This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For example, while South African companies follow International FinancialReporting Standards (IFRS), the US requires compliance with its Generally Accepted AccountingPrinciples (GAAP). IFRS is principles-based and allows for some judgment in financialreporting, while GAAP is more rigid, rules-based, and less forgiving.

Members’ Profile: Rofhiwa Irene Singo In this edition of our CFO Spotlight series, we are featuring Rofhiwa Irene Singo, an accomplished finance leader whose journey is a testament to resilience, adaptability, and impactful leadership. What key skills should a newly qualified accountant develop on their path to becoming a CFO?

How a CFO Ensures Compliance in FinancialReporting Reliable financial statements are crucial for business management, but ensuring compliance may feel like a luxury in the resource-constrained world of small business. Read on to learn how CFOs perform this evaluation and what compliance looks like in small businesses.

What is a Chief Financial Officer (CFO)? A Chief Financial Officer (CFO) is a senior executive in charge of the strategic direction and goal setting of a nonprofit’s accounting and financial management. Responsibilities typically include advanced analysis and reporting, budgeting, etc.

When choosing the best financialreporting software solution, it's important to consider factors such as ease of use, scalability, integration with existing systems, compliance with accounting standards, cost, customer support, and any unique requirements your organization might have. What is financialreporting software?

Big companies used to hog all the CFO action, but now even small and medium-sized businesses are jumping on the bandwagon. Why the sudden CFO craze? Well, CEOs are cluing in on the fact that having a financial expert on board can steer their ship in the right direction and spur business growth. As the Director of Amyris Inc.,

The #1 accounting mistake that nonprofits make is hiring the wrong people to help them. Get this FREE guide to discover what you need to do to ensure you hire the right accountant, bookkeeper, or CFO the FIRST time. Assurance is an opinion given by a CPA on the accuracy of an organization’s financial statements.

The difference between cost of goods sold and ordinary business expenses is well defined in Generally Accepted AccountingPrinciples (GAAP) but routinely ignored by small business bookkeeping services. Depreciation and amortization reported for tax purposes in excess of that reported in financialreports.

For many, the mistakes were discovered when corporate finance teams were changing accounting paperwork to comply with the new U.S. tax law and revenue accounting rules. Camping World Holdings, for example, had to file a restatement after it incorrectly recorded a deferred tax asset related to its acquisition of a 41.7

The changes to in kind donation reporting are specifically for organizations that follow generally accepted accountingprinciples (GAAP) in preparing their financial statements. And the second will impact the information you include in your disclosures (footnotes) to your financialreports.

And then, there are a series of reports and financial statements you’ll use to communicate the financial reality of your organization to potential donors, the IRS, watchdog agencies, and other stakeholders. The basic accountingprinciples for nonprofit organizations are the same as accounting for for-profit companies. .

It enables finance teams to automate and accelerate the financial close with minimal IT support. It also helps finance teams deliver financial results, create informative financial and management reports, and provide the chief financial officer (CFO) with an enterprise view of key financial ratios and metrics.

To comply with Generally Accepted AccountingPrinciples (GAAP), you must separate your revenue into at least 2 categories: Restricted Revenue shows funds with donor-placed restrictions on how or when you can spend the money. At The Charity CFO, we help 150+ nonprofits get audit-ready financialreports monthly, like clockwork.

A financial statement audit is a thorough review of your financial statements to determine if your financial statements present fairly, in all material respects, in accordance with generally accepted accountingprinciples. The purpose of a financial statement audit is NOT to detect fraud. Get the free guide!

In connection with this, the Association of Chartered Certified Accountants is urging businesses to take steps to maximise the opportunities of AI and lay foundations for responsible use of new technologies. Technology has long been a game-changer for accounting.

Nonprofit bookkeeping is the process of entering, classifying, and organizing financial data for the purpose of creating accurate financial records for your organization. Bookkeepers lay the foundation for the accounting processes that will follow. At The Charity CFO, we handle the books and all of your accounting needs.

This makes it challenging to create technology that tracks data for fundraising purposes while still following accountingprinciples. This makes it difficult to maintain the integrity of both donor and financial records when attempting to sync the two systems. Need some help interpreting your financial data?

