This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The return on equity may be an equation that comes from accounting statements, but in keeping with my argument that every number needs a narrative, each of these numbers has a narrative, often left implicit, that should be made explicit.

Lisa Shallet, chief Investment Officer at Morgan Stanley has had a number of fascinating roles in Wall Street, which is kind of amusing considering she had no interest in working on Wall Street, and yet she was CEO and chairman at Sanford Bernstein. I was traveling and on an airplane all the time. So I took the plunge, I quit.

While the job losses varied across sectors, with job skills and unionization being determining factors, the top line numbers tell the story. However, attempts at disruption, whether it be from Mark Cubans pharmaceutical start-up or from Google and Amazons health care endeavors, have largely left the system intact.

In addition, they’ve put up some really impressive numbers over the past 30 years, which has given them the opportunity to donate tens of millions of dollars to their favorite organizations. We don’t give exact numbers. Number one, it means our transaction costs are less, which based on your career, you know exactly.

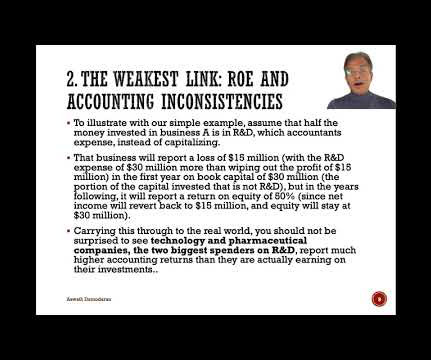

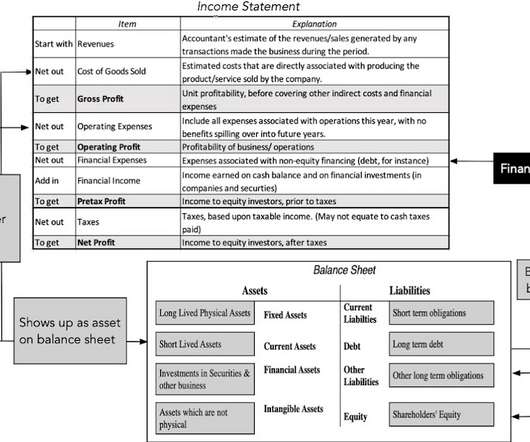

In the second post, I pointed to inconsistencies in how accountants classify operating, capital and financing expenses , and the consequences for reported accounting numbers. As someone who has spent the last four decades talking, teaching and doing valuation that we have lost our way in valuation.

In the second post, I pointed to inconsistencies in how accountants classify operating, capital and financing expenses , and the consequences for reported accounting numbers. Narrative and Value As someone who has spent the last four decades talking, teaching and doing valuation that we have lost our way in valuation.

That skewing can affect valuation and pricing judgments about these firms, and correcting accounting inconsistencies is a key step towards leveling the playing field. To the extent that these numbers are used in computing financial ratios, it will affect your measures of operating income and return on invested capital.

The resulting debate among accountants about how to bring intangibles on to the books has spilled over into valuation practice, and many appraisers and analysts are wrongly, in my view, letting the accounting debate affect how they value companies. So, how far has accounting come in bringing intangible assets on to balance sheets?

That skewing can affect valuation and pricing judgments about these firms, and correcting accounting inconsistencies is a key step towards leveling the playing field. Accounting 101 I am not an accountant, and have no desire to be one, but I have used their output (accounting statements) as raw material in valuation and corporate finance.

Even though we live in an age where user platforms and hyper revenue growth can drive company valuations, that adage remains true. The numbers yield interesting insights. . The proverbial bottom line for success in business is the capacity to deliver profits, at least in the long term.

Munchery came on the scene in 2010, and hit a valuation of $300 million in 2015. Careem will now provide food delivery services in Dubai and Jeddah, but the company sees the service eventually expanding to include pharmaceuticals. You’ll benefit from the sheer number of eyes on the app that can find your restaurant.”

Even though we live in an age where user platforms and hyper revenue growth can drive company valuations, that adage remains true. The numbers yield interesting insights. The proverbial bottom line for success in business is the capacity to deliver profits, at least in the long term.

