This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A number of well-followed ESG-themed stock indices have been outperforming their conventional benchmarks since 2022, presenting potentially attractive investment opportunities in Southeast Asia.

Owner’s opinions of their business value can be influenced by inherent biases, flawed valuation methodologies, and factors lurking beyond their control. Owners often seek valuations from CPAs or similar entities for purposes such as insurance, estate planning, or internal events.

The reporters did not suggest wrongdoing, but allow me to point out that any advisor, let alone two, who became billionaires while wildly underperforming their benchmarks are obviously not fiduciaries. My advice was not based on fear of a bubble or the (over)valuation of Yahoo; rather, I suggested employing a regret minimization framework.2

This is more than overconfidence, the DKE is how poorly we are at metacognition assessing our own abilities at a specific task Look at the history of performance and the small number of professional investors who outperform their benchmarks over 1, 5, 10, and 20 years. How should they be reacting to the economic volatility?

Now, we know from the academic literature that three years before the fraud, they tend to beat earnings benchmarks. Their initial response was to increase their human intervention in 2008: They changed their inventory valuation assumption, their revenue recognition assumptions, and a few other things. Horton: Heres one.

But did you know that business valuation can give you more insight into your business than just the economic value? Keep reading to learn more about why business valuation is such an important process for every business. Business valuation is the best way to get proof of how well your business is doing year to year.

Valuations of Hong Kong-listed stocks are now quite reasonable, Mr. Ru said, adding that he doesn’t expect China’s internet sector to be hit with major regulatory changes this year. . In the bond market, the benchmark 10-year U.S. Treasury yield declined to 1.903%, according to Tradeweb.

In today’s competitive and high-cost market, sponsors rely on margin expansion to drive higher valuations and prepare portfolio companies for exit. They optimize shared services, launch digital transformation efforts across portfolio companies, and enhance unit economics through data-driven pricing and supply chain adjustments.

Ultimately, lack of financial know-how can leave you unprepared for shifting economic conditions that could undermine revenue and growth. EBITDA measures operational earnings (not capital investments), and it is often a better profitability benchmark than net income.

His approach involves working backward from desired outcomes, such as an EBITDA goal or exit valuation, and breaking these down into actionable steps and KPIs. For instance, if the goal is to grow and exit, we work backward from the desired valuation. What EBITDA profitability does the company need at the expected valuation multiple?

The current economic climate is causing profound challenges for business owners across industries. Three: Benchmark Industry Profitability Ratios Your profit margin might look weak to you, but is it? Benchmark your industry before looking at your profitability so you know what to aim for. But how much are they really worth?

In this episode, we talk in-depth about how, in 2022, Eric and his wife Kali faced a tumultuous year the firm dipped from $600,000 to $500,000 of revenue run rate in just the first few months and because it coincided with the arrival of their first child they didn’t have the bandwidth and capacity to adapt, how, to help with capacity constraints, (..)

You get a bachelor’s in economics from Colgate and then an MBA in finance from NYU Stern. I was an economics and English major. We learned everything, you know, across from accounting to auditing to, to tax and valuation. It seemed like the perfect match of asset and liabilities until real estate valuations bottomed out.

The current economic climate is causing profound challenges for business owners across industries. Three: Benchmark Industry Profitability Ratios Your profit margin might look weak to you, but is it? Benchmark your industry before looking at your profitability so you know what to aim for. But how much are they really worth?

For example, you can see what’s the biggest drawdown, how long did it last, how long and how often did a strategy beat its benchmark, and by what magnitude. Barry Ritholtz : So let’s break that into two halves, starting with valuation. Explain why P/E isn’t the best way to measure valuation.

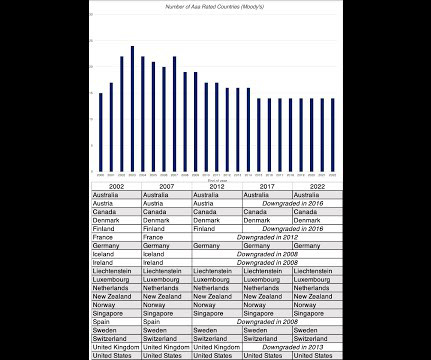

After the rating downgrade, my mailbox was inundated with questions of what this action meant for investing, in general, and for corporate finance and valuation practice, in particular, and this post is my attempt to answer them all with one post.

When focusing on growth ambitions, organizations must consider the variables that affect hiring and deploying a high-performing workforce, including economic uncertainty, talent shortages, and hybridized workplaces. That agility and flexibility is important as markets go from bullish to bearish, resulting in falling valuations.

RITHOLTZ: And last question about the various teams, does everybody have a different benchmark? How do you contextualize the economic data and the broad stamp recession when you’re thinking about managing risk? How does this impact global trade and other economic factors? How do you track performance? TROPIN: Yeah.

A bachelor’s in economics from Northwestern and then an MBA from University of Chicago. And so I kind of leveraged that when I went to Morningstar because they’re very focused on quality, the whole concept of economic moats, but also about buying companies when they’re trading at a discount to intrinsic value.

But what he’s found to be the most interesting in talking to who’s on the ground, is the differences in how people voted based on their age or economic status. In the very near future these companies may see the valuation of their businesses diminish, capital requirements change and even more investors looking to invest in the E.U.

Its index and its benchmark. There’s also quantitative metrics that we look at Those have evolved, but always within that capa, that cluster of high returns on investment stability across the economic cycle are consistent and strong balance sheets. a year, way over both. It’s in the top 1% of its peers. In 2000, right.

The scale of the proposed transaction, and therefore the quantum of its economics, is wholly different from those we’ve already signed,” the executive said, noting that Kroger was in the best position to be successful in the U.S. In the middle of it all, the company is looking to raise $10 billion with an implied valuation of $160 million.

