This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As the risk-free rate rises, expected returns on equities will be pushed up, and holding all else constant, stock prices will go down., and the reverse will occur, when risk-free rates drop. That is why the risk-free rate becomes an input into option pricing and forward pricing models , and its absence leaves a vacuum.

During the course of the year, investors also rediscovered that the essence of business is not growing revenues or adding users, but making profits from that growth. In this post, I will focus on trend lines in profitability at companies in 2022, with the intent of addressing multiple questions.

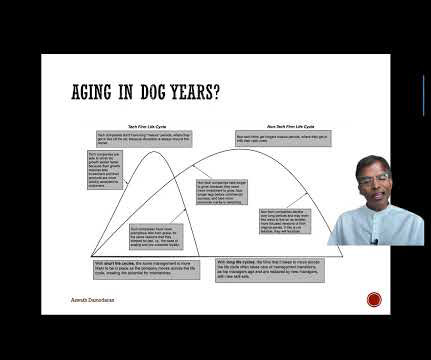

Not surprisingly, the operating metrics change as companies age, with high revenue growth accompanied by big losses (from work-in-progress business models) and large reinvestment needs (to delivery future growth) in early-stage companies to large profits and free cash flows in the mature phase to stresses on growth and margins in decline.

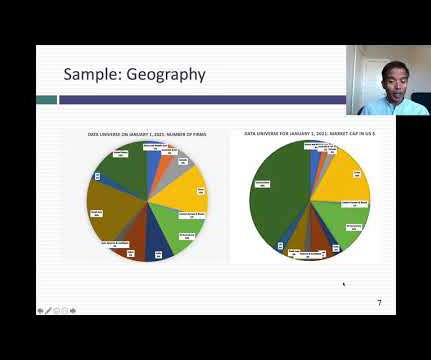

That said, it does mean that any broad conclusions (about profitability and revenues) that emerge from my data apply to public companies, and it may be dangerous to extrapolate to private businesses, especially in a year like 2020 where private businesses could have been affected more adversely by COVID shutdowns than public companies.

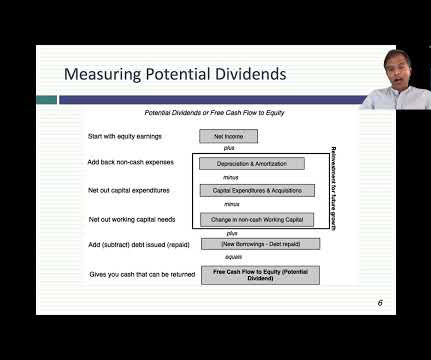

In the second, Warren Buffet used some heated language to describe those who opposed buybacks, calling them “economic illiterates” and “silver tongued demagogues “. As growth moderates and profitability improves, free cash flows to equity will turn positive, giving these firms the capacity to return cash.

There’s very few, I would argue probably no consistent predictors of, of any sort of economic or market cyclicality. So you’ve got, you’ve got a modeling hurdlerate that you need to figure out when you’re adding diversifiers. I think ity economics would argue you have to protect your capital to survive.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content