This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Financial reporting specialist and lecturer Adam Deller explains the basic principles of IFRS 5, 'Non-Current Assets Held for Sale and Discontinued Operations'. The post The fundamentals of IFRS 5 appeared first on FutureCFO.

Medical device companies can offer training, consulting, and certification programs alongside the sale of their equipment to ensure healthcare providers can fully utilize the technology. Accounting standards such as ASC 606 and IFRS 15 provide guidance, but medical device companies must navigate specific nuances for different models.

As organizations deal with increasingly complex revenue streams across sales, services, subscriptions, and projects, the need for a flexible, scalable, and industry-tailored revenue recognition solution has never been more critical. Enter Universal RevRec (URR) —SAP S/4HANA Cloud Public Edition’s powerful new revenue recognition platform.

Compliance with standards like ASC 606 and IFRS 15 is still crucial, but the focus has shifted to optimising operations for growth. Inconsistent application of IFRS 15 and ASC 606 can lead to significant risks, including audit adjustments, compliance penalties, and investor mistrust.

Harmonising financial reporting and compliance Finding the balance between financial reporting and compliance across multiple jurisdictions, while trying to comply to global standards such US GAAP and IFRS with local tax regimes and regulatory requirements without overburdening local teams can be such a huge task for many organisations.

Many companies have suffered from the effects of the crisis and the drop in their sales, or sometimes they have simply experienced delays in delivery from their suppliers or payment from their customers. Any hiccup may require readjustment of the accounting of the transactions, as required by IFRS 9.

Financial Information Systems help businesses automate compliance checks, ensuring they meet regulations such as International Financial Reporting Standards (IFRS 17) and tax laws. Often, finance teams work separately from sales, operations, and HR, leading to inconsistent financial data.

Financial governance allows your organization to meet compliance requirements, such as IFRS and GAAP updates, by having the right financial controls in place. For single and multiple family offices, governance is key to financial success and is an important element of your organizational structure.

ASC 606/IFRS 15 Compliance : Under the ASC 606 (U.S.) and IFRS 15 (International) revenue recognition standards, media companies must recognize revenue based on performance obligations, such as when content is made available or when specific services are rendered.

It can quickly become unmanageable to try and handle lease contract management, lessor accounting, maintenance services, sales of consumables, revenue recognition and disclosure reporting all with different siloed software. For revenue recognition, they also must comply with ASC 606 and IFRS 15.

In addition, medical device vendors are interested in finding ways to make revenues more predictable as opposed to the inherently spiky revenue seen from large equipment sales. Bramasol client, Hillrom, is a prime example of how new subscription-based models can be successful in the medical device sector.

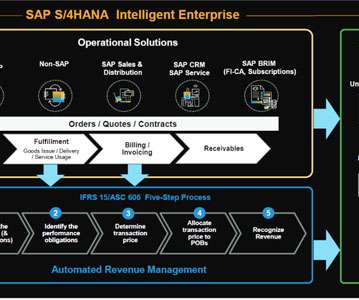

Within the Five-Step model, Step 4 of ASC 606 and IFRS 15 requires an allocation of the total consideration in a contract, which your company is entitled to collect for each distinct performance obligation. Standalone Selling Price: What is SSP, why is it needed, and how is it determined?

GAAP, IFRS, and cash base side by side for better visibility. Create quotes, sales orders, backorders, invoices, returns, credit memos, debit memos, and more with ease and rapidly deliver them via email. Ability to implement user-access controls. Ability to view performance on U.S. Define your own workflows.

Last-mile delivery has become a critical cost factor as retail sales shift from in-store to online. Some of the key challenges and disruptive trends in the transportation sector include: Supply chain inefficiencies exposed by the pandemic and shifts in consumer buying behavior.

Although the initial compliance phase for ASC 606 and IFRS 15 revenue recognition mandates is in the rear-view mirror for most companies, it's important to also keep a focus on the road ahead because optimization of overall RevRec processes across the enterprise will be key to ongoing success. Cloud Deployment Options.

And yet, it remains key to have access to, and reconciliation of, data that ranges from sales to travel expenses. This is especially true when multinationals must reconcile data across different accounting standards, such as GAAP and IFRS. The optimization of the accounting process, he said, is difficult at times with limited staff.

Bringing an Expanded RevRec "Compliance Mindset" into New Business Models: Even though subscription-based, Digital Solutions Economy (DSE) business models are radically changing many industries, RevRec compliance under ASC 606 and IFRS 15 is still required.

