This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

What is a hurdlerate for a business? In this post, I will start by looking at the role that hurdlerates play in running a business, with the consequences of setting them too high or too low, and then look at the fundamentals that should cause hurdlerates to vary across companies. What is a hurdlerate?

I am in the third week of the corporate finance class that I teach at NYU Stern, and my students have been lulled into a false sense of complacency about what's coming, since I have not used a single metric or number in my class yet. Data Update 4 for 2025: Interest Rates, Inflation and Central Banks!

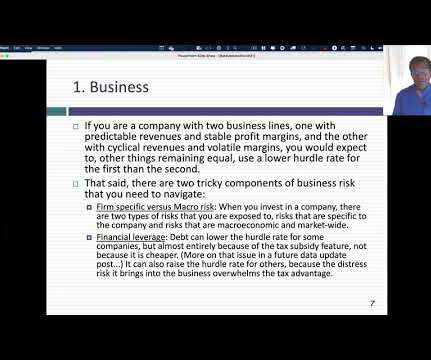

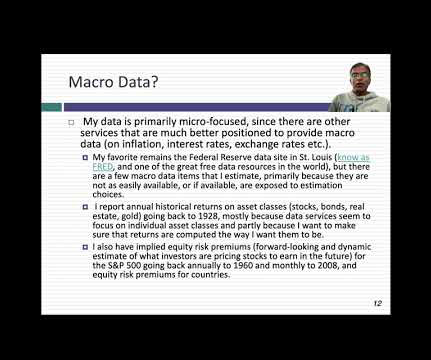

In my last three posts, I looked at the macro (equity risk premiums, default spreads, risk free rates) and micro (company risk measures) that feed into the expected returns we demand on investments, and argued that these expected returns become hurdlerates for businesses, in the form of costs of equity and capital.

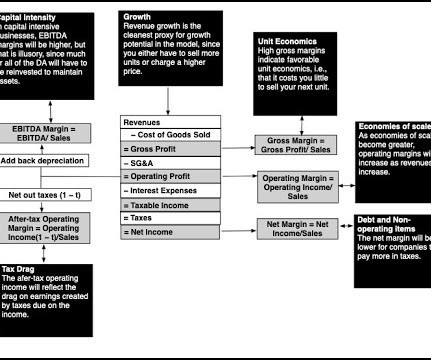

The question of whether a company is making or losing money should be a simple one to answer, especially in an age where accounting statements are governed by a myriad of rules, and a legion of number-crunchers follow these rules to report profits generated by a firm. The numbers yield interesting insights. .

Measuring Profitability The question of whether a company is making or losing money should be a simple one to answer, especially in an age where accounting statements are governed by a myriad of rules, and a legion of number-crunchers follow these rules to report profits generated by a firm. The numbers yield interesting insights.

Implementing DTSCF can be more complex than traditional SCF due to the increased number of parties involved and the need to track payments across multiple tiers. Societe Generale also offers a dedicated and simplified solution to retail clients or small and midsize enterprises (SMEs) based on their ESG rating.

In January 1993, I was valuing a retail company, and I found myself wondering what a reasonable margin was for a firm operating in the retail business. Aggregate operating numbers 3. Insider, CEO & Institutional holdings 2. Beta & Risk 1. Return on Equity 1.

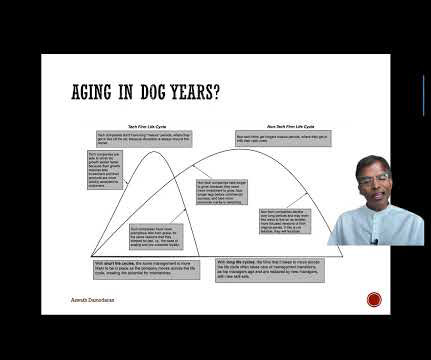

With more mature companies, as investment opportunities become scarcer, at least relative to available capital, the focus not surprisingly shifts to financing mix, with a lower hurdlerate being the pay off. That portfolio will have the benefit of stability, but expecting it to contain ten-baggers and hundred-baggers is a reach.

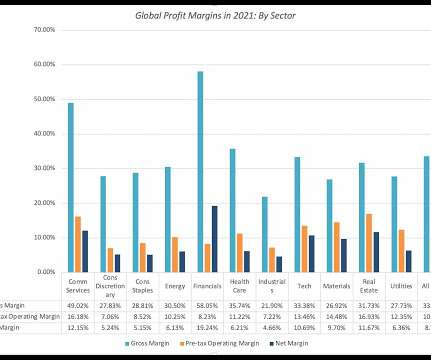

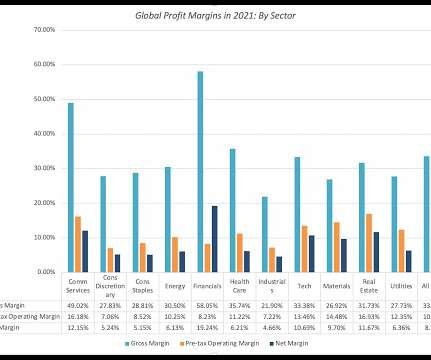

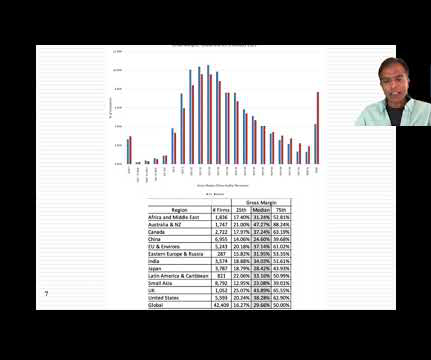

Starting with gross margins, and computing the number for all non-financial service firms, we report the distribution of gross margins across publicly traded companies at the start of 2023, again based upon gross income and sales in the most recent twelve months: While the median gross margin across all publicly traded global firms is about 30%.,

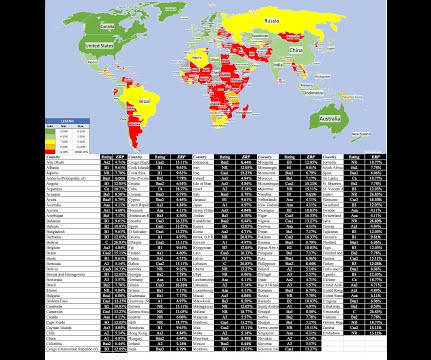

Thus, if a country derives 50% of its economic output from iron ore, a drop in the price of iron ore will cause pain not only for mining companies but also for retailers, restaurants and consumer product companies in the country.

And 00:06:38 [Speaker Changed] Door number one was much better than door number three in, in the circumstances. When we talk about breadth, we’re talking about the numbers of advancers versus decliners. So it’s like, yeah. It, it’s, it’s a totally, it’s, it’s very different.

Honest back testing, really looking at the numbers versus exaggerating returns and, and making up the claim that something’s live when it’s not. 12, 14 even that not a lot of numbers. So you’ve got, you’ve got a modeling hurdlerate that you need to figure out when you’re adding diversifiers.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content