This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

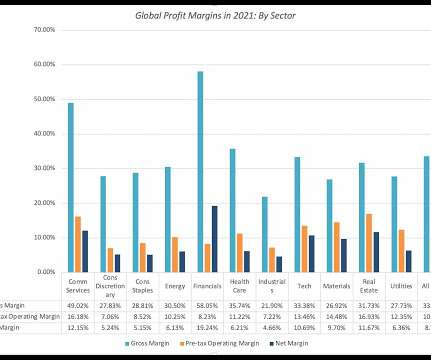

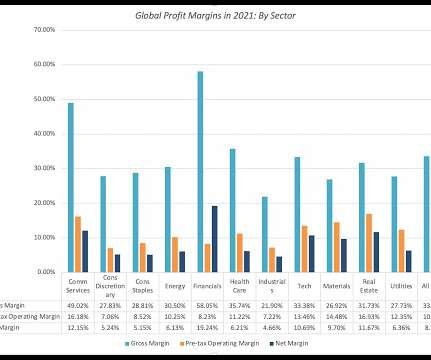

In this post, I will focus on how companies around the world, and in different sectors, performed on their end game of delivering profits, by first focusing on profitability differences across businesses, then converting profitability into returns, and comparing these returns to the hurdlerates that I talked about in my last data update post.

Societe Generale also offers a dedicated and simplified solution to retail clients or small and midsize enterprises (SMEs) based on their ESG rating. Finally, establishing connectivity to CRX Markets improves support for Societe Generales largest clients to help grow the banks SCF programs.

What is a hurdlerate for a business? There are multiple definitions that you will see offered, from it being the cost of raising capital for that business to an opportunity cost , i.e., a return that you can make investing elsewhere, to a required return for investors in that business. What is a hurdlerate?

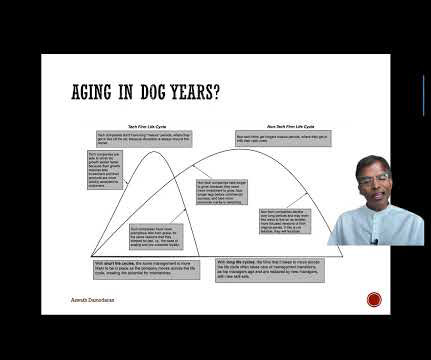

In fact, the business life cycle has become an integral part of the corporate finance, valuation and investing classes that I teach, and in many of the posts that I have written on this blog. Tech companies age in dog years, and the consequences for how we manage, value and invest in them are profound.

In my last three posts, I looked at the macro (equity risk premiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdlerates for businesses, in the form of costs of equity and capital.

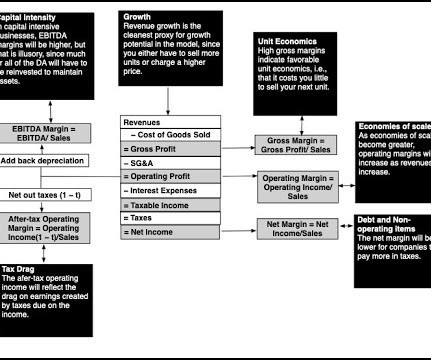

Income from financial holdings (including cash balances, investments in financial securities and minority holdings in other businesses) are added back, and interest expenses on debt are subtracted out to get to taxable income. Returns on Invested Capital (or Equity).

Income from financial holdings (including cash balances, investments in financial securities and minority holdings in other businesses) are added back, and interest expenses on debt are subtracted out to get to taxable income.

In January 1993, I was valuing a retail company, and I found myself wondering what a reasonable margin was for a firm operating in the retail business. In pursuit of an answer to that question, I used company-specific data from Value Line, one of the earliest entrants into the investment data business, to compute an industry average.

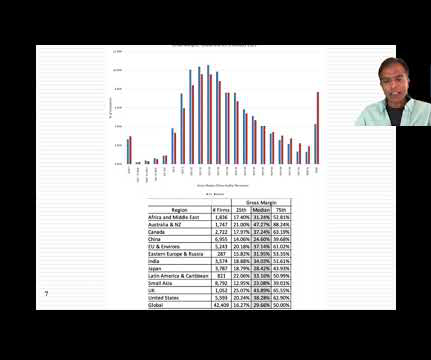

Some of that variation can be attributed to different mixes of businesses in different regions, since unit economics will result in higher gross margins for technology companies and commodity companies, in years when commodity prices are high, and lower gross margins for heavy manufacturing and retail businesses.

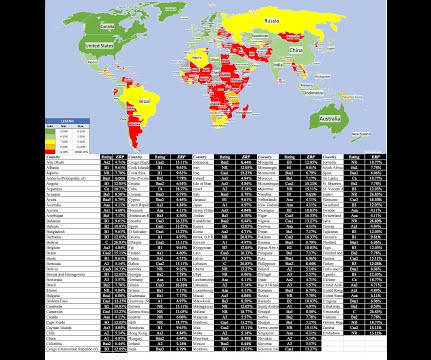

Country Risk: Determinants At the risk of stating the obvious, investing and operating in some countries is much riskier than investing and operating in others, with variations in risk on multiple dimensions. Political Structure Would you rather invest/operate in a democracy than in an autocracy?

You work at Capital Growth Financial and in former global markets before you join investing Giant Merrill Lynch in 2007, what was that transition like from smaller shops to a really, really big one? So it’s gonna take a little more confidence, you know, and equities to, because you get your, your hurdlerates higher, you know?

I, if you are at all interested in concepts of things like portable alpha or return stacking, or just want to know how a quant looks at the world of investing and tries to decide where there are opportunities. Quantitative investing was, was that the plan from the beginning? Let’s talk a little bit about your background.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content