Musings on Markets: Data Update 5 for 2022: The Bottom Line!

CFO News Room

JANUARY 18, 2023

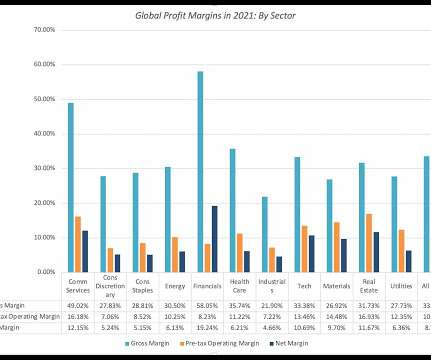

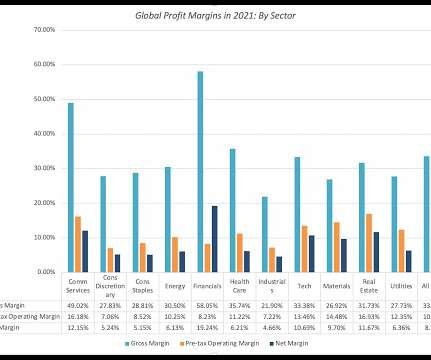

Even though we live in an age where user platforms and hyper revenue growth can drive company valuations, that adage remains true. IFRS and GAAP now treat as leases as debt, but that is still not the case in many other markets that are not covered by either standard). The numbers yield interesting insights. .

Let's personalize your content