This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The company’s CBAM obligations and purchased certificates have to be accounted for in accordance with global accounting standards like the IFRS or US GAAP. With the Trump administration embracing digital assets, finance leaders need to get educated on the potential risk and reward of cryptocurrencies and stablecoins.

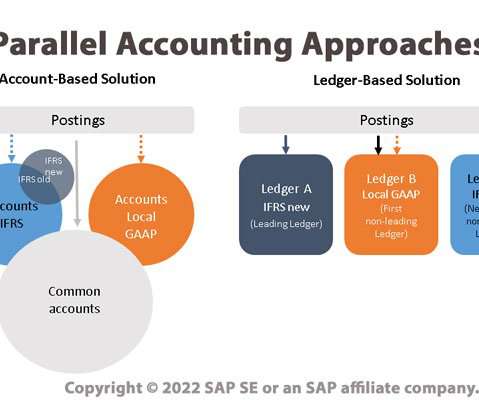

One important side effect of the ongoing trend toward globalization is the need to comply with a range of different accountingprinciples as well as with disparate reporting and compliance mandates. Parallel Ledgers - in which multiple ledgers are used, with an accountingprinciple applied to each ledger.

There are 10 most sough-after shared services skills in the finance and accounting function in the past year, said Gartner recently. Looking for the top finance shared services skills in the same place as everyone else is costly,” said Jessica Kranish, senior principal, research, Gartner. Accounting experience.

Finance organizations regularly face the challenges of meeting strict deadlines and satisfying data quality requirements for closing the books and delivering accurate financial statements. It enables finance teams to automate and accelerate the financial close with minimal IT support. DOWNLOAD NOW.

So now is the perfect time to make sure you report in kind gift donations in compliance with GAAP standards in 2022. The changes to in kind donation reporting are specifically for organizations that follow generally accepted accountingprinciples (GAAP) in preparing their financial statements. Who do the changes impact?

But that’s not quite true—nonprofits face a decision between 2 different accounting methods for tracking their financial activity: cash accounting vs. accrual accounting. Though both systems use the same numbers, looking at those numbers differently can give you a very different perspective on the state of your finances.

If you’re like most nonprofit leaders, you’re not researching nonprofit accounting basics to satisfy your curiosity. You need to get a better grasp of your organization’s finances now. The basic accountingprinciples for nonprofit organizations are the same as accounting for for-profit companies. .

This makes it challenging to create technology that tracks data for fundraising purposes while still following accountingprinciples. Instead, accounting software prioritizes accuracy, standardization, and regulatory compliance. For nonprofits, GAAP ensures transparency, accuracy, and consistency in financial statements.

If you’re looking for info on fund accounting in government here is a great resource for you. Both Generally Accepted AccountingPrinciples (GAAP) and Financial Accounting Standards Board (FASB) 116/117 require at least a minimum level of fund reporting, so you’ll need it in order to pass an audit.

All these sources must be carefully managed to ensure compliance with Generally Accepted AccountingPrinciples (GAAP) and guidelines. Understanding how and when to recognize different revenue is perhaps one of the most important but difficult aspects of managing a nonprofit’s finances. Get the free guide!

Anthony Noto Anthony Noto, a famous finance executive and former NFL exec, now wears the CEO and CFO hats at a fintech company named SoFi. His main job is to handle all money matters at SoFi, like planning, accounting, and dealing with investors. Ianniello is well-known in finance circles. As the Director of Amyris Inc.,

Financial accounting: A topic that can easily disorient even the most driven entrepreneurs. However, don't undervalue the significance of comprehending finance for your startup's survival. They prepare the income statement, balance sheet, and statement of cash flows using the accrual accounting method.

In doing so, Zack will help ensure that our clients’ financials are prepared in accordance with general accepted accountingprinciples (GAAP) and their 990s meet IRS guidelines. And he began his career in public accounting focusing on audits of local and national nonprofit and governmental organizations.

Because of their unique structure and operational model, nonprofits must comply with various accounting standards that are, in many ways, different from for-profit organizations. In the United States, these Generally Accepted AccountingPrinciples (or GAAP) are set by the Financial Accounting Standards Board (FASB).

Episode 243 Becoming a Treasurer Series, Part 24: Languages of Finance: FP&A As we jump back into the Becoming a Treasurer series, we are launching a new sub-series where we will look at the “language of finance.” What are some of the different ways we look at it in finance, accounting as a view of it?

The PCAOB and AICPA essentially interpret and enforce accounting rules as promulgated by the Financial Accounting Standards Board (FASB) , which is responsible for establishing and improving accounting standards for financial reporting in the United States.

GAAP , or generally accepted accountingprinciples, are rules and guidelines that organizations in the US must follow when preparing their financial statements. GAAP is designed to ensure that financial statements are accurate and consistent, making them easy for investors to compare.

