This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

I spend most of my time in the far less rarefied air of corporate finance and valuation, where businesses try to decide what projects to invest in, and investors attempt to estimate business value. A key tool in both endeavors is a hurdlerate a rate of return that you determine as your required return for business and investment decisions.

I know that this classification is at odds with the industry classifications based upon SIC or NAICS codes, but it works well enough for me, at least in the context of corporate finance and valuation. Since I teach corporate finance and valuation, I find it useful to break down the data that I report based upon these groupings.

After the rating downgrade, my mailbox was inundated with questions of what this action meant for investing, in general, and for corporate finance and valuation practice, in particular, and this post is my attempt to answer them all with one post. and the reverse will occur, when risk-free rates drop.

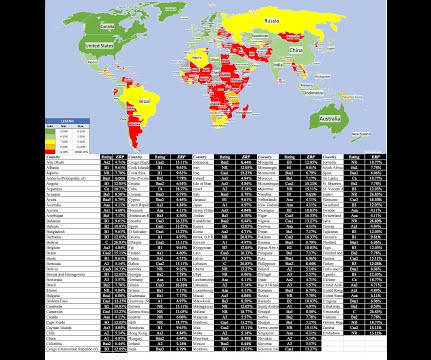

Put simply they look at a long time period in the past (50 years or even 100 years) and look at the premium that stocks earned over a risk free investment (treasury bills or bonds); that historical risk premium then gets used as a measure of the current equity risk premium. Data Update 4 for 2021: The HurdleRate Question.

To illustrate, consider a practice in valuation, where analysts are trained to add a small cap premium to discount rates for smaller companies, on the intuition that they are riskier than larger companies. It is very likely that these rules of thumb were developed from data and observation, but at a different point in time.

Company HurdleRates This post has already become much longer than I intended it to be, but I want to end by bringing these equity risk premiums down to the company level, and examining how they play out in hurdlerates, to be used in investment analysis by companies and valuation by investors.

CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. CHANCELLOR: And look — yeah, but then if you look at the valuation of the market at that time, the market was — the U.S. They’re actually just buying long dollars, treasuries.

” look at the Monte Carlo simulations, look at what is the hurdlerate. So, last year, valuations were high, interest rates were low. And I said, “Look, you’ve got to look at where we are with valuations, and you have to look at where the 10-year Treasury is at. Is it at 1.5%?”

Country Risk in Business Most corporate finance classes and textbooks leave students with the proposition that the right hurdlerate to use in assessing business investments is the cost of capital, but create a host of confusion about what exactly that cost of capital measures.

00:21:21 [Speaker Changed] So this story came out that, oh, value is defensive because it has this valuation buffer to it 00:21:28 [Speaker Changed] In that one example. So you’ve got, you’ve got a modeling hurdlerate that you need to figure out when you’re adding diversifiers. The second is behavioral.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content