This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

So of course, what the Fed will do impacts markets, impacts valuations, impacts interest rates. 00:46:16 [Speaker Changed] I mean, if you look at the, the valuations, if you look at the fundamentals, it is, it’s surprising, right? So there’s still a pretty big valuation gap. What’s keeping you entertained?

I like to think that, you know, in core wealth management, Morgan Stanley, and, and you know, where we’ve come, you know, first under James Gorman and now hopefully under, under Ted Pick’s leadership is really, you know, differentiating us and allowing us to pull away from the pack, at least in wealth management.

We learned everything, you know, across from accounting to auditing to, to tax and valuation. I ended up in what was called the valuation services group, where we valued real estate and businesses either for transactions or for m and a activity. Starting with what’s keeping you entertained these days?

So I wanna talk a little bit about leadership, especially leadership at a, a large investment firm. What did the experience at both this small firm and a a a giant firm, how did that shape your leadership at Barings? You, you’ve self described your own leadership style as confident humility. They’re giant.

That is not being reflected in valuations from a top down standpoint. One is, if you think about EM, equity valuations versus the s and p, the EM index is trading at, you know, 10 to 11 times forward pe. But key valuations are necessary but not sufficient condition for an opportunity to be attractive. 00:35:18 Right.

And I understood from that that well-meaning people can still muck things up because they don’t have an appropriate guide frame or appropriate leadership, or they’re not, so like little things can take projects astray. What, what’s keeping you entertained? But there’s a variety of ways to incorporate it.

And in 2017, the leadership of jb, which was a European money manager, came calling and, and, and they had fallen in love. And, and so my point to you is, is once we define the categories, dominance matters, somebody will own the reason the, the, the market is paying upwards of, has been paying upwards of $15 billion a valuation on kava.

It’s online, we have to report to the all of the partners, the leadership teams experience, and then every partner at Bridgeway, that’s every person that has a long-term commitment to and from Bridgeway has to do the same thing. We ask all of our guests, starting with what’s been keeping you entertained these days?

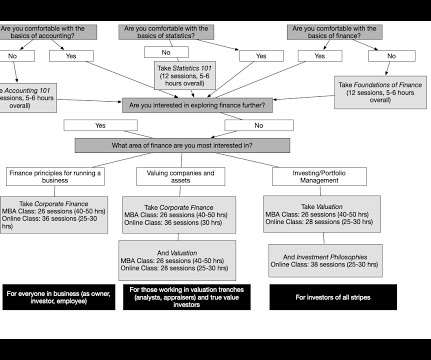

Owner’s opinions of their business value can be influenced by inherent biases, flawed valuation methodologies, and factors lurking beyond their control. Owners often seek valuations from CPAs or similar entities for purposes such as insurance, estate planning, or internal events.

Starting in late January 2023, I will be back in the classroom, teaching valuation and corporate finance to the MBAs and valuation to the undergraduates, and these classes will continue through May 2023.

Starting in late January 2023, I will be back in the classroom, teaching valuation and corporate finance to the MBAs and valuation to the undergraduates, and these classes will continue through May 2023.

It was a good week for Amazon’s stock price, with a valuation that briefly exceeded $1 trillion before falling back into the far more conservative $927 billion range, reaffirming its membership in the trillion-dollar club along with Microsoft ($1.27 trillion market value), Apple ($1.38 CEO John Furner. percent throughout the industry.

And from there, I I really realized that while I loved being an investor or making investment recommendations, I also felt like it wasn’t perhaps my true genius and that I might be more successful in the long run to focus on a leadership direction of my, my career. But maybe second to valuation as a primary consideration.

JEFFREY RAYPORT: Well, maybe the best way to bring it to life is to talk about one of the companies that we’ve spent a lot of time with, and that’s King Digital Entertainment. Can you just explain what extrapolation is? It’s a London-based game maker. Many people will know it. It’s been recently acquired by Activision Blizzard.

How, how are the higher rates affecting valuations amongst private companies? 00:37:43 [Speaker Changed] So there’s two issues that are affecting valuations. 00:39:24 [Speaker Changed] So, so let’s look at valuation in a historical perspective. The auditors look at those valuations.