But, in general, as investors deepen their understanding about the new economy businesses, their valuations are expected to return to a more reasonable level, Deloitte China added. This indicates a 14% fall in number of IPOs, but an 842% surge in proceeds against 37 IPOs raising HK$14.1 Report highlights. billion (US$1.8 billion (US$7.9

Coming in at number one is India’s Rivigo , a logistics company that announced $50 million in Series D funding; according to reports, the investment has nearly pulled the company into unicorn territory. Rivigo focuses its B2B services on delivery and logistics for various verticals across India, including eCommerce and pharmaceutical firms.

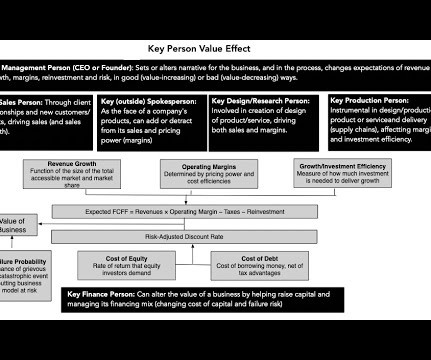

Of course, and with small businesses, especially those built around personal services (a doctor or plumber’s practice), it is part of the valuation process, where the key person is valued or at least priced and incorporated into valuation. To estimate key person value, there are three general approaches: 1.

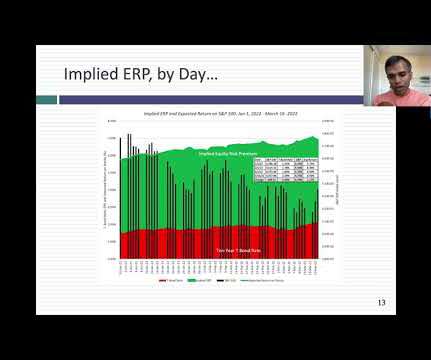

The implied equity risk premium, which started the year at 4.24%, was at 4.73% by March 16, and the expected return on equity, which was close to an all-time low at 5.75% at the start of the year, was now up to 6.92%, still lower than historical norms, but closer to the numbers that we have seen in the last decade. YouTube Video.

The implied equity risk premium, which started the year at 4.24%, was at 4.73% by March 16, and the expected return on equity, which was close to an all-time low at 5.75% at the start of the year, was now up to 6.92%, still lower than historical norms, but closer to the numbers that we have seen in the last decade. to 25% for the Eurozone.

I left HSBC Group at the end of 1999, and some friends of mine that I’d known a long time had came on — came out of the fixed income side at a number of investment banks, generally, top II-rated (ph) mortgage research and more — traders, fixed income salesman, and to raise third-party capital broker-dealers required. CONROD: Sure.

And actually, interestingly, Joe was director of research there for a number of years before I moved on to start Perceptive. I’m 00:19:11 [Speaker Changed] Really intrigued by the concept at some of the big pharma, the big pharmaceutical companies and their pipeline. You know, valuation sense, 00:30:47 [Speaker Changed] Right.

And because my mother and grandmother were looking at these trying to figure out what was going on, I was curious about the sea of numbers. And 00:28:03 [Speaker Changed] That’s an amazing number. 00:44:11 [Speaker Changed] Kathy would may have her own valuation, so, but I can’t replicate it myself.

I was thinking any number of things and mostly that I didn’t really know what I wanted to be when I grew up, but I was not kind of at all informed by, you know, gender norms that people asked me a lot about now, in particular how do you know a woman, how did you think about ending up in this thing? MCCARTHY: Yeah, absolutely.

Everybody wants to sell a company when they get a good valuation. So up 18 or 19 percent for the year, you see those spectacular numbers. Obviously, profits, very important to company valuation — BERNSTEIN: Absolutely. The other thing we do, Barry, is we group valuation as a sentiment indicator. BERNSTEIN: Correct.

In addition to being a portfolio manager and running a number of mutual funds and ETFs, he is just a world-class technology investor who understands the sector like few other people do. And you want to get every, every number right? Doesn’t it deserve a, a richer valuation? I’m shocked it’s only 29%.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content