This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In the first five posts, I have looked at the macro numbers that drive global markets, from interest rates to risk premiums, but it is not my preferred habitat. A key tool in both endeavors is a hurdlerate a rate of return that you determine as your required return for business and investment decisions.

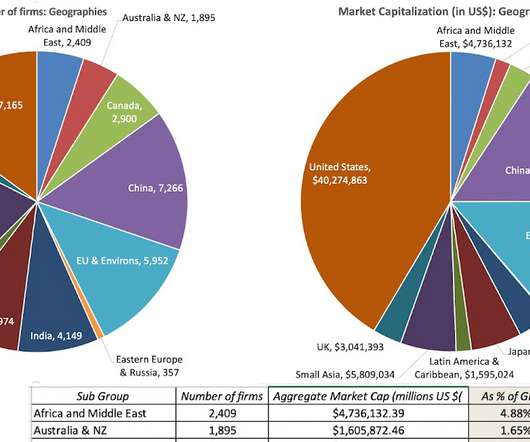

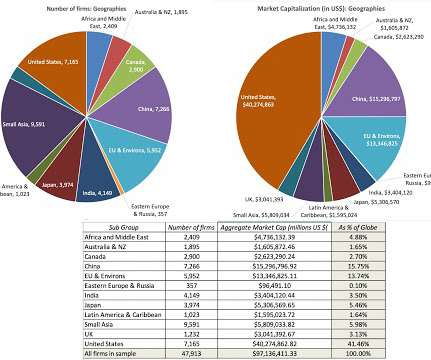

Not surprisingly, the company listings are across the world, and I look at the breakdown of companies, by number and market cap, by geography: As you can see, the market cap of US companies at the start of 2025 accounted for roughly 49% of the market cap of global stocks, up from 44% at the start of 2024 and 42% at the start of 2023.

What is a hurdlerate for a business? In this post, I will start by looking at the role that hurdlerates play in running a business, with the consequences of setting them too high or too low, and then look at the fundamentals that should cause hurdlerates to vary across companies. What is a hurdlerate?

Risk and HurdleRates In investing and corporate finance, we have no choice but to come up with measures of risk, flawed though they might be, that can be converted into numbers that drive decisions. By the same token, Embraer and TCS are global firms that happen to be incorporated in Brazil and India, respectively.

I am in the third week of the corporate finance class that I teach at NYU Stern, and my students have been lulled into a false sense of complacency about what's coming, since I have not used a single metric or number in my class yet. Data Update 4 for 2025: Interest Rates, Inflation and Central Banks!

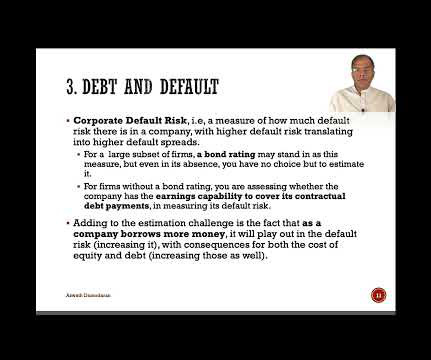

Risk and HurdleRates In investing and corporate finance, we have no choice but to come up with measures of risk, flawed though they might be, that can be converted into numbers that drive decisions. In corporate finance, this takes the form of a hurdlerate , a minimum acceptable return on an investment, for it to be funded.

Mean reversion : I am not a knee-jerk believer in mean reversion, but the tendency for numbers to move back towards averages is a strong one. Counter made-up numbers : It remains true that people (analysts, market experts, politicians) often make assertions based upon either incomplete or flawed data, or no data at all.

Implementing DTSCF can be more complex than traditional SCF due to the increased number of parties involved and the need to track payments across multiple tiers. Financial institutions can better understand the risk profiles of small suppliers by leveraging alternative data and machine learning, thus expanding access to financing.

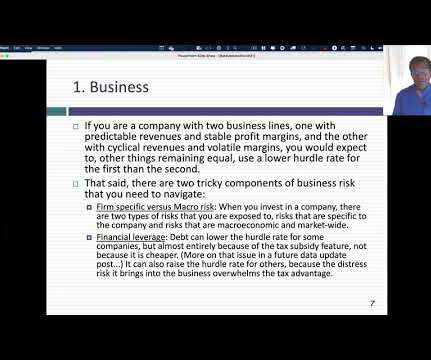

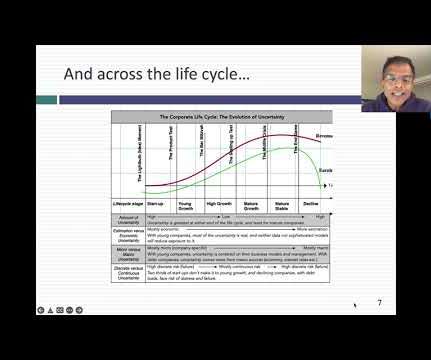

With more mature companies, as investment opportunities become scarcer, at least relative to available capital, the focus not surprisingly shifts to financing mix, with a lower hurdlerate being the pay off. That portfolio will have the benefit of stability, but expecting it to contain ten-baggers and hundred-baggers is a reach.