One is our leadership in thematic investing. And we’re having very good conversations with clients that I think, at current valuation levels, they remain, you know, very interested in the market and they see some opportunities. I think I mentioned earlier, I have like a four-and-a-half-year-old that keeps me really entertain.

RITHOLTZ: We’ll talk a little bit about leadership and crew development a little later. So let’s discuss leadership and what you do to develop crew members and to identify and foster other people’s leadership skills. DAVIS: Where international equities, because of valuations, probably 7% to 7.5%.

The fact that you’ve got declining risk appetite, declines are prolonged, deep and valuations mean revert. The second, and what’s interesting about that period, is the fact that valuations actually peaked in 1961. MIAN: Valuations are ebb and flow. What’s entertaining the family? ” RITHOLTZ: Right.

But that valuation, to be able to come up with the valuation, to be then able to work in a restructuring process, bankruptcy process, and say, Hey, I think at the end of this, we are buying debt at 50 cents. Starting with, tell us what’s keeping you entertained these days? Netflix, what keeps you entertained?

One, when people have asked me to compare and contrast today versus 2007, 2008, what you hear from a lot of people is, yes, there’s some fairly heady valuations. What’s been keeping you entertained? We’ve seen a couple of these events now. There were some fairly aggressive kind of investment strategies being pursued.

It’s just a fascinating conversation about looking at the world from both bottoms up and top-down, as well as thinking about what valuations are like, how likely are macro events, the impact you’re getting not just the return on capital, but as famously said in fixed income, a return of your capital. RITHOLTZ: Really quite fascinating.

And if they don’t, we’re happy to own them at the valuation that we are creating that company act. I’m not, I’m not really into fiction or, or entertaining reading. Tell us about what’s going on today that makes it so interesting. 00:37:26 [Speaker Changed] Huh. That’s really quite intriguing.

Now the, the V on the LTV loan to value the value oftentimes is a disparity because when you ask a tech person, what’s this company worth, generally it’s, it’s very, very high numbers, which we don’t always support from our valuation. What’s been been keeping you entertained?

And we’d sort of turn that into a valuation business. MILLER: Well actually I thought, leading up to the great financial crisis, I thought to myself, we’re going to be out of business within a couple of years because nobody wanted an independent valuation. What’s keeping you entertained? RITHOLTZ: Sure.

Now, we’re shifting to more international places like China, Europe, et cetera, that are really growing, and that valuations are cheaper. You serve as the National Leadership Council of Communities in Schools, and the Educational Foundation in New York. Think about the incredible growth of U.S. I mean, I watch tons of sports.

I found the book to be really entertaining and, and amusing and a little bit horrifying. It really is just a, a, a very entertaining book and I thought this conversation was, was absolutely fascinating. 00:38:35 [Speaker Changed] So, so tell us a little bit about the leadership of Tether. But Zeke is a, a fascinating guy.

And one of the worst performing factors has been valuation. So we’re now in an environment where all the 45-year-old portfolio managers out there have been, have worked their entire careers in these momentum fueled markets, and they’ve been trained to believe that valuation doesn’t matter. I loved White Lotus.

Obviously, you know, geopolitics and the election and black swan risks are always the potential, but I think sentiment and valuation. As we all learned in the 1990s, valuation can get stretched and sentiment can get stretched, and that can last for years. Let’s jump to our speed round.

And he also talked about the importance of the US role in the world in terms, I 00:30:48 [Speaker Changed] I picked that up also in terms of, I thought that was the first time I’ve heard of Fed Chief talk about liberal democracy is an important aspect of global leadership. And I thought, oh boy, we’re in big trouble.

And this is a combination of strategy and, and business leadership and investing. And then this is the one I was saying the pillar off to the side valuation is a nice to know, but it is not a driving force of my investment process. Well there’s also this assumption that that underpins this view on valuations.

00:24:49 [Speaker Changed] So let’s talk a little bit about valuation in the public markets. Does that valuation difference in the public markets extend to private markets as well? Does that valuation difference in the public markets extend to private markets as well? Hence the valuation gap.

Doesn’t it deserve a, a richer valuation? And, and then they’ve lost leadership on Foundry to TS MC 00:36:14 [Speaker Changed] And then MA Mobile, they lost 00:36:16 [Speaker Changed] Leadership on that. That we ask all of our guests starting with what’s keeping you entertained these days? I 100% agree.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content