This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For example, while South African companies follow International FinancialReporting Standards (IFRS), the US requires compliance with its Generally Accepted AccountingPrinciples (GAAP). Balancing Different Standards Let’s start with the most obvious challenge: reconciling IFRS and GAAP.

The consolidation process typically includes aggregating financial results, eliminating intercompany transactions, handling currency conversions, and ensuring compliance with accounting standards like the International FinancialReporting Standards (IFRS) or Generally Accepted AccountingPrinciplesGAAP.

How a CFO Ensures Compliance in FinancialReporting Reliable financial statements are crucial for business management, but ensuring compliance may feel like a luxury in the resource-constrained world of small business. What is Financial Statement Compliance? Contact us today for more information.

The difference between cost of goods sold and ordinary business expenses is well defined in Generally Accepted AccountingPrinciples (GAAP) but routinely ignored by small business bookkeeping services. Even worse, an IRS income tax return does not follow the same rules as GAAP. Interest expense. R&D expenses.

When you pass the audit, you’ll receive a clean bill of health from your auditor and a professional opinion stating the accuracy and validity of your accounting records. It assures outside observers that “the organization’s financial records meet generally accepted accountingprinciples.”

But the deadline for making the changes has passed, and the FINAL deadline (for interim reporting periods) is coming up next month. So now is the perfect time to make sure you report in kind gift donations in compliance with GAAP standards in 2022. When do the changes to in kind gift reporting go into effect?

This makes it challenging to create technology that tracks data for fundraising purposes while still following accountingprinciples. This makes it difficult to maintain the integrity of both donor and financial records when attempting to sync the two systems. The short answer: these two datasets serve different purposes.

And then, there are a series of reports and financial statements you’ll use to communicate the financial reality of your organization to potential donors, the IRS, watchdog agencies, and other stakeholders. The basic accountingprinciples for nonprofit organizations are the same as accounting for for-profit companies. .

All these sources must be carefully managed to ensure compliance with Generally Accepted AccountingPrinciples (GAAP) and guidelines. Revenue recognition is an accounting process of properly identifying when income has been earned. It’s important to recognize revenue when it’s earned and not before or after.

Click on the link to download to discover in detail a list of the benefits that IBM Cognos Controller provide for finance teams: Data collection and validation Reconciliations Workflow and tasks to improve the close cycle Currency conversion Minority interest calculations Inter-company eliminations Group closing adjustments Management adjustments Allocations (..)

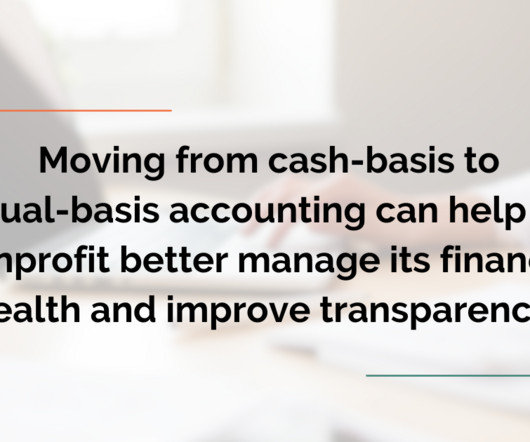

Cash accounting does not comply with Generally Accepted AccountingPrinciples (GAAP) for nonprofit organizations. So if you expect to grow or search for new sources of funding, you’ll probably need to graduate to accrual-basis accounting. Is Accrual Accounting a Requirement For You?

When choosing the best financialreporting software solution, it's important to consider factors such as ease of use, scalability, integration with existing systems, compliance with accounting standards, cost, customer support, and any unique requirements your organization might have. What is financialreporting software?

If you’re looking for info on fund accounting in government here is a great resource for you. Both Generally Accepted AccountingPrinciples (GAAP) and FinancialAccounting Standards Board (FASB) 116/117 require at least a minimum level of fund reporting, so you’ll need it in order to pass an audit.

In an ideal world, financialreports should build shareholder trust by offering accurate data about the performance of the company. In reality, a company’s financialreport can be more flimsy—involving estimates and judgment from leadership that’s far from the truth. at its peak to $0.26

Overview of the PCAOB and AICPA The Public Company Accounting Oversight Board (PCAOB) is a regulatory body established by the Sarbanes-Oxley Act of 2002 in response to corporate accounting scandals like Enron and WorldCom. Why Should You Care?

In the United States, these Generally Accepted AccountingPrinciples (or GAAP) are set by the FinancialAccounting Standards Board (FASB). NPOs must adhere to these accounting policies to remain compliant with the law and maintain their tax-exempt status. 117 (FASB 117). Get the free guide!

Reports in The Block Crypto late last week said a group of California CPAs has sent a letter to the FinancialAccounting Standards Board, a federal board that sets Generally Accepted AccountingPrinciples (GAAP), requesting that it consider establishing a task force to address a lack of clarity in cryptocurrency accounting standards.

For that reason, your account numbering, category names, and structure should follow standard guidelines and numbering conventions established by Generally Accepted AccountingPrinciples (GAAP). . For example, you don’t need separate accounts for different types of office supplies (pens, paper, markers).