SEIDES: If the S&P is your benchmark, which it isn’t for these pools of capital. RITHOLTZ: What should be their benchmark? So the proper benchmark for those pools has to look a little bit like the underlying assets they’re investing in. So what do you use for a benchmark? 14, 15% a year? RITHOLTZ: Right.

You know, I think of like a Mike Spies or at Sutter Hill, you know, a Martine Cado and Andreessen, you know, Gurley when he was at Benchmark. It was about $170 million valuation. It’s 00:52:47 [Speaker Changed] A tough benchmark to beat. There are world class partners of ours in Silicon Valley. We are all analysts.

But when you look at emerging markets and when you look at value, the opportunity for alpha is much, much greater than it is in traditional large cap growth stocks in the US And a lot of managers in that space actually beat their benchmark. So I decided to become an economics major and a psychology minor. Christine Philpots.

The best example I always love to give is that Amazon’s last private round was at a $60 million post money valuation. Post money valuations until the market has changed dramatically. 00:15:29 [Speaker Changed] That’s your benchmark, correct? So, so let’s talk a little bit about valuation.

Issue: Capital Allocation and Cash Flow Resilience Ask Yourself: Is our liquidity strategy agile enough to withstand economic shocks? In times of economic uncertainty, CFOs must scrutinize capital project commitments and cash flow strategies to protect the business from unfavorable conditions.

So a variety of risk meetings, a variety of economic meetings. They create the benchmark. So when there’s a major turnover like that that happens, you always have the option, “Hey, can you do it exactly on the time that it enters the benchmark? So, our active team has been successful outperforming their benchmarks.

To help determine an appropriate fee, advisors can then look to various benchmarking studies , which can provide industry-wide fee data , as well as information on specific fee structures and geographic areas that can help a firm owner tailor their fee. sequence of return risk ). Gregg Greenberg| InvestmentNews).

So I leave the Bureau of Labor Statistics and I move into economic consulting. And how do we think about them from a valuation perspective? NORTON: Concentrated portfolios or willing to stick our necks out and look different than a benchmark. That’s very funny. NORTON: Right. And so you can think of that.

And the advice that he gave to David Einhorn about it that helped lead Einhorn to start really kicking the benchmark’s butt again for the past couple of years. We built a company that was focused on valuation, initially, actually targeting corporate strategic planning departments. It pushes valuations higher over time.

economics, correct. RITHOLTZ: Oh, not the control, just the economics. capital problem helps improve our economic sharing …. CONROD: I — I think the — in this low interest rate environment people are looking for yield and income, and how do they — they have a — they have a benchmark. Is that right? CONROD: Yeah.

The fact that you’ve got declining risk appetite, declines are prolonged, deep and valuations mean revert. The second, and what’s interesting about that period, is the fact that valuations actually peaked in 1961. MIAN: Valuations are ebb and flow. RITHOLTZ: So let’s take a couple of examples.

And they also have a unique approach to feeds when they’re generating alpha, when they’re outperforming their benchmark, they take a performance fee. A degree in mathematics from Oxford, a doctorate in mathematical epidemiology and economics from Cambridge. What made you add economics to your, to your graduate degree?

He has absolutely crushed his benchmark over that period. He’s crushed the Russell 2000, whatever benchmark you want to talk about. You’re 34th, you’re retiring after 34 years and you trounce what’s really the more appropriate benchmark, I would assume the Russell 2000. a year since 1989. Much better.

Psychologically, it’s a benchmark of economic health, even if it is divorced from reality. And because it hasn’t thrown corporate valuations into the ditch, hopefully, companies have been able to bring back furloughed workers. That’s not to say the stock market isn’t important.

The valuation of risk versus 00:46:33 [Speaker Changed] Reward 00:46:34 [Speaker Changed] Is something that I think a machine cannot do in the same way that human can. 00:47:06 [Speaker Changed] I know you guys don’t release public performance numbers, but I know you are doing much better than your benchmark this quarter.

And because remember, Lehman had the Lehman Agg and that was the benchmark. There is above benchmark returns to be generated by active selection of credit quality duration and specific bonds. Now, we’re shifting to more international places like China, Europe, et cetera, that are really growing, and that valuations are cheaper.

Executing the Profitability Triad: Growth, Efficiency, and Margin in 2025 The Economic Context: A Brief Look Back In early 2025, macroeconomic changes reshaped how private equity firms think about value creation: Rising tariffs. Where Theres Opportunity Theres still more that can be done.

Globally, Social bonds will be constrained by a lack of benchmark-sized projects, while transition-labeled bonds and sustainability-linked bonds (SLBs) will remain niche segments as they navigate evolving market sentiment, the ratings agency posted on its website. Its now upgrading and extending the lifetime of its machines.

And one of the worst performing factors has been valuation. So we’re now in an environment where all the 45-year-old portfolio managers out there have been, have worked their entire careers in these momentum fueled markets, and they’ve been trained to believe that valuation doesn’t matter.

You get a BA in economics and poli sci from the University of Delaware. And it had to do with the discipline of the models that he used and how he segmented economic liquidity, investor liquidity, and then technicals and and breath conditions and understood how they melded together. What was the original career plan?

You get a BA in Economics from Hamilton College. So what we did was we figured out the economic rationale, the macroeconomic influences about why growth and value work at any point in time. Everybody wants to sell a company when they get a good valuation. So we do a lot of valuation work. You get an MBA from NYU.

But if you buy low multiples and sell high multiples, either in a long-only beat the benchmark sense, whether over and underweight, and you did the same thing everyone does and call me a hedge fund manager. And value and momentum do, whether it’s relative outperformance against a benchmark or absolute performance in a hedge fund.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content