Revenue Stream Diversification : For automakers, subscriptions offer a steady revenue stream beyond initial vehicle sales. Revenue Recognition Compliance For automakers and ride services providers, ensuring compliance with revenue recognition standards such as ASC 606 or IFRS 15 is critical, especially with recurring subscription revenues.

The 69-million pound victory is equivalent to more than a day’s sales for Sainsbury, which brought in 23.5 What’s interesting is that the court concluded that a lawful level of credit interchange for the UK market would be over 65% higher than the 30bps rate cap imposed in the 2015 Interchange Fee Regulation (“IFR”).

Operational Accounting is concerned primarily with the processes for areas like sales, revenue, treasury, cash flow, margins, KPIs, etc. This has enabled clients to smoothly comply with ASC 842 and IFRS 16.

Bringing an Expanded RevRec "Compliance Mindset" into New Business Models: Even though subscription-based, Digital Solutions Economy (DSE) business models are radically changing many industries, RevRec compliance under ASC 606 and IFRS 15 is still required.

Without a solid IT system, consolidating sales data from different stores for monthly reporting can be a nightmare. With a robust system in place, real-time sales data from all locations can be automatically pulled into the financial reports, reducing the time spent on manual entries and increasing data accuracy.

CBRR is based on optimized features for revenue accounting inbound processing and contract management and enables assigning the sales price to the relevant output of the obligations in the underlying contract. Agreements are analyzed to detect the performance obligations POBs and decide on the revenue recognition patterns.

An FP&A leader needs to collaborate with different business functions including sales, marketing, business development, supply chain, IT, HR etc. The model can help understand how different support functions (procurement, IT, HR etc.) work to add value to the entire process.

They also need to address compliance requirements such as revenue reporting under ASC 606 and IFRS 15, which are still required but can be more complex for DSE business models. Sales – streamlining of sales master data, sales contract management, sales order processing, billing, invoicing, claims, returns, refunds, and sales forecasting.

By the end, you should clearly understand what qualifies as a goodwill asset, how to evaluate its worth and how it will be taxed at the time of sale. It is the amount of money a buyer pays above the fair value market price in the sale of a business. What Is a Goodwill Asset? Are All Intangible Assets Goodwill? billion.

These systems provide built-in support for complexities such as currency translation, intercompany eliminations, and reporting under multiple accounting guidelines, such as US GAAP or IFRS. The need for an EPM solution will emerge.

It is true that IFRS has moved faster in bringing intangible assets on to balance sheets, albeit not always in the most sensible ways, but even with those rules in place, progress on bringing intangible assets onto balance sheets has been slow.

Using the words of IFRS (1.7), ‘ Information is material if omitting, misstating or obscuring it could reasonably be expected to influence decisions that the primary users of general purpose financial statements make on the basis of those financial statements, which provide financial information about a specific reporting entity ’.

It automates the discovery of anomalies and missing data, projects sales and budgets, pressure-tests assumptions, and drastically simplifies and accelerates planning processes while improving accuracy. Planful addresses these challenges with Predict.

In the years since, disclosure requirements have changed and expanded, with companies in foreign markets creating their own rules in IFRS (International Financial Reporting Standards), with many commonalities and a few differences from GAAP. In 2019, Uber claimed that its TAM was $5.2

This includes integrations with systems like Salesforce, QuickBooks, NetSuite, Xero, and Sage so you can analyze and use all your data—including, HR, sales, and CRM—in one place. In addition to offering financial and sales planning solutions, Workday Adaptive also caters to workforce and operational planning needs.

For instance, I have always computed the present value of lease commitments in future years and treated that value as debt, a practice that IFRS and GAAP have adopted in 2019, but that computation requires explicit disclosures of lease commitments in future years.

In addition, from an internal perspective, Bramasol is proactively implementing AI capabilities across virtually all functional areas, including service delivery, customer satisfaction, project management, marketing, sales and finance. We see AI as a game changer for improving productivity for our team and higher value for our clients.

Delivering Consumer Services: Customer Data Centralization: With SAP cloud-based ERP, telcos can integrate customer data across all touchpoints (sales, service, billing), enabling a 360-degree view of each customer. IFRS or GAAP) becomes easier, and financial data can be tracked and reported in real-time.

We organize all of the trending information in your field so you don't have to. Join 39,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content