This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The company’s CBAM obligations and purchased certificates have to be accounted for in accordance with global accountingstandards like the IFRS or US GAAP. With the Trump administration embracing digital assets, finance leaders need to get educated on the potential risk and reward of cryptocurrencies and stablecoins.

If your nonprofit uses donations of supplies, services, and even time to help fund your operations, you need to know about recent changes in accountingstandards for in kind donations. So now is the perfect time to make sure you report in kind gift donations in compliance with GAAPstandards in 2022. Get the free guide!

What does this mean to the finance and accounting team of 2022? Increasingly more Finance & Accounting (F&A) functions will adopt a hybrid work model in which CFOs provide the tools to finance staff to productively work from anywhere.

Accountingstandards for nonprofits are probably not the first thing you think about, but are crucial for your organization to succeed. Because of their unique structure and operational model, nonprofits must comply with various accountingstandards that are, in many ways, different from for-profit organizations.

AI coupled with The Digitization of the Finance Function create powerful levers for today’s CFO. AI in the “Real World” While these powerful tools seem to have a near mastery of natural language communication, they are not necessarily designed to possess many of the skills required by finance and accounting professionals.

Assessing Accounting For entities preparing GAAP compliant financial statements, adoption of Revenue Recognition Standard (ASC 606) and Lease AccountingStandard (ASC 842) is now mandatory. The post Strategic Finance Focus at Year-End appeared first on vcfo.

Finance organizations regularly face the challenges of meeting strict deadlines and satisfying data quality requirements for closing the books and delivering accurate financial statements. It enables finance teams to automate and accelerate the financial close with minimal IT support. DOWNLOAD NOW.

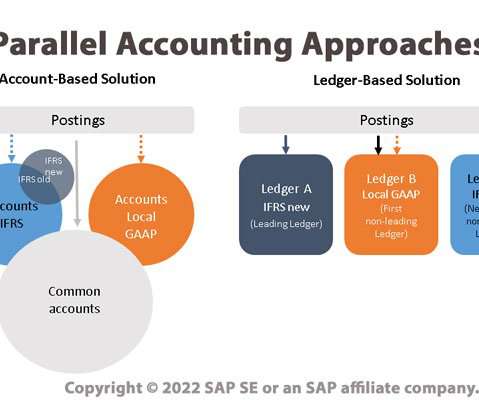

One important side effect of the ongoing trend toward globalization is the need to comply with a range of different accounting principles as well as with disparate reporting and compliance mandates. Parallel Ledgers - in which multiple ledgers are used, with an accounting principle applied to each ledger.

The PCAOB and AICPA essentially interpret and enforce accounting rules as promulgated by the Financial AccountingStandards Board (FASB) , which is responsible for establishing and improving accountingstandards for financial reporting in the United States. Why Should You Care?

If you’re looking for info on fund accounting in government here is a great resource for you. Both Generally Accepted Accounting Principles (GAAP) and Financial AccountingStandards Board (FASB) 116/117 require at least a minimum level of fund reporting, so you’ll need it in order to pass an audit.

In a survey conducted by the Institute of Management Accountants (IMA), and sponsored by Blackline, titled “Process Automation in Accounting and Finance,” examining the attitudes and concerns of 750 financial professionals surrounding accounting and month-end closing processes, manual activities remain prevalent — at the cost of time and money.

Top accountancy firms are asking the Financial AccountingStandards Board (FASB) to clarify how corporates should report on supplier finance programs that are in place, according to Compliance Week reports on Friday (Oct. As the letter notes, U.S.

Instead, accounting software prioritizes accuracy, standardization, and regulatory compliance. The Impact of GAAP on Integration Efforts We’ve mentioned GAAP several times, but why do these principles affect integration so much? For nonprofits, GAAP ensures transparency, accuracy, and consistency in financial statements.

AI coupled with The Digitization of the Finance Function create powerful levers for today’s CFO. AI in the “Real World” While these powerful tools seem to have a near mastery of natural language communication, they are not necessarily designed to possess many of the skills required by finance and accounting professionals.

In this new role, he will serve as one of our in-house experts on existing and emerging nonprofit accountingstandards and auditing best practices. In doing so, Zack will help ensure that our clients’ financials are prepared in accordance with general accepted accounting principles (GAAP) and their 990s meet IRS guidelines.

AccountingStandards In the United States, all organizations must adhere to the Generally Accepted Accounting Principles (GAAP). For nonprofits, however, there is an additional and specific set of standards that organizations must follow, as set out by the FASB 117. Reach out to us here for a free consultation.

Reporting functional expenses has been required by Generally Accepted Accounting Principles (GAAP) since 2017, as detailed in ASU 2016-14. Being clear, consistent, and accountable in your reporting of expenses is a big step toward earning their trust. . So you really don’t have a choice, but if you want more reasons….

As a small business owner or finance manager, it’s crucial to approach this process with a clear plan. This article includes small business accounting tips to prepare for an audit while minimizing its expenses and findings. An audit evaluates: Compliance with accountingstandards (GAAP or IFRS.)

has announced a spring 2016 update to its key financial management flagship offering in a push to streamline the workflow of finance professionals. GAAP and international accountingstandards, is another boon to efficiency, said Bres.

Whether you are an educational, charitable, religious, sports, or other public-benefit organization, you need to have a good handle on your finances in order to make the most impact. Yes, they might have a board member or volunteer who takes care of the finances, but they often lack specific expertise in nonprofit accounting.

In general, financial statement compliance involves adhering to established standards and regulations, such as Generally Accepted Accounting Principles (GAAP) and the Financial AccountingStandards Board (FASB) guidelines. This continuous improvement approach helps maintain high standards of financial reporting.

You have a primary responsibility to your donors, grantmakers, and other stakeholders to find ways to share these statements while still following the highest accountingstandards. It helps you comply with GAAPstandards and IRS regulations. This financial report contains three segments: 1. Get the free guide!

For accountants, this means the profit-generating strategies and investment ideas you bring to the table are still applicable and can make a massive impact. One key differentiator is that what is recorded following GAAP is what will show up on the audit and may not show up on the IRS tax form, Federal Form 990. Get the free guide!

Not having up to the minute transparency into your finances can be daunting. You may also choose to outsource certain aspects of your accounting that may require less immediate access. Properly evaluate each company and their credentials before letting go of your financial data. Get the free guide!

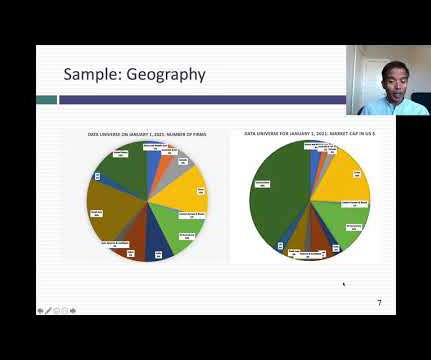

My motivation was to understand the responsibility of the CFO suite, the process of billing to accounting, and the software tools available to run an effective finance office. I interviewed 50 people that held CFO, finance manager, and financial analyst type roles. The following are select responses from the finance leaders.

This measure is a direct product of fair value reporting, a principle insisting that assets be reported at their market value, which forms the bedrock of financial reporting standards under US GAAP. Determining Eligibility for Depreciation To accurately apply depreciation, it is essential to first determine which assets are eligible.

One reason is that these businesses are not only not required to publicly disclose their financial details in most parts of the world, but often follow more malleable accountingstandards, making the data less reliable and comparable. Macro Data I do not report much macroeconomic data for two reasons.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content