Reporting functional expenses has been required by Generally Accepted AccountingPrinciples (GAAP) since 2017, as detailed in ASU 2016-14. At The Charity CFO , we work exclusively with nonprofit organizations to give them accurate books, timely reports, and expert advice on their nonprofit finances. To build public trust.

Bookkeepers, accountants, and Chief Financial Officers (CFOs) all serve critical roles in managing an organization’s finances. An accountant generally holds a bachelor’s degree in accounting or finance. Some nonprofit accountants are also Certified Public Accountants (CPA) , though it’s typically not required.

Without it, you won't know if you can make that capital investment or if you have the finances to hire to scale up production. A cash flow statement is an important tool that reveals how your business decisions affect cash and cash equivalents – and divides the analysis down into operating, investing, and financing activities.

Your business is creating a product or service; finance is not your business. Accountant: If your financial status doesn’t warrant hiring a CFO, you still need financial support; at the very least, you’ll need help with your day-to-day accounting and regulatory compliance. Courtesy of YEC.

Sure, your mission should be a priority, but managing finances can’t be neglected either. Without a good grasp of your finances, your nonprofit risks: Exposure to fraud. When creating your fiscal policy, ensure that it complies with the Generally Accepted AccountingPrinciples (GAAP). Bring GAAP compliance.

What will our finances look like?" Pro forma financial statements and GAAP It's important to note that, since pro forma statements are based on hypothetical or projected data, they are not compliant with generally accepted accountingprinciples—GAAP statements must be based on actual financial results.

In general, financial statement compliance involves adhering to established standards and regulations, such as Generally Accepted AccountingPrinciples (GAAP) and the Financial Accounting Standards Board (FASB) guidelines. When the finance team sees their leader prioritize compliance, they are more likely to follow suit.

Whether you are an educational, charitable, religious, sports, or other public-benefit organization, you need to have a good handle on your finances in order to make the most impact. Yes, they might have a board member or volunteer who takes care of the finances, but they often lack specific expertise in nonprofit accounting.

While many nonprofits start with cash-basis accounting due to its simplicity, this method often falls short of providing a comprehensive view of a nonprofit’s financial health. Transitioning to accrual-basis accounting can offer a more accurate representation of finances and enhance long-term planning. Get the free guide!

Accounting Standards In the United States, all organizations must adhere to the Generally Accepted AccountingPrinciples (GAAP). This establishes core accounting standards for nonprofits which help with accountability and transparency. Utilize your employees’ skill sets and expertise to your advantage.

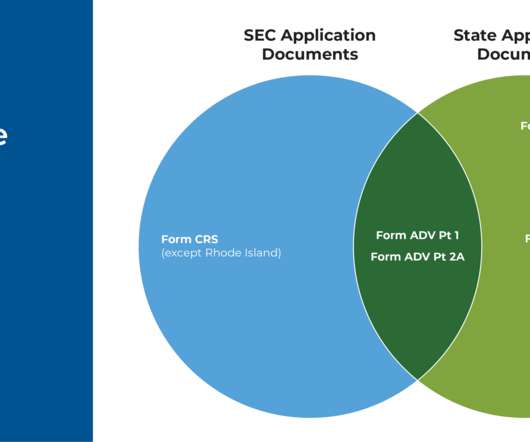

Along with renewing their registration annually (for both SEC- and state-registered firms), firms face a variety of requirements related to their internal finances, fees, marketing activities, and advisor agreements depending on whether they are SEC- or state-registered. RIA Fee Itemization And Surprise Custody Audits.

But in the accounting world, “financial consolidation” is a well-defined process that includes several complexities and accountingprinciples. Here are the key accounting consolidation steps in the finance consolidation process : Collecting trial balance data (e.g.,

In addition to accounting processes, the CFO leads prospective financial activities that are part of the vision: forecasting, budgeting, mergers, and investments. Both the CFO and controller are financial experts and can be relied upon to accurately report data and finances. The case for a CFO.

Besides the wasted time involved in chasing down and correcting incorrect revenue recognition, it creates issues with meeting the Generally Accepted AccountingPrinciples (GAAP) standard for financial reporting. If revenue is improperly recognized, it will report higher profits than actual.

This accountingprinciple offers an insightful perspective into a business's worth , underlining the importance of financial reporting in today's market dynamics. Understanding the Net Book Value (NBV) of a company's assets is critical for knowing its financial health and potential for future growth.

Generally Accepted AccountingPrinciples (GAAP) and International Financial Reporting Standards (IFRS)-compliant, so you can focus on what matters—telling your company’s financial story. “Now we have one set of data and one view of life,” says Mark Cohen, VP of finance at Thule.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content