This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The consolidation process typically includes aggregating financial results, eliminating intercompany transactions, handling currency conversions, and ensuring compliance with accountingstandards like the International Financial Reporting Standards (IFRS) or Generally Accepted AccountingPrinciplesGAAP.

If your nonprofit uses donations of supplies, services, and even time to help fund your operations, you need to know about recent changes in accountingstandards for in kind donations. So now is the perfect time to make sure you report in kind gift donations in compliance with GAAPstandards in 2022. Get the free guide!

Accountingstandards for nonprofits are probably not the first thing you think about, but are crucial for your organization to succeed. Because of their unique structure and operational model, nonprofits must comply with various accountingstandards that are, in many ways, different from for-profit organizations.

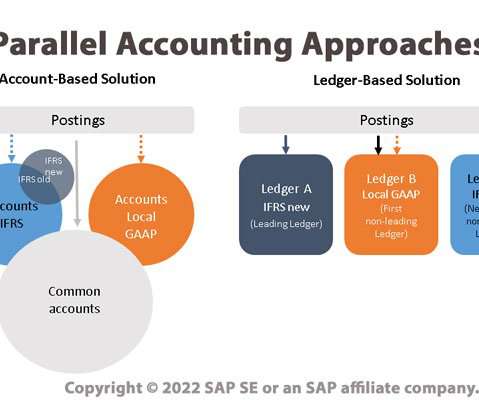

One important side effect of the ongoing trend toward globalization is the need to comply with a range of different accountingprinciples as well as with disparate reporting and compliance mandates. Parallel Ledgers - in which multiple ledgers are used, with an accountingprinciple applied to each ledger.

The PCAOB and AICPA essentially interpret and enforce accounting rules as promulgated by the Financial AccountingStandards Board (FASB) , which is responsible for establishing and improving accountingstandards for financial reporting in the United States. Why Should You Care?

Reports in The Block Crypto late last week said a group of California CPAs has sent a letter to the Financial AccountingStandards Board, a federal board that sets Generally Accepted AccountingPrinciples (GAAP), requesting that it consider establishing a task force to address a lack of clarity in cryptocurrency accountingstandards.

This makes it challenging to create technology that tracks data for fundraising purposes while still following accountingprinciples. Instead, accounting software prioritizes accuracy, standardization, and regulatory compliance. For nonprofits, GAAP ensures transparency, accuracy, and consistency in financial statements.

If you’re looking for info on fund accounting in government here is a great resource for you. Both Generally Accepted AccountingPrinciples (GAAP) and Financial AccountingStandards Board (FASB) 116/117 require at least a minimum level of fund reporting, so you’ll need it in order to pass an audit.

In this new role, he will serve as one of our in-house experts on existing and emerging nonprofit accountingstandards and auditing best practices. In doing so, Zack will help ensure that our clients’ financials are prepared in accordance with general accepted accountingprinciples (GAAP) and their 990s meet IRS guidelines.

Audited financial statements focus on compliance with GAAPaccountingstandards, whereas Quality of Earnings reports focus on the company’s earnings history and potential. Significant and/or unusual accounting policies such as: Changes in accounting methods. Changes in accountingprinciples.

In general, financial statement compliance involves adhering to established standards and regulations, such as Generally Accepted AccountingPrinciples (GAAP) and the Financial AccountingStandards Board (FASB) guidelines. What is Financial Statement Compliance?

AccountingStandards In the United States, all organizations must adhere to the Generally Accepted AccountingPrinciples (GAAP). For nonprofits, however, there is an additional and specific set of standards that organizations must follow, as set out by the FASB 117.

Reporting functional expenses has been required by Generally Accepted AccountingPrinciples (GAAP) since 2017, as detailed in ASU 2016-14. Being clear, consistent, and accountable in your reporting of expenses is a big step toward earning their trust. . So you really don’t have a choice, but if you want more reasons….

Many jurisdictions are moving towards international accountingstandards such as International Financial Reporting Standards (IFRS) and US Generally Accepted AccountingPrinciples (GAAP). However, APAC and EMEA take a much more localised approach.

Yes, they might have a board member or volunteer who takes care of the finances, but they often lack specific expertise in nonprofit accounting. As a result, the organization might not adhere to Generally Accepted AccountingPrinciples (GAAP), which can trip them up come tax time or during an audit.

When choosing the best financial reporting software solution, it's important to consider factors such as ease of use, scalability, integration with existing systems, compliance with accountingstandards, cost, customer support, and any unique requirements your organization might have.

This accountingprinciple offers an insightful perspective into a business's worth , underlining the importance of financial reporting in today's market dynamics. Understanding the Net Book Value (NBV) of a company's assets is critical for knowing its financial health and potential for future growth.

The company’s CBAM obligations and purchased certificates have to be accounted for in accordance with global accountingstandards like the IFRS or US GAAP. CBAM compliance also requires the purchase, management, and surrender of CBAM certificates.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content