This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Members’ Profile: Rofhiwa Irene Singo In this edition of our CFO Spotlight series, we are featuring Rofhiwa Irene Singo, an accomplished finance leader whose journey is a testament to resilience, adaptability, and impactful leadership. What sparked your interest in finance?

Ensure auditable reporting and compliance The CFO needs to work with other functions like corporate financial reporting, regulatory compliance, tax, treasury, and legal to ensure timely, auditable reporting and financial accounting. CBAM compliance also requires the purchase, management, and surrender of CBAM certificates.

Many nonprofit organizations both large and small need to undergo a financial statement audit every year. Preparing for a nonprofit audit can be overwhelming and anxiety-filled, especially if it’s your first audit or you don’t have a strong and experienced financial team. What is a financial statement audit?

Discover how SAP solutions lay a solid foundation for audits and next level PCAOB or AICPA compliance reviews. While passing each audit is a critically important milestone, companies also should understand that it is only one aspect of ensuring their financial transparency and integrity.

But that’s not quite true—nonprofits face a decision between 2 different accounting methods for tracking their financial activity: cash accounting vs. accrual accounting. Though both systems use the same numbers, looking at those numbers differently can give you a very different perspective on the state of your finances.

Corporate accounting standards are changing, with the Financial Accounting Standards Board adopting new standards in ways companies report on leases, hedging and other financial activity. ” Meanwhile, previous research from Audit Analytics has also revealed that the number of accounting errors among the U.S.’s

A research firm has discovered that the number of material accounting mistakes made by U.S. Massachusetts-based Audit Analytics looked at disclosures from more than 9,000 U.S.-listed For many, the mistakes were discovered when corporate finance teams were changing accounting paperwork to comply with the new U.S.

If you’re like most nonprofit leaders, you’re not researching nonprofit accounting basics to satisfy your curiosity. You need to get a better grasp of your organization’s finances now. The basic accountingprinciples for nonprofit organizations are the same as accounting for for-profit companies. .

The changes to in kind donation reporting are specifically for organizations that follow generally accepted accountingprinciples (GAAP) in preparing their financial statements. Typically, a CPA would prepare these statements as part of a yearly review or audit. What exactly is changing about in kind donation reporting?

The Ascend program is an opportunity for Senior Finance Executives from underrepresented groups to join The CFO Leadership Council. Duanne also developed SELF’s proprietary underwriting method based on ability to repay, designed to provide affordable, unsecured financing to low-and-moderate income populations with low credit scores. “It

All these sources must be carefully managed to ensure compliance with Generally Accepted AccountingPrinciples (GAAP) and guidelines. Understanding how and when to recognize different revenue is perhaps one of the most important but difficult aspects of managing a nonprofit’s finances. Undergo annual financial audits.

Financial accounting: A topic that can easily disorient even the most driven entrepreneurs. However, don't undervalue the significance of comprehending finance for your startup's survival. Familiarity with Generally Accepted AccountingPrinciples (GAAP) is essential.

In this new role, he will serve as one of our in-house experts on existing and emerging nonprofit accounting standards and auditing best practices. In doing so, Zack will help ensure that our clients’ financials are prepared in accordance with general accepted accountingprinciples (GAAP) and their 990s meet IRS guidelines.

How can a small business ensure compliance in reporting without overspending on accounting staff and audits? In general, financial statement compliance involves adhering to established standards and regulations, such as Generally Accepted AccountingPrinciples (GAAP) and the Financial Accounting Standards Board (FASB) guidelines.

Because of their unique structure and operational model, nonprofits must comply with various accounting standards that are, in many ways, different from for-profit organizations. In the United States, these Generally Accepted AccountingPrinciples (or GAAP) are set by the Financial Accounting Standards Board (FASB).

To pass an independent audit. Reporting functional expenses has been required by Generally Accepted AccountingPrinciples (GAAP) since 2017, as detailed in ASU 2016-14. That means you’ll need to present a Functional Expense Report to pass an audit. So you really don’t have a choice, but if you want more reasons….

If you’re looking for info on fund accounting in government here is a great resource for you. Both Generally Accepted AccountingPrinciples (GAAP) and Financial Accounting Standards Board (FASB) 116/117 require at least a minimum level of fund reporting, so you’ll need it in order to pass an audit.

In order to successfully manage the financial health of your nonprofit organization, here are 7 key concepts you should understand: Compliance and Audit Requirements Compliance is the act of ensuring the public that nonprofits are abiding by the rules that allow them to take advantage of tax exempt status and other financial incentives.

Whether you are an educational, charitable, religious, sports, or other public-benefit organization, you need to have a good handle on your finances in order to make the most impact. Yes, they might have a board member or volunteer who takes care of the finances, but they often lack specific expertise in nonprofit accounting.

CFOs rely on robust finance and accounting expertise, backed by years of experience, to boost the organization's financial health. In their capacity, CFOs usually: Engage with departments such as accounting, customer service, and finance. Address accounting and finance issues.

Your business is creating a product or service; finance is not your business. Accountant: If your financial status doesn’t warrant hiring a CFO, you still need financial support; at the very least, you’ll need help with your day-to-day accounting and regulatory compliance. Courtesy of YEC.

But in the accounting world, “financial consolidation” is a well-defined process that includes several complexities and accountingprinciples. Here are the key accounting consolidation steps in the finance consolidation process : Collecting trial balance data (e.g.,

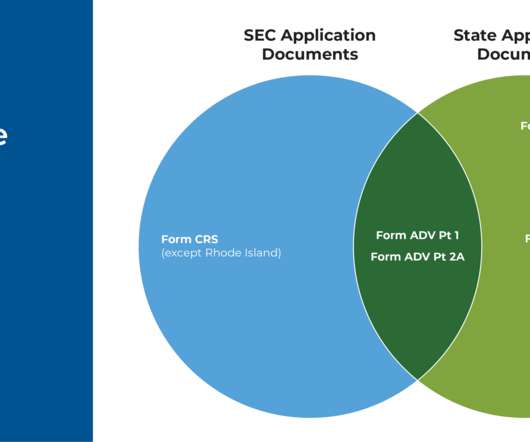

Along with renewing their registration annually (for both SEC- and state-registered firms), firms face a variety of requirements related to their internal finances, fees, marketing activities, and advisor agreements depending on whether they are SEC- or state-registered. RIA Fee Itemization And Surprise Custody Audits.

Sure, your mission should be a priority, but managing finances can’t be neglected either. Without a good grasp of your finances, your nonprofit risks: Exposure to fraud. When creating your fiscal policy, ensure that it complies with the Generally Accepted AccountingPrinciples (GAAP). Collaboration issues.

This form allows the IRS and the general public to track a nonprofit’s finances, management practices, and governance structure. Proper revenue recognition is a core accountingprinciple that ensures proper financial reporting, ensuring that you remain compliant and maintain donor confidence. Get the free guide!

What will our finances look like?" Pro forma financial statements and GAAP It's important to note that, since pro forma statements are based on hypothetical or projected data, they are not compliant with generally accepted accountingprinciples—GAAP statements must be based on actual financial results.

Besides the wasted time involved in chasing down and correcting incorrect revenue recognition, it creates issues with meeting the Generally Accepted AccountingPrinciples (GAAP) standard for financial reporting. Your finance team should review all cash receipts to ensure they are properly allocated to their respective accounts.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content