This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

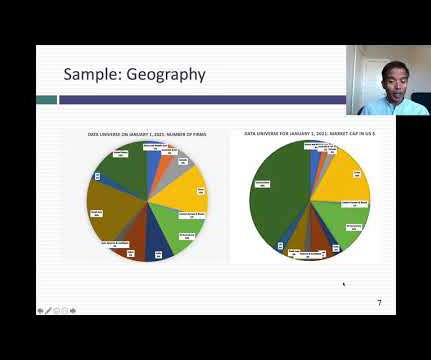

Not surprisingly, the company listings are across the world, and I look at the breakdown of companies, by number and market cap, by geography: As you can see, the market cap of US companies at the start of 2025 accounted for roughly 49% of the market cap of global stocks, up from 44% at the start of 2024 and 42% at the start of 2023.

As I have argued in all four of my posts, so far, about 2022, it was year when we saw a return to normalcy on many fronts, as treasuryrates reverted back to pre-2008 levels, and risk capital discovered that risk has a downside.

The failures of the signal have been variously attributed to low interest rates, accounting mis-measurement of earnings (especially at tech companies), and by some, to animal spirits. Data Update 4 for 2021: The HurdleRate Question. If you buy into this measure of equity risk premiums, consider its limitations.

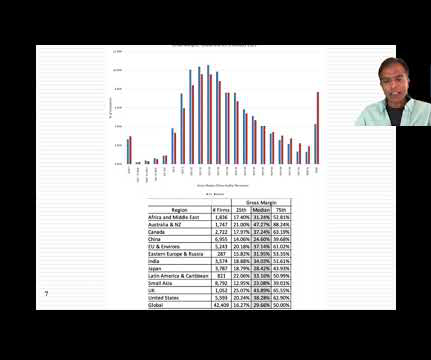

While the universe of companies is diverse, with approximately half of all firms from emerging markets, it is more concentrated in market capitalization, with the US accounting for 40% of global market capitalization at the start of the year. If there is a hole in my sample, it is the absence of privately owned businesses.

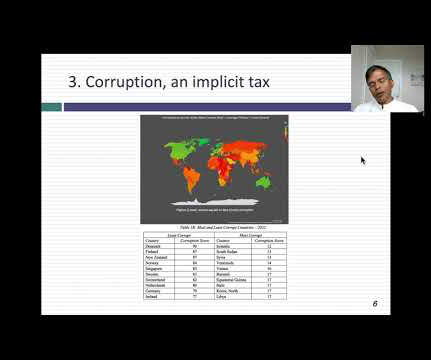

To estimate the equity risk premium, for most countries I start with default spreads, either based on the sovereign ratings assigned by the ratings agencies, or from the market, in the form of sovereign CDS spreads. the riskfree rate in Egyptian pounds is 14.38%.

” look at the Monte Carlo simulations, look at what is the hurdlerate. But we want it on the calendar so that we keep clients and ourselves accountable so that we make sure that those meetings actually do happen. But really the main driver in that first meeting is, “Hey, we’ve got to update the financial plan.

I mean, I used to write about that in this new book where money flows off to the emerging markets when dollar rates are low. They’re actually just buying long dollars, treasuries. Well, the way I see negative rate is it’s a tax on capital, which is instituted by an unelected — RITHOLTZ: Central bank.

So you’ve got, you’ve got a modeling hurdlerate that you need to figure out when you’re adding diversifiers. And instead of replacing a house, you’re replacing exposure like the s and p 500 or treasuries, where historically it’s been really hard to beat the market. The second is behavioral.

Accounting was very difficult. It’s about a 50% fail rate, something like that. You, you mentioned the fed raising rates. What do you see in, in treasuries and the fixed income half of the portfolio? And I remember that first level was tough. I had no finance background. So, 00:08:16 [Speaker Changed] Right.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content