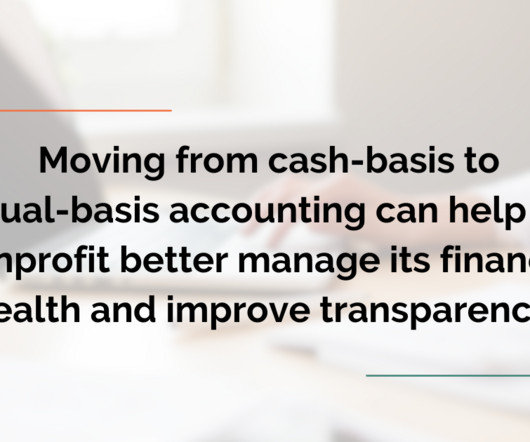

Cash accounting does not comply with Generally Accepted AccountingPrinciples (GAAP) for nonprofit organizations. So if you expect to grow or search for new sources of funding, you’ll probably need to graduate to accrual-basis accounting. The post Do Nonprofits Use Cash or Accrual Accounting? Get the free guide!

All these sources must be carefully managed to ensure compliance with Generally Accepted AccountingPrinciples (GAAP) and guidelines. Revenue recognition is an accounting process of properly identifying when income has been earned. Your organization’s accounting method really impacts the timing of recognizing transactions.

If you’re looking for info on fund accounting in government here is a great resource for you. Both Generally Accepted AccountingPrinciples (GAAP) and FinancialAccounting Standards Board (FASB) 116/117 require at least a minimum level of fund reporting, so you’ll need it in order to pass an audit.

For that reason, your account numbering, category names, and structure should follow standard guidelines and numbering conventions established by Generally Accepted AccountingPrinciples (GAAP). . For example, you don’t need separate accounts for different types of office supplies (pens, paper, markers).

In the United States, these Generally Accepted AccountingPrinciples (or GAAP) are set by the FinancialAccounting Standards Board (FASB). NPOs must adhere to these accounting policies to remain compliant with the law and maintain their tax-exempt status.

What could go wrong if your Chief Financial Officer (CFO) is not effective in their job? They could steer your company towards poor financial decisions, like risky investments, inaccurate budgeting, or insufficient cost control. What CFOs are Capable of Doing?

Improved Financial Transparency Accrual accounting provides stakeholders with a detailed view of your organization’s financial activities, improving trust and confidence. Transparent financialreporting can also improve donor relations. Many regulatory bodies and grantors require accrual-basis financial statements.

For example, “salary” is a straightforward line-item on a for-profit financialreport. . To complete your IRS 990, you’ll need to report your expenses based on how they fall within 3 categories, they are: . The #1 accounting mistake that nonprofits make is hiring the wrong people to help them.

This is why at The Charity CFO , we strive to provide relevant resources and support to ensure that your organization runs smoothly and efficiently. This week, we’ve rounded up 7 keys to nonprofit financial management. This establishes core accounting standards for nonprofits which help with accountability and transparency.

Yes, they might have a board member or volunteer who takes care of the finances, but they often lack specific expertise in nonprofit accounting. As a result, the organization might not adhere to Generally Accepted AccountingPrinciples (GAAP), which can trip them up come tax time or during an audit. Provide personalized service.

Proper revenue recognition is a core accountingprinciple that ensures proper financialreporting, ensuring that you remain compliant and maintain donor confidence. This complete visibility of financial information at all times is necessary to maintain a strong cash inflow and help make informed economic decisions.

But in the accounting world, “financial consolidation” is a well-defined process that includes several complexities and accountingprinciples. Here are the key accounting consolidation steps in the finance consolidation process : Collecting trial balance data (e.g.,

Maintaining healthy financial management is critical for the organization’s sustainability, stability, and flexibility, now and in the future. Poor financialreporting. They provide a framework for the oversight and governance of financial operations and activities. Collaboration issues. A Nonprofit Budget.

The Pros of AI in Bookkeeping The strong computational and comparative power of AI provides three distinct advantages: Efficiency: AI dramatically speeds up data processing, enabling faster financialreporting and analysis, crucial for timely business decisions.

For example, 70% of jurisdictions in South America mandate electronic transaction reporting, yet this is only the case for two jurisdictions in APAC (15%) – India and South Korea.

This is why most advisers do not collect more than $1,200 in fees per client, 6 months or more in advance, so as to avoid the requirement to prepare and publicly report their balance sheet.

Skip to main content Dont miss tomorrows CFO industry news Let CFO Dives free newsletter keep you informed, straight from your inbox. Most importantly, CBAM puts a price on carbon, making it a clear part of the CFO’s mandate. To manage this new financial liability, there are six steps that every CFO should take to prepare.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content