, Vanguard’s dividend appreciation ETF, total return of -9.8% in 2022 and now up 8.7% YTD. Vanguard’s total stock (VTI) was down 19.5% in 2022 but now up 18.4 this year.

I agree the equity portion of our portfolio is where we take most of the risk hence the smallish portion right now to minimize sequence of returns risks. As for why a TSM portfolio, I am future-proofing in case of mental impairment or a financially dis-interested widow (my spouse). By owning the haystack, I don’t have to go looking, hoping, praying for the needles (i.e. out-performing stocks). As for other asset classes (eg. gold, commodities), I am trying to keep the portfolio simple for later me/spouse. I am essentially DCA’ing back into stocks from the TIPS umbrella for peace of mind because the current market seems over-bought (a form of systematic market-timing). It may not be maximizing returns if, instead, I were to get lucky and pick the right stocks/sectors at the right time. But, I believe the US stock market as a whole will generally rise over the 25+ year timeframe, beating both inflation and current TIPS YTM returns. In the end, I hope we will be well-positioned with a 70/30 portfolio to meet later-in-life costly, unknowable expenses like Long Term Healthcare. But what do I know, I am just some person on the internet (;-).

Excellent, thoughtful response. Thanks.

Pingback: Experiment: Let’s try out a very short-term TIPS | Treasury Inflation-Protected Securities

Not sure this is the place for this comment, but TreasuryDirect just sent me a survey about bond names that led me to believe they are considering changing the names of their bonds— specifically I-bonds and EE-bonds. Seemed rather silly to me. Wondered how wide they cast their net on this.

Perhaps they could be named “Grandchildren’s Debt” US bonds.

David,

A bit off topic, but could it make sense to purchase TIPS on the secondary market which are maturing soon? The WSJ shows yields over 3% for TIPS maturing in 2024. With inflation, these yields might be better than t-bills. The risk of deflation seems very small. Thanks!

My guess is that these very short-term TIPS will end up with a return similar to a T-bill. I looked at the TIPS maturing Oct 2024, with a coupon rate of 0.125% and an inflation index of 1.1889. If you buy $10,000 par you would pay about $11,495 for about $11,889 of principal. From then on you’d earn 0.125%. Your total return over 12 months would be 3.4% plus whatever inflation you see in the next year. If inflation runs at 3.0%, your return would be 6.4% over 14 months, for an annual return of 5.5%, about the same as a 1-year Treasury right now.

Hi David, I’m seeing a number of these trading on Schwab, under par (98.8) and with YTMs over 3%: “US Treasury TIP 2.375% 01/15/2025”

If inflation runs at 3.0%, wouldn’t these be quite attractive compared to anything else, or what am I missing? Thanks!

Thanks David! It makes sense that the short-term TIPS have essentially the same return as T-BILLs. The TIP Roam identified does look marginally better.

Roam, there are two tips maturing in Jan 2025. I looked at CUSIP 912810FR4. This one has a coupon rate of 2.375% and an inflation index of 1.61831. So if you buy $10,000 par you are actually buying $16,183 in principal. The discounted price is 99.070 and for a $10,000 purchase, so you’d be actually paying $16,012 for $16,183 of principal. That’s an immediate gain of 1.13%, which annualizes out to about 0.85%. Add that to the coupon rate of 2.375% and you get to a 3.22% annual return. If inflation averages 3% over that time, your return would be 6.22%, better than a 1-year Treasury. Of course, if inflation averages only 2.2%, you get to 5.42%. The market is betting on 2.5% inflation or less, it appears.

Thanks so much, that helps! I was wondering because my sense was that this purchase would have a better return over a similar timeframe than the previous example above in response to John, all other things considered equal.

Quick question about principal calculation: “…with a coupon rate of 0.125% and an inflation index of 1.1889. If you buy $10,000 par you would pay about $11,495 for about $11,899 of principal.” Shouldn’t that be $11,889 of principal?

Similarly, “This one has a coupon rate of 2.375% and an inflation index of 1.61831. So if you buy $10,000 par you are actually buying $16,193 in principal.” Shouldn’t that be $16,183 of principal?

Jim, it looks like my typing skills were off this morning. Your numbers are right and I corrected the comments.

I loved this article! Wonderful to read your story, as I think many readers, myself included, have had quite the journey buying TIPS/Nominals as the yields have risen over the past two years, and it is quite helpful to hear how others have executed their plans. And it is very true we cannot kick ourselves for earlier buying at lower yields – who knew what would happen (or continue to happen).

David, what are the pros and cons of selling the Apr-22 5-year TIPS (0.125% coupon) and using the proceeds to purchase the upcoming Oct-23 5-year TIPS (which should have a real yield in the 1.9% range)? At the moment, the Apr-22 5-year TIPS has a market price of about $920, which means selling it would result in a loss of about $80 per $1000 bond.