To comply with Generally Accepted AccountingPrinciples (GAAP), you must separate your revenue into at least 2 categories: Restricted Revenue shows funds with donor-placed restrictions on how or when you can spend the money. At The Charity CFO, we help 150+ nonprofits get audit-ready financialreports monthly, like clockwork.

They also pitch in on major financial moves like mergers and fundraising. They double-check financialreports for accuracy and offer advice to the company leaders and the board. The CFO plays a key role in ensuring these statements are accurate and in line with standard accountingprinciples (GAAP).

Nonprofit bookkeeping is the process of entering, classifying, and organizing financial data for the purpose of creating accurate financial records for your organization. Bookkeepers lay the foundation for the accounting processes that will follow. And it’s impossible to do that without accurate bookkeeping.

Learn more about our nonprofit financial services by contacting us today ! Do You Struggle to Make Sense of Your Financial Statements? Get our FREE GUIDE to nonprofit financialreports, featuring illustrations, annotations, and insights to help you better understand your organization's finances. Get the free guide!

Improved Financial Transparency Accrual accounting provides stakeholders with a detailed view of your organization’s financial activities, improving trust and confidence. Transparent financialreporting can also improve donor relations. Many regulatory bodies and grantors require accrual-basis financial statements.

Maintaining healthy financial management is critical for the organization’s sustainability, stability, and flexibility, now and in the future. Poor financialreporting. They provide a framework for the oversight and governance of financial operations and activities. Ease the tax reporting. Interdependence.

Yes, they might have a board member or volunteer who takes care of the finances, but they often lack specific expertise in nonprofit accounting. As a result, the organization might not adhere to Generally Accepted AccountingPrinciples (GAAP), which can trip them up come tax time or during an audit.

For example, “salary” is a straightforward line-item on a for-profit financialreport. . To complete your IRS 990, you’ll need to report your expenses based on how they fall within 3 categories, they are: . That means you’ll need to present a Functional Expense Report to pass an audit. To build public trust.

Pro forma financial statements and GAAP It's important to note that, since pro forma statements are based on hypothetical or projected data, they are not compliant with generally accepted accountingprinciples—GAAP statements must be based on actual financial results.

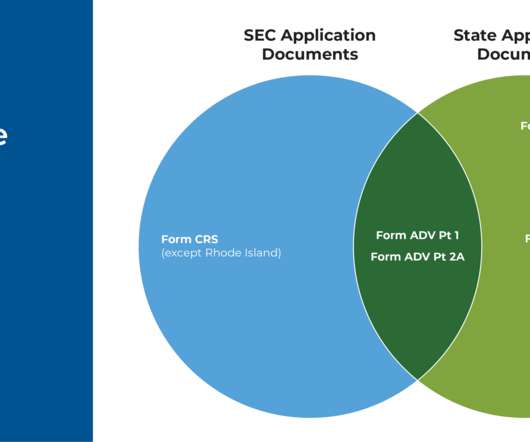

This is why most advisers do not collect more than $1,200 in fees per client, 6 months or more in advance, so as to avoid the requirement to prepare and publicly report their balance sheet. It should also be noted that, at least for state-registered advisers, financial statements must typically be prepared in accordance with GAAP.

But in the accounting world, “financial consolidation” is a well-defined process that includes several complexities and accountingprinciples. Here are the key accounting consolidation steps in the finance consolidation process : Collecting trial balance data (e.g.,

For example, 70% of jurisdictions in South America mandate electronic transaction reporting, yet this is only the case for two jurisdictions in APAC (15%) – India and South Korea. Across these regions, local GAAP is more common than international standards, required in 71% and 44% of jurisdictions respectively.

Accounting Standards In the United States, all organizations must adhere to the Generally Accepted AccountingPrinciples (GAAP). This establishes core accounting standards for nonprofits which help with accountability and transparency. Do You Struggle to Make Sense of Your Financial Statements?

If a company fails to accurately record its unearned revenue, it could lead to inaccurate financialreporting and create potential legal issues. If revenue is improperly recognized, it will report higher profits than actual. If an issue arises with unearned revenue, it’s important to research and rectify the reports.

Understanding the Net Book Value (NBV) of a company's assets is critical for knowing its financial health and potential for future growth. This accountingprinciple offers an insightful perspective into a business's worth , underlining the importance of financialreporting in today's market dynamics.

And that difference can vary when we think about cash if we’re formally trained in accounting, we think that the generally accepted accountingprinciple of cash is the way to go. Because there’s certain principles that govern accounting. What are we referring to when we say cash?

Almost in parallel, accounting as a profession found its footing and worked on creating rules that would apply to reporting, at least at publicly traded companies, with GAAP (Generally Accepted AccountingPrinciples) making its appearance in 1933.

Ensure auditable reporting and compliance The CFO needs to work with other functions like corporate financialreporting, regulatory compliance, tax, treasury, and legal to ensure timely, auditable reporting and financialaccounting. You can unsubscribe at anytime. Registered in England and Wales.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content