Mean reversion : I am not a knee-jerk believer in mean reversion, but the tendency for numbers to move back towards averages is a strong one. Counter made-up numbers : It remains true that people (analysts, market experts, politicians) often make assertions based upon either incomplete or flawed data, or no data at all.

But the true change comes when, hey, you know what, those loyal to that technological change figure out over not one, two, but three, five years, how to drive change and how to leverage it. We’ve always been a virtual company, just used to be through the mail and 1-800 number when I joined. That means a low hurdlerate.

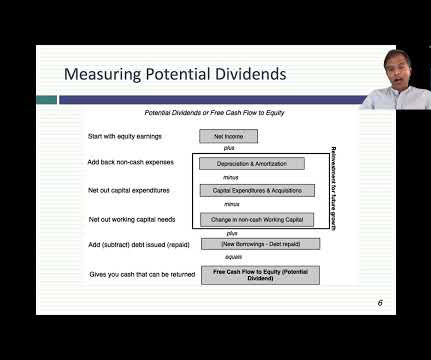

The dividend principle, which is the focus of this post is built on a very simple principle, which is that if a company is unable to find investments that make returns that meet its hurdlerate thresholds, it should return cash back to the owners in that business.

You do the math and you’re like, “Okay, well, an advisor can handle about 100 clients, an associate advisor can help with some of those clients, you can leverage maybe an associate advisor with a couple of advisors, but there’s a capacity limit for each of the roles.” And so, that can move the numbers, as well.

He co-chairs a number of the asset management investment committees. So I interviewed with a bunch of banks, got a number of job offers by the end of the week, and joined Goldman Sachs in October 1998. I ended up being hired onto the high yield desk as a research analyst and did that for a number of years, a couple of years.

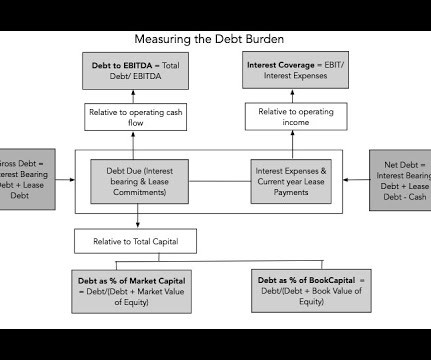

In fact, that may explain why firms that trade at low EV to EBITDA multiples are more likely to become targets in leveraged buyouts (LBOs) or leveraged recapitalizations. Business risk : Not surprisingly, for any given level of cash flows and marginal tax rate, riskier firms will be capable of carrying less debt than safer firms.

I mean, I didn’t want to blow my own trumpet up too much because most of the positions were in place, the quality funds, which more defensive and less leveraged, and low allocation to — a relatively low allocation to equities, and then the hedge funds sort of long/short positions that benefited in the financial crisis.

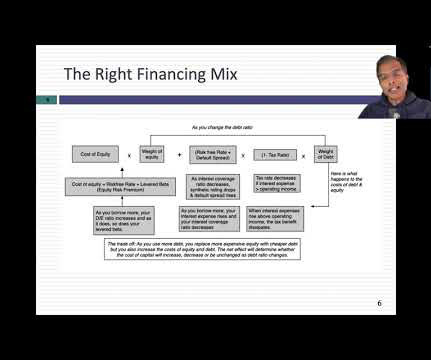

The cost of debt is lower than the cost of equity : If you review my sixth data update on hurdlerates , and go through my cost of capital calculation, there is one inescapable conclusion. At every level of debt, the cost of equity is generally much higher than the cost of debt for a simple reason. to3.5%) during the year.

Honest back testing, really looking at the numbers versus exaggerating returns and, and making up the claim that something’s live when it’s not. 12, 14 even that not a lot of numbers. So you’ve got, you’ve got a modeling hurdlerate that you need to figure out when you’re adding diversifiers.

And 00:06:38 [Speaker Changed] Door number one was much better than door number three in, in the circumstances. When we talk about breadth, we’re talking about the numbers of advancers versus decliners. So it’s like, yeah. It, it’s, it’s a totally, it’s, it’s very different.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content