It seems to me that the current market value of ALL TIPS reflects the current 1.9% real yield, so therefore it seems to me a wash, i.e. selling the Apr-22 TIPS at a loss in the expectation of getting a higher coupon rate on the Oct-23 TIPS would provide no benefit and that it’s best simply to hang onto the Apr-22 TIPS to maturity.

Yes, it would pretty much be a wash, because that Apr 2027 TIPS currently has a real yield of about 2.39% and the October 2028 issue could be higher, or lower, or about the same. Probably about the same. The only benefit would be a higher coupon rate (meaning higher current income), if that makes any difference to you. On the positive side, that Apr 2027 TIPS has had an inflation accrual of about 7.9% since issue, so you might actually be above water on that investment.

Karli’s, the inflation adjustment is added to the principal rather than being paid out

David–I am curious if you have thought about whether you will stick with your ladder strategy if/when the Fed has to fight the next recession with qualitative easing (QE) and real yields go back down to zero or below? At that point your TIPs should have a significant premium value above their adjusted principal and you will have to consider the likelihood that if you maintain the ladder intact, that premium value will gradually erode as the economy recovers and real yields increase again.

Nothing is forever.

If the Fed pushes mid- and long-term real yields back toward zero, I will just sit back and enjoy retired life, knowing the ladder will do what it is supposed to do and couldn’t be reproduced again (at that time). The one negative is that the brokerage IRA account will have a much higher value and that will lead to higher RMDs.

That’s one reason why I’ve not committed all my IRA assets to my TIPS ladder. The other assets are available in case RMDs come out higher than expected. they also are available to convert to an annuity if it starts to look like I will outlive the ladder. Or they will be part of my estate. But the ladder is sufficient to cover my needs while it lasts, to age 93.

I completely agree with your gradual approach to adding to your TIPS position, although I think a ladder beyond 10 years might be a bit extreme for me. I think patience will be rewarded in this volatile/uncertain market. If you extend the real yield chart back to pre-2008 financial crisis you will see real yields in excess of 2.60%. So it seems to me that those “normal” conditions may appear at some point in the future. Another reason to go slow and maybe not extend maturities much beyond 10 years.

I see the yield to maturity of 1.96% on the Schwab TIPS area on the February 2041 bond you mentioned. How do I calculate the “real yield”?

View Only US Treasury TIP 2.125% 02/15/2041 YTM

912810QP6 2.125 02/15/2041 Ask 50 102.42000 50 9000 1.961 — 56.300 71,382.610 View

For a TIPS, the yield to maturity you see in these brokerage quotes is the real yield. Note that TIPS has a coupon rate of 2.125%, slightly higher than the real yield, so the price is higher at 102.42.

David-

It sounds like most of what you’ve been doing recently is exchanging TIPS in funds (SCHP and VTIP) for individual TIPS. If so, then it wouldn’t seem to matter much when you did it, since any time TIPS are cheap then the funds you sell to buy them are cheap also – and vice versa.

Am I missing something?

Yes, I am trading the uncertainty of a TIPS fund for the certainty of a hold-to-maturity ladder of TIPS. The fund could actually do better than the ladder (or worse). The point of this ladder is to have defined inflation-protected cash maturing each year.

I understand why you want to build a ladder; I built mine for the same reason. I’m just saying that if you are trading TIPS funds for a basket of TIPS, you don’t gain anything by waiting until yields are high.

In my case, my TIP fund holdings were 80% in VTIP and 20% in SCHP. I got out of SCHP first. So in essence, I have been trading a short-term TIPS fund for a collection of mid- to longer-term TIPS. VTIP was my holding fund for future TIPS purchases, and it hasn’t performed poorly, by the way. Its total return was +5.36% in 2021, -2.96% in 2022 and +1.86% so far in 2023.

Too many moving parts for me to follow. I’ve got a number of accounts laddering out to the end of 2025 with mostly tbills, some notes, some agency bonds and some JPM CDs (5.6%). The non-callable parts are all at 5% or greater (5.537% the highest so far) and the callable parts 5.35 to 5.75%. I think we hit 6% by the end of the year or so and am content to keep the doggies rollin’ out to 2025 eventually to early ’26. Not sure what will happen with the callable parts at the earliest call dates, but I’m happy to get paid a higher than tbill rate until then. I can’t fathom tying up capital till 2043 with the uncertainty of the government’s debt. The only thing I see on that front is that China is way worse off than us. Skip to the 2min mark to see the chart. https://youtu.be/ovvQdCmnCLo?si=wCzucEXJHMzoMP0E

Good luck to us all. We’re gonna need it.

