This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

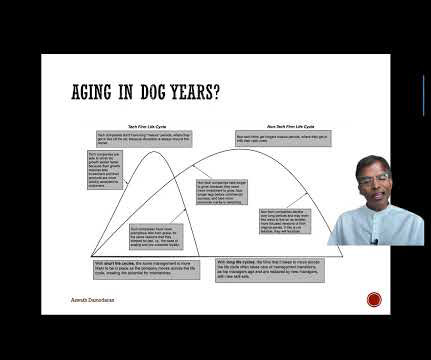

In fact, the business life cycle has become an integral part of the corporatefinance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. In 2022, I decided that I had hit critical mass, in terms of corporate life cycle content, and that the material could be organized as a book.

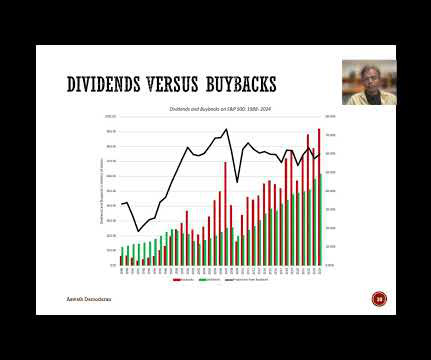

The Dysfunctional Version In practice, though, there is no other aspect of corporatefinance that is more dysfunctional than the cash return or dividend decision, partly because the latter (dividends) has acquired characteristics that get in the way of adopting a rational policy. Data Update 5 for 2025: It's a small world, after all!

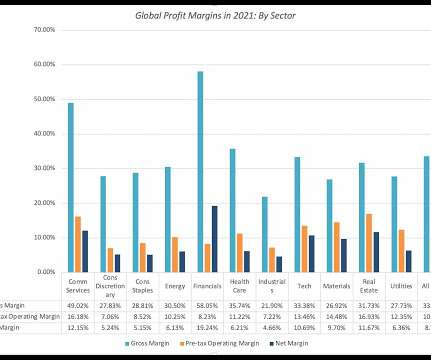

Income from financial holdings (including cash balances, investments in financial securities and minority holdings in other businesses) are added back, and interest expenses on debt are subtracted out to get to taxable income.

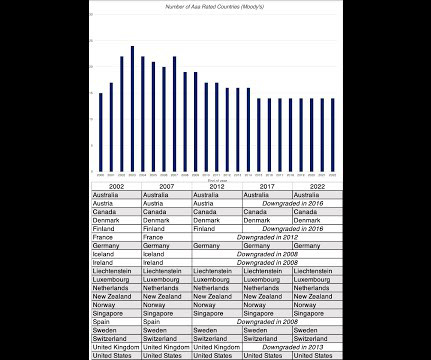

After the rating downgrade, my mailbox was inundated with questions of what this action meant for investing, in general, and for corporatefinance and valuation practice, in particular, and this post is my attempt to answer them all with one post. Why does the risk-free rate matter? What is a risk free investment?

Income from financial holdings (including cash balances, investments in financial securities and minority holdings in other businesses) are added back, and interest expenses on debt are subtracted out to get to taxable income. I will use this data to draw three broad conclusions: Low HurdleRate ?

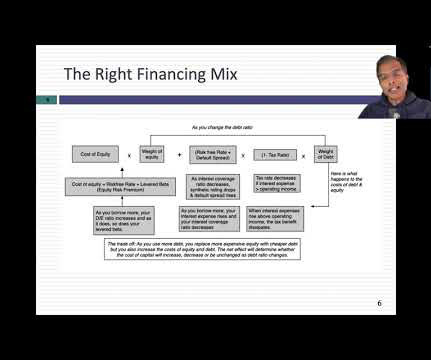

If you have taken a corporatefinance class sometime in your past life are probably wondering how this approach reconciles with the Miller-Modigliani theorem, a key component of most corporatefinance classes, which posits that there is no optimal debt ratio, and that the debt mix does not affect the value of a business.

I went into what’s called corporatefinance, what people would see now as sort of M&A department. CHANCELLOR: Well, I was actually in a sort of subgroup there, which was called corporate strategy. But I didn’t last very long there because I thought I didn’t like corporatefinance.

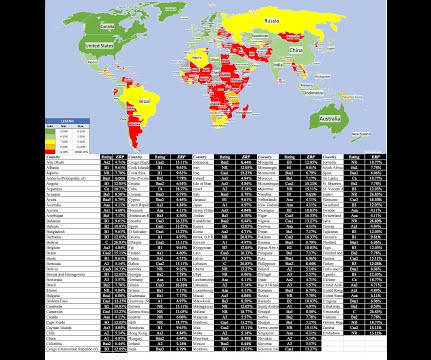

Maplecroft, a risk management company, mapped out the trendline on nationalization risk in natural resources in the figure below: Source: Maplecroft National security is the reason that some governments use to justify public ownership of key resources.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content