This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This opportunity allowed me to audit clients like the South African Revenue Service and South African Tourism, as well as manage accounts for Mastercard South Africa. When you’re young, focus on deeply understanding the core accountingprinciples, financial reporting, and regulatory compliance.

Contrary to what many people envision, a nonprofit audit doesn’t usually start with a letter from the IRS. Instead, an independent nonprofit audit is something you choose to build trust in your nonprofit organization. An audit can be a critical step for a growing nonprofit that needs to raise increasing amounts of funds.

Discover how SAP solutions lay a solid foundation for audits and next level PCAOB or AICPA compliance reviews. While passing each audit is a critically important milestone, companies also should understand that it is only one aspect of ensuring their financial transparency and integrity.

Furthermore, accrual accounting is required by Generally Accepted AccountingPrinciples ( GAAP ) because it gives you a more accurate picture of your organization’s fiscal situation and allows for easier side-by-side comparison with financial statements of other organizations. Common accrual accounts include: .

The basic accountingprinciples for nonprofit organizations are the same as accounting for for-profit companies. . So let’s start with the basics, and later we’ll dig into some of the things that make nonprofit accounting unique. . The core principles of nonprofit accounting are the same as for-profit accounting.

Nonprofits rely on a mix of sources for their income, from fundraising, grants, and investments to earned income and individual contributions. All these sources must be carefully managed to ensure compliance with Generally Accepted AccountingPrinciples (GAAP) and guidelines. Undergo annual financial audits.

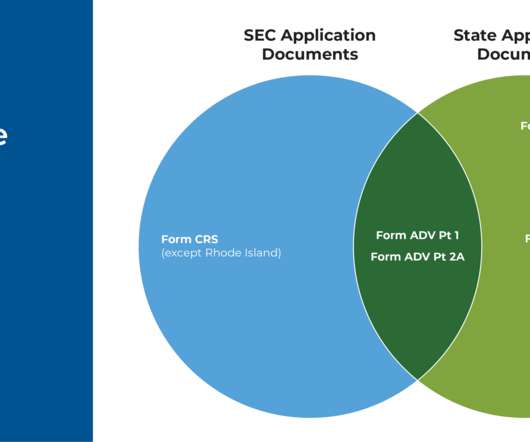

In the United States, Registered Investment Advisers (RIAs) are required to register in one of 2 ways: with the Federal government (namely the SEC) or with one (or more) state securities regulatory agencies. Executive Summary. Guest Contributor. Federal Vs State Registration Application Differences For RIAs. Parts Of Form ADV For RIAs.

Her consulting experience included audit and risk advisory services, project management, business process improvement and information technology, primarily serving financial institutions. Indri Ongko, Controller, Western Technology Investment. Indri Ongko, Controller, Western Technology Investment.

If you’re looking for info on fund accounting in government here is a great resource for you. Both Generally Accepted AccountingPrinciples (GAAP) and Financial Accounting Standards Board (FASB) 116/117 require at least a minimum level of fund reporting, so you’ll need it in order to pass an audit.

Accounting for in-kind donations isn’t just important; it’s required for many nonprofit organizations. . Prepare financial statements per Generally Accepted AccountingPrinciples (GAAP). Submit to an annual audit. You need to track and report in-kind donations if your organization is required to… .

But in the accounting world, “financial consolidation” is a well-defined process that includes several complexities and accountingprinciples. Here are the key accounting consolidation steps in the finance consolidation process : Collecting trial balance data (e.g., Using the Right Tool for the Job.

They could steer your company towards poor financial decisions, like risky investments, inaccurate budgeting, or insufficient cost control. Facilitate risk management, audits, and research. Spot investment and financial planning prospects. What could go wrong if your Chief Financial Officer (CFO) is not effective in their job?

NPOs should track all donations, grants, and investments made to their organization to make sure they are properly accounted for. Proper revenue recognition is a core accountingprinciple that ensures proper financial reporting, ensuring that you remain compliant and maintain donor confidence.

Misuse of funds and poor investments. Your organization has physical assets, including cash, investments, and other tangible property. When creating your fiscal policy, ensure that it complies with the Generally Accepted AccountingPrinciples (GAAP). Is there a need to invest more in particular projects or initiatives?

Compliance: Adherence to accounting standards and regulations, such as Generally Accepted AccountingPrinciples (GAAP) or International Financial Reporting Standards (IFRS). Audit Trail: A record of changes made to financial data and reports, ensuring transparency and accountability.

It helps companies assess their progress, manage risks, and make informed investment decisions. It includes items such as taxes, investments, and income sources. Your finance team should review all cash receipts to ensure they are properly allocated to their respective accounts.

Pro forma financial statements and GAAP It's important to note that, since pro forma statements are based on hypothetical or projected data, they are not compliant with generally accepted accountingprinciples—GAAP statements must be based on actual financial results. Pro forma statements are also used to secure financing.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content