As someone who bought a lot of 2032 maturing January tips ($160k) at ~1.5% in mid July, now 2% a few weeks later, I’m trying to remind myself that the difference between 1.5, 2.0%, or even 2.5% isn’t huge compared to stocks. I bought the 1/2032 tips at 88.32, now at 85.18, so perhaps 4% cheaper. I sold VTI (vanguard total market) to buy the tips at $226, now down to $219, so 3% loss. If I bought this month instead of last month I would have gotten a better tips price but have less money to buy them with.

Unless you are sitting in t bills or a money market fund trying to time the TIPS market real interest rate peak (so lowest price to buy), you also have the other variable of trying to time the peak of the other asset you are selling to buy tips.

The nice thing about holding tips to maturity is there is no sell decision. You only have to market time when to buy at a reasonable tips real positive yield. It could be this is the new normal and we have the next decade to buy positive real tips. It could be this opportunity goes away in the next 1-2 years, or sooner.

from my perspective, something unusual has been going on at Fidelity in the last week when I’ve tried to access info on TIPS trading yields after hours. usually they’ll show ask and bid info for the last trading session, even when bond trading is closed. most recently, when i’ve done a TIPS search on their bond platform i get: “Fidelity’s current fixed income offerings do not match your search criteria or the offering period has closed for this offering. Please try your search again with new criteria or speak to a representative…” wondering if it’s user error on my part, or others seeing same messaging during and/or after trading sessions.

As I have noted before, Vanguard’s bond trading platform is useless over the weekend for secondary market purchases. Probably both brokerages are discouraging use of outdated information from Friday’s close.

I have noticed the same issue the past few days. Remarkably different from the last year…quite frustrating!

On Friday I found Fidelity’s secondary market TIPS platform was down while the market was open. I went to the Fixed Income, Bonds, and CDs page, clicked on the Bonds tab, selected “TIPS (Secondary)”, then tried several ranges of maturity dates, but always got a box stating “No Result Found – There are no results matching your search criteria. Please revise and try again.” Called Fidelity and a customer service agent confirmed there was an issue on their side and they were working on it, but it remained down all day. I’ll try again on Monday and call again if it’s still down.

FWIW, the issue at Fidelity with the secondary TIPS market listings that I pointed out has resolved this week.

I noted in your August 2022 post you mentioned “. . . I would be highly tempted to dive into a 5-year Treasury note if the yield surpasses 4.0% . . . “. With a year under our belts, What are your current thoughts on this idea? It’s over 4% for 3,4,5,10,20 and 30 years now.

The 5-year Treasury note closed at 4.44% on Friday. One issue for me is that I have 2028 pretty locked up, with investments that include a 5-year CD @ 4.61%. Right now I am leaning more toward the 2-year at 5.03%, there is an auction coming Monday. I am more focused now on 2025 and 2026, and then going with TIPS for 2028 and beyond.

At the US Senate Credit Union ($6 to join for lifetime membership with American Consumers Council) you can get a 3-year 5.18% CD (interest compounded daily with posted monthly) for a minimum $1,000. One of the best deals out there.

But taxable by states, right?

Yes, it’s taxable, but still great rate as I expect rates to drop by next year.

I bought a fair amount at 1.5%, but my regret is small compared to what it would have been if they had gone back to 1%. I’m still buying at 2%. That’s enough for me. And for my daughter, over 30 years in her IRA, that’s still more than a 60% increase in real purchasing power, more if one takes into account the compounding of the inflation component, which is automatically reinvested in the principal at 2%.

Newbie question: I’m confused by “…inflation component, which is automatically reinvested in the principal at 2%.” Could you elaborate? Thx

Karlos, The Bond Guy is not quite right. The 2% Yield to Maturity is based on the assumption there is no future inflation/deflation at the time when the TIPS was bought, just the remaining interest payments from the coupon set at auction. The inflation component (Index Ratio in Treasury-speak) affects the principal of the TIPS; but, there is no guarantee what the inflation percentage increase will be, just that your principal will fluctuate up/down based on the non-seasonally adjusted CPI-U and market action. The 2% YTM is only relevant at the time of purchase, it does not compound over time. That’s why you will see gains/losses on individual TIPS holdings daily, on a marked-to-market basis (just like every other bond fund). It is possible, but highly unlikely, that deflation will exist during the entire TIPS holding period from when you bought it. If it did, then you are guaranteed to receive the TIPS par value at maturity (e.g. $100) even if the Index Ratio component puts the value at $90. I hope that helps.

Rick S, well said.

Yes, thx! I understand inflation compounds but I just bought my first TIPS in the last few months so I haven’t seen any interest payments yet and wasn’t sure if I understood how they work.

The interest on the coupon rate is paid semi-annually as a direct payment. The inflation accruals change each day based on the inflation rate two months earlier. Inflation accruals keep building and aren’t paid out until maturity, or when you sell the TIPS.

Thanks for correcting that. What I had in mind is that the coupon rate is applied to the inflation-adjusted principal.